Silicon Dioxide Market Outlook:

Silicon Dioxide Market size was valued at USD 10.89 billion in 2025 and is likely to cross USD 19.69 billion by 2035, registering more than 6.1% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of silicon dioxide is assessed at USD 11.49 billion.

The silicon dioxide market’s growth is due to the expansion of end use industries and rising demand for high-performance electronic devices. Silicon dioxide is a critical material in the manufacturing of semiconductors and the growth of the semiconductor industry is poised to drive demand for the material. For instance, in June 2024, Evonik, one of the global leaders in specialty chemicals, announced investments in the North America semiconductor industry and began production of ultra-high purity colloidal silica in the U.S. Evonik’s ultra-high purity colloidal silica production plant will be the first of its kind in North America. It augurs well for the future of the silicon dioxide market as it paves the way for more industry stakeholders to expand silica production.

Another major growth driver of the silicon dioxide market is its growing adoption in the food & beverage industry as a stabilizer anti-caking agent. The market benefits from favorable regulatory clearance for the use of silica as a food additive, fostering consumer trust and allowing manufacturers to invest in supplying food-grade silica. For instance, in October 2024, the European Food Safety Authority (EFSA) concluded that silicon dioxide as a food additive does not cause safety concerns and it applies to all age demographics. Furthermore, busy consumer lifestyles have led to rising demand for ready-to-eat food, which requires silicon dioxide as an additive to maintain product quality and extend shelf life. The favorable trends within the food & beverage sector are projected to assist a sustained demand for food-grade silica that key industry players can leverage.

Additionally, the financial performance of major players in the silicon dioxide market highlights the potential of profit within the sector. For instance, in February 2024, U.S. Silica Holdings, Inc., announced their annual report for the financial year 2023, highlighting that the full year net income of USD 146.9 million increased 88% year-over-year, while full year company contribution margin of USD 549.7 million increased 16% year-over-year. The improved product mix in the industrial and specialty products segment of the company played a major role in the growth indicating favorable opportunities in the silicon dioxide market. Profitable performance by key players is reinforcing investor confidence and indicates the growing demand for silicon dioxide. The global silicon dioxide market is poised to leverage the favorable trends and maintain its robust growth curve by the end of the forecast period.

Key Silicon Dioxide Market Insights Summary:

Regional Highlights:

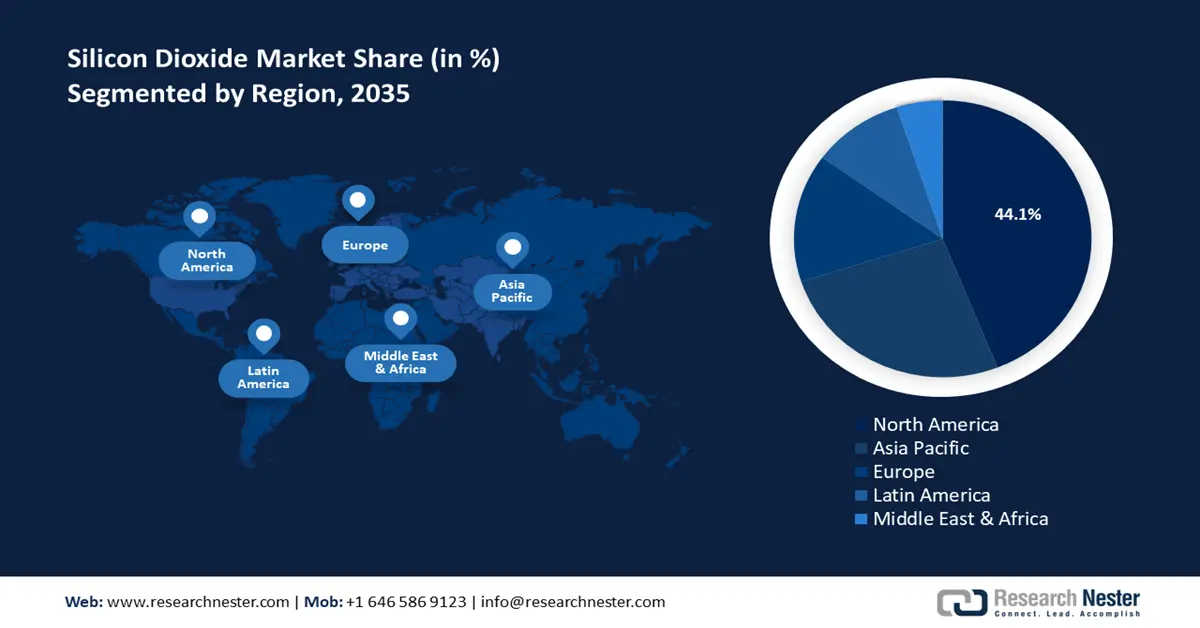

- North America silicon dioxide market will account for 44.10% share by 2035, driven by rising investments by industry leaders to expand production capacity.

- Asia Pacific market will exhibit the fastest growth during the forecast period 2026-2035, fueled by booming industrialization and urbanization trends in APAC.

Segment Insights:

- The building and construction segment in the silicon dioxide market is forecasted to hold a 39.90% share by 2035, attributed to increasing urbanization driving demand for silica in cement and glass manufacturing.

Key Growth Trends:

- Expanding usage in personal care and pharmaceuticals

- Surge in specialized applications and expansion in emerging markets

Major Challenges:

- Supply chain bottleneck constraints

- Price sensitivity among small-scale end users

Key Players: Evonik Industries AG, PPG Industries, Inc., Cabot Corporation, Solvay S.A., Wacker Chemie AG, Tosoh Corporation, Tokuyama Corporation, Gelest, Inc., Imerys S.A., Shin-Etsu Chemical Co., Ltd.

Global Silicon Dioxide Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 10.89 billion

- 2026 Market Size: USD 11.49 billion

- Projected Market Size: USD 19.69 billion by 2035

- Growth Forecasts: 6.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (44.1% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: China, United States, Germany, Japan, India

- Emerging Countries: China, India, Japan, South Korea, Thailand

Last updated on : 18 September, 2025

Silicon Dioxide Market Growth Drivers and Challenges:

Growth Drivers

- Expanding usage in personal care and pharmaceuticals: The silicon dioxide market is poised to benefit from the expanding applications in the pharmaceuticals and personal care sectors. Silica is an absorbent powder in cosmetics and a key ingredient in makeup and sunscreens. In March 2023, Dow Personal Care announced the acceleration of sustainable portfolio transformation. It launched the EcoSmooth Rice Husk cosmetic powder that contains rice silica obtained from rice agriculture by-product feedstock. The rise of clean beauty trends is poised to drive further demand for the compound, and sustainable cosmetics portfolio expansions by major players indicate the sector’s growth potential.

Additionally, the healthcare industry’s growing reliance on silicon dioxide for delivery systems drives the sector. Ongoing research on silica-based nanoparticles as therapeutics has the potential to expand applications of silica in the healthcare industry. - Surge in specialized applications and expansion in emerging markets: Beyond the regular end use applications and industries such as construction, electronics, food & beverage, cosmetics, etc., the silicon dioxide sector is exhibiting a growth curve due to a surge in specialized applications that opens new revenue streams. The rising demand for silicone doll manufacturing where silica is a crucial starting material, and 3D printing are encouraging trends for key market players to invest in expansion of production capabilities. For instance, in October 2024, Evonik announced a major expansion in silica production in Charleston, U.S., supported by customer demands. The boost in silica production is expected to support the domestic supply chain in North America.

Furthermore, scaling up in emerging markets in APAC is positioned to boost the sector’s continued growth. For instance, in November 2024, PQ announced the expansion of specialty silica production in Indonesia which will support the company in meeting demand for high-quality silica in APAC. Key market players are investing to strengthen their revenue share in the domestic markets of developing economies. - Advancements in curbing emissions: The increasing scrutiny regarding greenhouse gas (GHG) emissions and the global net zero carbon initiatives is prompting businesses to adopt sustainable production methods. Advancements in sustainable manufacturing processes assist in curbing costs in production and boost investor appeal. For instance, in September 2024, Wacker, a German multinational chemical company announced the successful capture of carbon dioxide from the silicon production process, and the ability to reuse or store the GHG to prevent its release into the atmosphere. These advancements are promising for long-term financial benefits by improving profit margins through cost reductions, and increased consumer trust owing to burgeoning sustainability trends globally.

Furthermore, in July 2024, Rover Critical Minerals signed a letter of intent (LOI) to acquire 100% interest in high-purity silica assets in the Silicon Valley Silica Project with Orichalcum Holdings Inc. High-profile acquisitions within the silicon dioxide market are a testament to the market’s promising value for industry stakeholders

Challenges

- Supply chain bottleneck constraints: The global supply chain for silicon dioxide can be prone to logistical disruptions due to geopolitical tensions and transportation inefficiencies. The COVID-19 pandemic and geopolitical conflicts are recent examples of issues causing supply chain bottlenecks. Companies are investing to secure supply chains to mitigate the impact of various events.

- Price sensitivity among small-scale end users: Large-scale industries can absorb the costs of high-quality silica but small-scale end users may struggle with pricing constraints. Budget constraints can limit the adoption of premium materials. The upfront expenses continue to remain a barrier for smaller businesses.

Silicon Dioxide Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

6.1% |

|

Base Year Market Size (2025) |

USD 10.89 billion |

|

Forecast Year Market Size (2035) |

USD 19.69 billion |

|

Regional Scope |

|

Silicon Dioxide Market Segmentation:

End use Industry Segment Analysis

By 2035, building and construction segment is estimated to hold silicon dioxide market share of more than 39.9%. The increasing urbanization propelling construction work for residential and commercial spaces is a significant driver for the market as silica is a crucial component in cement and glass manufacturing. In November 2023, SRMPR Cements in India launched its Portland pozzolana cement (PPC) with an investment worth USD 27 million in production facilities. Since, silica is a key component in the production of Portland cement, new ventures in the cement industry with PPC portfolios boost demand for silica.

Furthermore, advancements in silica-based products are expected to expand the revenue share of key industry players. For instance, in May 2023, U.S. Silica Holdings, Inc., launched the EverWhite Pigment, a highly-refined silica-based pigment for building products and coatings. The advancement is promising for the future of the silicon dioxide sector by benefiting the demand for silica-based pigments.

The electricals & electronics segment by end use industry is positioned to increase its revenue share in the silicon dioxide market by the end of the forecast period. The rising demands from the semiconductor industry and for the manufacturing of optical fibers benefit the segment's growth. The rapid growth of data-intensive applications such as video streaming services and the proliferation of 5G and IoT drives demand for optical fibers that can transmit vast amounts of data.

In July 2024, STL launched the high-density 864F Micro Cables to bring uninterrupted connectivity to dense fiber networks in the U.S. and benefit the service providers in the region. The increasing production of optical fibers is poised to create a sustained demand for silica in its manufacturing process, assisting the segment’s continued growth.

Form Segment Analysis

The amorphous segment of the silicon dioxide market is poised to exhibit robust growth during the forecast period. Its extensive use as a filler, thickening agent, and anti-caking agent drives profitable growth. Furthermore, compared to other forms of silicon dioxide, the amorphous form offers a high surface area making it highly absorbent. Furthermore, the industry-accepted non-toxicity of the material expands usage in various end use applications.

Key players in the silicon dioxide market are investing to expand production capabilities to leverage surging consumer and business demands. For instance, in February 2024, PyroGenesis Canada Inc. announced a milestone for a fumed silica reactor project with the capacity to convert amorphous and quartz silica to fumed silica. The reactor is expected to usher in a new innovative approach to the production of one of the most demanding materials in various end use industries, i.e., silica.

Our in-depth analysis of the global silicon dioxide market includes the following segments:

|

End use Industry |

|

|

Form |

|

|

Application |

|

|

Purity |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Silicon Dioxide Market Regional Analysis:

North America Market Insights

By 2035, North America silicon dioxide market is likely to account for around 44.1% share. The growth of the regional market is owing to rising investments by industry leaders to expand production capacity in the region, benefiting the regional supply chain and reducing downtimes. The U.S. and Canada dominate the region’s market share.

The heightened acquisition deals and portfolio expansions in North America are a major indicator of the profitability of the silicon dioxide market. For instance, in November 2023, the Sio Silica Corporation announced entering a definitive agreement with the Pyrophyte Acquisition Corporation., for a business combination that reflected an enterprise value of USD 708 million and equity value of USD 758 million. The combined business is poised to supply high-purity quartz silica which is a critical mineral in the global net zero transition.

The U.S. silicon dioxide market holds the largest revenue share in North America. The country’s supportive regulatory ecosystem for businesses has led to major players in the industry investing to expand the production of silica in the country. Additionally, the U.S. has cemented itself as a significant exporter of silica and quartz sands in the world, with the Observatory of Economic Complexity estimating exports worth USD 70.1 million and imports worth USD 2.79 million, resulting in a positive trade balance of USD 67.3 million. The surplus indicates strong domestic production capacity, ensuring a stable and reliable supply chain for end use industries that use silica in large quantities.

Furthermore, the rising demand for food-grade silica to be used as a stabilizer in beer production is a key driver of the market. The U.S. Brewer’s Association estimated the country’s beer industry at USD 117 billion, indicating profitable opportunities for food-grade silica suppliers.

Canada is exhibiting robust growth in the silicon dioxide market. The thriving mining industry of Canada provides a steady supply of high-purity silica, catering to diverse applications in the electronics and construction sectors in the country. Furthermore, Canada benefits from the presence of industry leaders such as Sio Silica Corporation and LaPrairie Group. Furthermore, Canada’s push to expand renewable energy production is poised to boost the manufacturing of solar panels that require silicon, and silicon dioxide remains a crucial early-stage component in silicon production.

Furthermore, expansion by companies in Canada to emerging markets is poised to benefit the domestic silicon dioxide sector. For instance, in November 2024, Homerun Resources Inc., reported the discovery of HPQ silica sand in multiple locations in Brazil, and the average drilling results are reported at 99.23% silicon dioxide. The successful drilling operation is expected to benefit the supply of high-purity silica from Canada.

APAC Market Insights

The APAC silicon dioxide market is poised to exhibit the fastest growth during the forecast period. The region’s revenue share is led by China and India. The booming industrialization and urbanization trends in APAC have heightened construction activities and contributed to increasing demand for silica in the construction sector. Additionally, led by China, India, and Japan, APAC has positioned itself as a hub of the semiconductor sector necessitating a steady supply of silica.

Global players are identifying the potential in the APAC silicon dioxide market, evidenced by acquisitions in the region. For instance, in October 2024, Momentive Technologies announced the acquisition of Sibelco’s spherical alumina and spherical silica businesses located in South Korea to strengthen its work on thermal fillers used in thermal interface materials (TIMs) and expand the ceramics powder product portfolio.

China registered a dominant revenue share in the Asia Pacific silicon dioxide market. The major driver of the market’s dominant share in China is the expansion of applications in end use industries. China is a global leader in the production of electronics and semiconductors, necessitating a constant supply of high-purity silicon dioxide. Furthermore, in September 2024, the Observatory of Economic Complexity estimated China’s silicon dioxide exports at USD 60 million and imports at USD 18.3 million, indicating a positive trade balance. With the country seeking to continue its establishment as a global powerhouse for crucial mineral exports, the domestic market within the country promises lucrative opportunities.

Additionally, companies from China are looking to expand the production line for silicon dioxide. For instance, in February 2023, Xinyi Solar Energy Holding Co., Ltd., announced plans of USD 3 million worth of investments in the silica sand mining operations in the Bangka-Belitung Islands of Indonesia.

India is expected to increase its revenue share in the APAC silicon dioxide market. A key opportunity for the market in India is to fill the supply chain gap that can occur due to rising geopolitical tensions between the U.S. and China, with the former banning the import of silica-based solar materials from the latter. This provides an opportunity for companies within India to increase their production to support the global supply chain, as well as for global companies to invest in India.

Companies in India are investing to increase production capacities to leverage the favorable market trends. For instance, in November 2023, Vesuvius expanded its operations by inaugurating alumina-silica (AlSi) and basic monolithic manufacturing facilities in the country. The development is in alignment with the ambitious Make in India goals of the country, which focuses on improving domestic manufacturing, and the government-backed incentives are beneficial to boost production lines in the country.

Silicon Dioxide Market Players:

- Evonik Industries

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Wacker Chemie AG

- Rover Critical Minerals

- Homerun Resources Inc.

- Sio Silica Corporation

- LaPrairie Group

- Momentive Performance Materials Quartz Inc.

- Solvay

- U.S. Silica Holdings, Inc.

- PPG Industries

- Merck

- BASF

The silicon dioxide market is projected for a profitable expansion during the forecast period. Key market players are investing in advanced manufacturing technologies and developing specialized forms of silicon dioxide for high-demand applications. Strategic mergers and partnerships indicate competitiveness within the market as companies seek to strengthen their supply chains. Furthermore, businesses are seeking to expand to emerging markets to increase revenue shares.

Here are some key players in the silicon dioxide market:

Recent Developments

- In July 2024, U.S. Silica Holdings, Inc. announced completion of transaction to be acquired by Apollo Funds for USD 1.86 billion. The Company will continue to operate under the U.S. Silica name and brand, and an affiliate of Apollo Funds acquired all of the outstanding shares of U.S. Silica stock while the shareholders are entitled to receive USD 15.50 per share in cash for each share of U.S.

- In May 2024, Covia completed the acquisition of R.W. Sidley’s Industrial Minerals Division, which provides high-quality, silica-based products for use in filtration, industrial, and sports applications. Through the acquisition, Covia expands its portfolio of industry-leading products.

- Report ID: 6832

- Published Date: Sep 18, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Silicon Dioxide Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.