OUR GEOGRAPHIC COVERAGE

Research Nester examines and analyzes data from diverse sources like surveys, interviews and market research studies in order to grasp the latest market trends and customer preferences. This information is then utilized to generate reports that offer valuable insights, into Latin American markets. These reports

Latin America (Mexico, Argentina, Rest of Latin America)

Latin America continues to demonstrate resilience and reinvention by balancing macroeconomic stability with inclusive growth ambitions. The economic development for the overall region is based on its growth projections, with an estimated rise in the gross domestic product (GDP) by 2.4% as of 2025, and an expected 2.3% by the end of 2026. The region’s moderate economic performance is expected to reflect in the labor industry’s restricted dynamism, with an increase in the number of employed persons by 1.5% as of 2025, along with an expected rise by 1.2% as of 2026. In the international context, Mexico and Argentina remain among the world’s largest economies by GDP in 2023, anchoring regional demand and supply chains.

Mexico

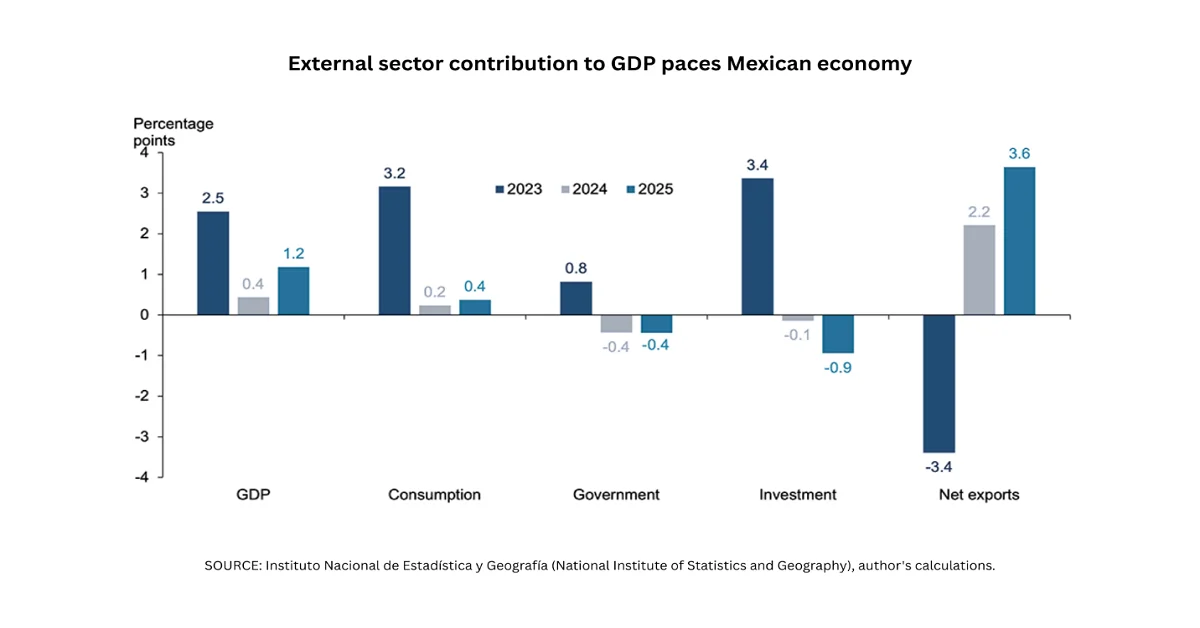

Mexico’s economy has a massive potential for growth and expansion, with a 1.8% growth during the first half of 2025. Based on this, there has been a reflection on the external sector performance, preferably net exports readily contributing 3.6% points to year-over-year (YoY) growth in terms of the GDP. Recently, the U.S. declared a 90-day extension to the present arrangement under which products from Mexico are taxed at 25% unless they are readily compliant under the USMCA, permitting them to enter duty-free. Besides, approximately 76% of imports from the country have entered under USMCA provisions, denoting a 50% rise.

Banking and Financial Services

Mexico’s banking and financial services sector remains a cornerstone of its economy, contributing significantly to GDP and supporting investment flows. In this regard, the non-performing loan ratio of the customer portfolio caters to 69% of commercial bank services, followed by 18% of regulated entities, 11% of non-regulated entities, and 2% of Infonacot. Meanwhile, the non-performing loan ratio of the mortgage portfolio accounts for 50% of Infonavit, followed by 39% of commercial banking, 10% of Fovissste, along with 0.4% each for regulated and non-regulated entities. Moreover, the overall financing of private non-financial organizations constitutes 73% of domestic sources and 27% of international sources. Based on this, the portfolio growth by organizational size caters to 86% of large-scale companies and 14% of small-scale companies.

Mexico comprises a huge space for optimizing the financial depth and enhancing the accessibility to finance. However, the access to financial services is effectively unequal across gender and income levels, as well as between urban and rural locations. If 92% of the adult population has access to a financial institution, across a few states, this is significantly lower and reaches only 77% in Puebla, 62% in Tlaxcala, and 56% in Oaxaca. Meanwhile, nearly 98% of the regional population has suitable access to a financial point, with 94% in Yucatan, 93% in Chiapas, and 81% in Oaxaca. However, the gender barrier still exists regarding accessibility to a few financial services, including retirement savings.

Government Investment and Policies

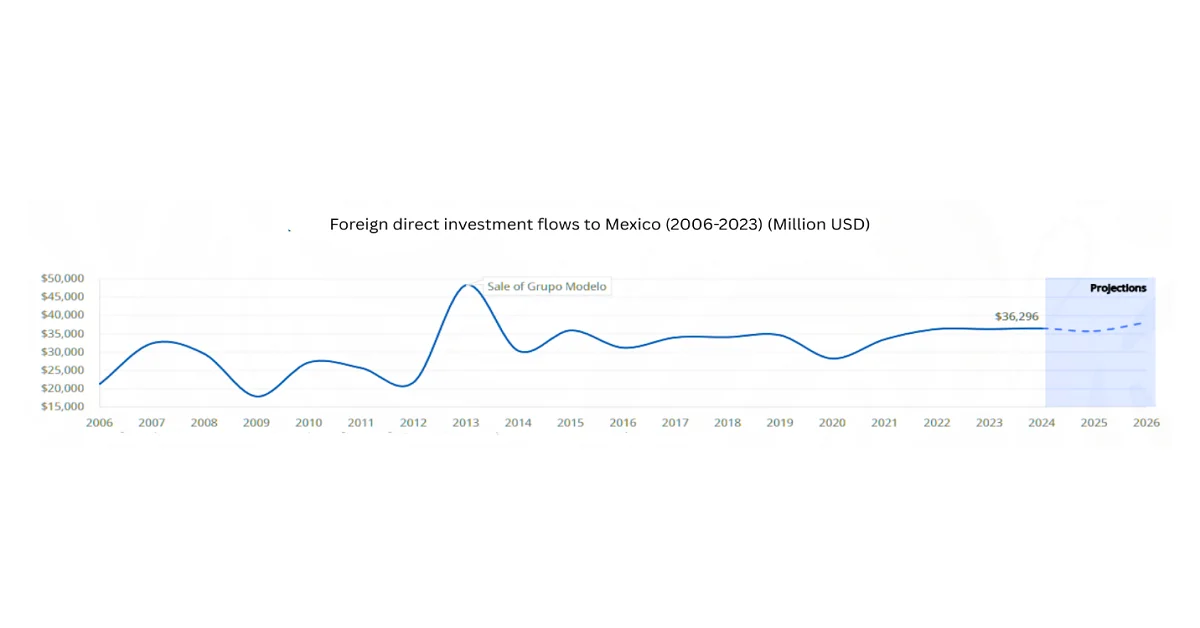

Mexico is the U.S.’s second-largest export industry in goods and services, and it is one of the most essential investment partners. The U.S. is the country’s top source of foreign direct investment (FDI), with a stock worth USD 283.8 billion as of 2023. There has been an increase in export facilities to the U.S. by 6.4% as of 2024 in comparison to 2023. Likewise, the inflation rate has been moderated, ending at 4.2% in 2024, mildly surpassing the Central Bank of Mexico’s (Banxico) target of 2% to 4%. Besides, the government’s allocated budget for 2025 aimed at narrowing down the fiscal deficit from 5.9% of the GDP in 2024 to 3.9% in 2025. Further, in October 2024, the President significantly signed a constitutional decree that redefined state-owned energy organizations, including Pemex and CFE as public enterprises to provide them with standard treatment in the country’s energy sectors.

Moreover, the decrease in the government’s fiscal deficit has created a positive impact on the country’s economic growth, thereby lowering borrowing demands from MXN 1.9 trillion to MXN 1.4 trillion. Besides, the total trade surpassed USD 1 trillion, with exports to the U.S. accounting for 83% of non-oil products and automotive products making up 35.7% of manufacturing exports. Meanwhile, FDI inflows to the country by economic industry amount to USD 103,102 million for industrial, USD 72,008 million for services, USD 15,900 million for extractive, USD 10,931 million for commerce, and USD 1,099 million for agriculture. Therefore, by the end of 2024, the nation recorded FDI of USD 36,872 million, representing a 2.3% rise from 2024.

Sectorial Analysis

The manufacturing sector is the backbone of exports in Mexico, and services are expanding through tourism and finance, while agriculture is continuing to offer rural employment but witnesses import and climatic risks. In 2022, there has been a deficit of USD 24 billion for advanced manufacturing products, which is indicative of the nation’s high dependence on imports. However, country-based imports of advanced manufacturing products are gradually increasing every year by 6.2%, and the U.S. has an estimated 47% share in the country’s market for associated equipment, robots, and sensors. Moreover, domestic orders for advanced manufacturing products have witnessed a yearly growth rate of 8% in 2022, and therefore the boosting demand for these products is regarded as the nearshoring trend in the overall country, with complex technological processes, along with technological innovation adoption.

In terms of the education and training service industry, Mexico comprises 7,738 students at the undergraduate level, denoting a 6.0%, along with 4,412 at the graduate level, which is 16.5%, 651 students at non-degree or other, and 1,699 for optional practical training. For uplifting the overall industry, the 100,000 Strong in the Americas (100K) Innovation Fund is considered one of the most successful regional programs. Based on this, 20 states in Mexico readily benefit from the program. As part of the U.S.-Mexico Bilateral Forum on Higher Education (FOBESII) initiatives for institutional collaboration, the U.S.-Mexico Program for the Internationalization of the Curricula, significantly executed by the Mexico-based Association for International Education (AMPEI), effectively supports faculty course development to offer students in both Mexico and the U.S. with global virtual exchange experiences.

Argentina

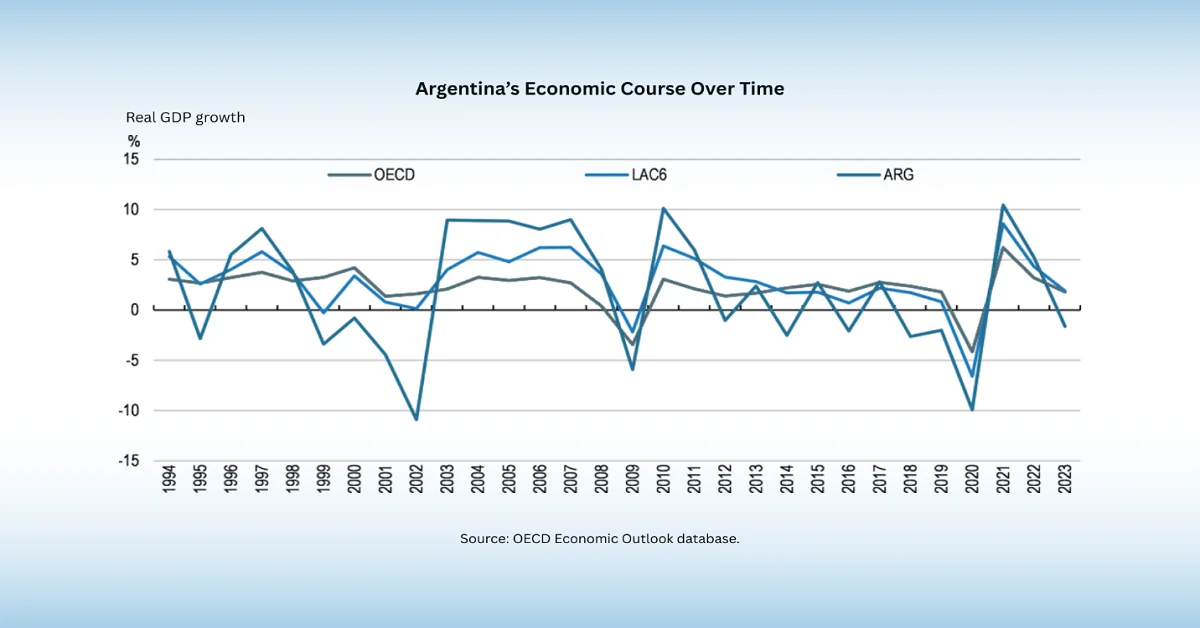

Argentina remains the third-largest economy in Latin America, with GDP accounting for 5.2% in 2025, and an expected 4.3% in 2026. In addition, the private consumption denoted a rise, with 9.6% in 2025, in comparison to 1.0% in 2023, and is further expected to be 3.8% in 2026. Besides, governmental consumption catered for 2.1% in 2023, with a projected 0.5% in 2026, and meanwhile, goods and services exports constituted an increase in its growth by 42.1% in 2025. Additionally, the consumer price index was 133.5% in 2023, which further increased to 219.9% in 2024, and the account balance of the country is expected to be 0.1% in 2026. Apart from these, the primary fiscal surplus reached 1.8% of the GDP in 2024, denoting a suitable turnaround from the 2.9% deficit that was witnessed in 2023.

Abundant Agricultural Production

Argentina is regarded as the world’s third-largest food exporter, with the agricultural industry constituting 15.7% of the GDP, along with 10.6% of tax revenues. Therefore, maintaining the international competitiveness of the country’s agri-food industry is regarded as the key to investing generously in the nation’s economic sustainability. The country’s food export is valued at USD 34,836 million, and significantly comprises 334,000 farms, of which 251,000 are owned by families. Besides, these 172,000 family farms do not comprise suitable resources, including capital or land, for making a standard living from the overall production. Therefore, to safeguard family farmers, solutions, such as the provision of social protection programs, promoting vertical and horizontal value chain integration, and ensuring the role of women in the overall industry’s workforce, providing support for their technical abilities in marketing, management, and production.

Farmers in Argentina are required to cope with a decrease in rainfall, extreme weather conditions, and long-lasting drought, which is expected to create a hindrance in the country’s overall GDP between 3% to 17%. Therefore, due to this situation, the agriculture industry is readily seeking to adapt to and incorporate the newest technologies to optimize water conservation and irrigation efforts. Besides, the country readily boasts more than 39 million hectares, which is 96 million acres, of cultivated land for farming and ranching. In addition, the cultivated areas of the country are further categorized into 3 zones, namely arid, accounting for 52.2%, followed by 27.7% of humid, and 18.1% of semi-arid, with both the semi-arid and arid zones comprising the potential to expand the overall agricultural frontier.

Governmental Analysis

The economy in Argentina comprises a turbulent history, which is characterized by a series of boom-bust cycles, with fiscal accounts causing a return of economic instability and an increase in inflation by 200% as of 2023. Besides, there has been a surplus for the majority of 2024, with the primary fiscal surplus reaching 1.8% GDP in 2024, thereby denoting a significant turnaround from the 2.9% deficit witnessed in 2023. Moreover, the headline fiscal balance has reached a small surplus of 0.3% of the GDP, indicating a 4.9%-point improvement since 2023.

Furthermore, the latest IMF-expanded Fund Facility program of USD 20 billion, along with an upfront disbursement of USD 12 billion as of April 2025, thus bolstered global reserves and permitted the government to uplift almost all remaining capital and currency controls. At the same time, the newest exchange and monetary rate regime has been successfully unveiled for enhancing the rate flexibility. This particular regime is projected to strengthen economic sentiment, medium-term growth, and private investment facilities, while also supporting suitable international reserve accumulation and readily improving resilience to external shocks.

Rest of Latin America (Brazil, Colombia, Chile, Peru, and others)

The broader Latin America region encompasses nations such as Brazil, Colombia, Chile, Peru, and several others. In recent years, these economies have demonstrated steady progress, driven by commitments to sustainable development and innovation. Their expansion has been supported by political stability, attractive business conditions, and the presence of a capable workforce. For the purpose of this presentation, our focus will be on examining the GDP trajectories of Brazil, Colombia, Chile, and Peru, which are four of the most influential economies shaping the region’s growth.

Brazil

Brazil remains the largest economy in Latin America and the ninth largest globally. It is home to 105.3 million people, with the real GDP per capita of USD 10,616, and also spans 8.5 million km2, with the presence of sharp contrasts. The overall GDP growth effectively reached 3.0% in 2023, but gradually slowed down to 1.8% in 2024. Besides, the private investment and consumption are expected to grow at a moderate pace, accounting for 4.3% in 2022, followed by 2.8% in 2023, and 2.1% in 2024.

Colombia

Colombia, the fourth-largest economy in Latin America after Mexico, Argentina, and Brazil and has maintained a diversified economic structure encompassing agriculture, manufacturing, services, and natural resources such as oil, coal, and gold. The country’s economy is projected to grow by 2.8% in 2026, along with 2.9% by the end of 2027. Investment is expected to resume with its partial and gradual recovery. Besides, inflation is projected to fall, but remain constant above the 3% target throughout 2027. Meanwhile, the fiscal consolidation is anticipated to resume, and fiscal deficits are expected to stay above 4% of the nation’s GDP.

Chile

Chile remains one of Latin America’s most stable and open economies, with a strong reliance on mineral extraction, agriculture, and services. The nation’s GDP development accounted for 2.4% as of 2025, and is further predicted to be 2.2% in both 2026 and 2027. There will be moderate consumption growth, readily supported by a rise in real incomes and employment. Additionally, net exports are expected to contribute positively to growth between 2026 and 2027. Moreover, the headline inflation is continuing to diminish and is projected to account for 3% by the end of 2026, and thereafter is expected to stabilize. Besides, the real GDP aspect in the country readily grew by 1.6% in 2025, supported by localized demand, which extended by 5.8% year-on-year (YoY).

Peru

Peru’s economy is heavily reliant on mining, petroleum extraction and refining, manufacturing, and agriculture, with services steadily expanding. Its GDP grew by 3.1% as of 2025, and is further anticipated to be 2.8% in 2026, which is followed by 2.7% by the end of 2027, amidst global uncertainty and increased domestic challenges. An upsurge in copper prices, a low inflation rate, regulatory simplification, and new infrastructure projects are suitable for supporting domestic consumption, international exports, and investments. Besides, inflation is predicted to be targeted by central banks at 2%. Furthermore, the aspect of private consumption readily benefited from a robust labor market and high real incomes, and meanwhile, private investment surged by 9.0% year-on-year (YoY), thereby reflecting optimized business sentiment, newly awarded public and private partnership contracts, and suitable financial conditions.

Role of The Research Nester in Guiding Market Players:

Research Nester has supported both emerging and established businesses in understanding the complexities of the market. By providing valuable insights into regional prospects, we have enabled companies to identify and capitalize on growth opportunities, ensuring that organizations can maximize their potential in highly competitive environments.