Ovarian Cancer Drugs Market Outlook:

Ovarian Cancer Drugs Market size was valued at USD 3.6 billion in 2025 and is expected to reach USD 7.22 billion by 2035, registering around 7.2% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of ovarian cancer drugs is evaluated at USD 3.83 billion.

Ovarian cancer (OC) was identified as the 3rd most common gynecological malignancy in the world, with a potential to register a notable rise in mortality by 2040, as per NLM. Another GLOBOCON statistical report revealed that the incidences of this condition across the globe are expected to grow by 42.0% from 2020 to 2040. Subsequently, the high expectancy and death cases are increasing the demand in the ovarian cancer drugs market. The surge is also driven by the worldwide presence of risk factors such as an aging population and environmental influences. According to the projections from a United Nations report, around 54.0% of the global habitats aged 65 and over are predicted to be female by 2050. These figures signify the need for early diagnosis and treatment to prevent widespread illness.

The efforts to make solutions from the ovarian cancer drugs market more accessible in every country is pushing companies to follow a standard range of payers’ pricing. In addition, the extended insurance coverage and subsidiary government policies are playing a crucial role in making required therapies more cost-effective. In this regard, a 2022 NLM study presented an overview of expenditure on such patients having reimbursement accommodations. It concluded that the monthly cost of prescribed PARP inhibitors, including niraparib, olaparib, and rucaparib, ranged between USD 13.0 and USD 15,000.0, where commercially insured beneficiaries were covered for a median total of USD 13,342.0. This embarks on the needed priority of affordability and availability in the market.

Key Ovarian Cancer Drugs Market Insights Summary:

Regional Highlights:

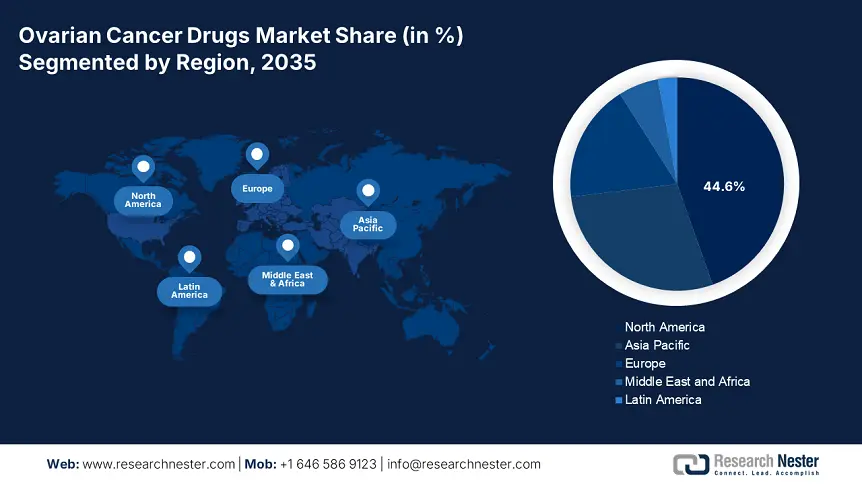

- North America leads the Ovarian Cancer Drugs Market with a 44.6% share, driven by a favorable regulatory framework and the presence of global leaders increasing medicine availability, ensuring significant growth by 2035.

- Asia Pacific's Ovarian Cancer Drugs Market is poised for rapid growth from 2026–2035, driven by continuous pharmaceutical expansion and enlarging patient pool in the region.

Segment Insights:

- The Targeted Therapy segment is set to lead the market from 2026-2035, driven by personalized diagnosis, therapeutics preferences, and FDA approvals in ovarian cancer care.

- The Hospital Pharmacy segment of the Ovarian Cancer Drugs Market is forecasted to hold a 57.40% share by 2035, driven by a large network of consumer bases and heightened expenditure on hospital pharmacies.

Key Growth Trends:

- Extensive use of drugs in OC detection

- Use of tech-based modules in drug development

Major Challenges:

- Unavoidable adverse reactions of medications

- Delay in diagnosis and product launches

- Key Players: GlaxoSmithKline plc, Pfizer, Eli Lilly and Company, Johnson & Johnson, Verastem Oncology.

Global Ovarian Cancer Drugs Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.6 billion

- 2026 Market Size: USD 3.83 billion

- Projected Market Size: USD 7.22 billion by 2035

- Growth Forecasts: 7.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (44.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, Germany, United Kingdom, France, Japan

- Emerging Countries: China, India, Brazil, Mexico, Russia

Last updated on : 12 August, 2025

Ovarian Cancer Drugs Market Growth Drivers and Challenges:

Growth Drivers

- Extensive use of drugs in OC detection: Besides the utility in combination therapies and as adjuvants, the ovarian cancer drugs market offers a wide range of medicines to assist in diagnosis. With the rising awareness about the importance of early identification to attain the best outcomes, more biomarkers are being internationally recognized, creating new opportunities for this sector. For instance, in November 2021, Cytalux (pafolacianine) received approval from the FDA to be a crucial part of molecular imaging for ovarian lesions. The formulation is specifically designed to help surgeons distinguish the malignant tissues, enabling them with an ability to detect the extensive spread of cancerous cells.

- Use of tech-based modules in drug development: Advancements in laboratory operations and tools are propelling the pace of development in the ovarian cancer drugs market. To combat the resistant mutational characteristics of malignant tissues, companies are adopting technological revolutions. For instance, in May 2024, Oregon Therapeutics participated in an AI-driven collaboration with Lantern Pharma to accelerate its progress in creating a new potent inhibitor, XCE853. The partners upscaled their AI capabilities to make this drug candidate a suitable option for a wide range of cancers, including OC. These innovations are procuring new possibilities for global leaders in this field.

Challenges

- Unavoidable adverse reactions of medications: The effectiveness of the offerings from the ovarian cancer drugs market are majorly evaluated on the basis of patient adherence. However, there are several events of toxicity and side effects, which often discourage residents from enrolling for these treatments. This also impacts the process of full-fledged commercialization due to these limitations in wide acceptance. Consequently, it hinders the profit margins and scale of revenue generation.

- Delay in diagnosis and product launches: The outcomes from the use of medicines available in the ovarian cancer drugs market highly depend on the severity and stage of the condition. On the other hand, a lack of awareness about symptoms and promotional campaigns, particularly in underserved regions, results in late detection. This makes it hard for these therapies to showcase their full potential in treating OC, shrinking the reach and exposure of this sector on a global scale.

Ovarian Cancer Drugs Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

7.2% |

|

Base Year Market Size (2025) |

USD 3.6 billion |

|

Forecast Year Market Size (2035) |

USD 7.22 billion |

|

Regional Scope |

|

Ovarian Cancer Drugs Market Segmentation:

Distribution Channel (Drug Stores & Retail Pharmacy, Hospital Pharmacy, Online Pharmacy)

Hospital pharmacy segment is likely to account for ovarian cancer drugs market share of around 57.4% by 2035. These organizations are some of the biggest investors in this field due to having a large network of consumer bases. This is further testified by the heightened expenditure on hospital pharmacies. On this note, an NLM article stated that 20-50% of the third-party pharmaceutical spending in Europe goes to these distributors. It also highlighted that hospital PE (pharmaceutical expenditure) accounted for 55.9% of the nationwide PE in the UK in 2020. Furthermore, with dedicated specialty departments and in-built pharmaceutical supply houses, hospitals have become the 1st point of connection for both manufacturers and patients.

Therapy (Chemotherapy, Immunotherapy, Targeted Therapy, Hormonal Therapy, Radiation Therapy, Others)

In terms of therapy, the targeted therapy segment is predicted to hold the largest share in the ovarian cancer drugs market throughout the forecasted timeline. The precise and specific kinetics of these therapies are the most attractive properties for OC care, which is shifting consumer preference towards the personalized approach of diagnosis and therapeutics. For instance, in January 2025, the FDA allowed the use of Avutometinib + Defactinib as a targeted therapy for KRAS mutant low-grade serous ovarian cancer. The decision was based on the results from phase 2 RAMP 201 and phase 1 FRAME trials. The emphasizing industry of precision oncology, which is poised to attain USD 116.5 billion by 2025 and USD 411.9 billion by 2035, is also evidence of this growth factor in this segment.

Our in-depth analysis of the global ovarian cancer drugs market includes the following segments:

|

Distribution Channel |

|

|

Therapy |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Ovarian Cancer Drugs Market Regional Analysis:

North America Market Analysis

North America ovarian cancer drugs market is expected to capture revenue share of over 44.6% by 2035. The region is home to several global leaders such as AbbVie, Johnson & Johnson, Eli Lilly and Company, Pfizer, and others. This has diversified the product line of this sector, increasing the availability of medicines and securing a good flow of business. The favorable regulatory framework is also an influential factor for these drug developers. For instance, in March 2024, AbbVie gained approval from the FDA for manufacturing and marketing its ELAHERE (mirvetuximab soravtansine-gynx), treating folate receptor alpha (FRα)-positive, platinum-resistant epithelial OCs. Moreover, their effort to develop innovative therapies is bringing new options and business opportunities to this field.

The U.S. presents a pre-established and lucrative trading environment for the ovarian cancer drugs market with a wide network of distribution channels. The country proactively supports and invests in the continuous upgrading of healthcare systems, allowing advanced solutions to streamline. This attracts both domestic and international leaders to participate. In addition, the country consists of a highly prone female population, among which 20,890 and 12,730 are predicted to be diagnosed with and deceased due to ovarian cancer by 2025: America Cancer Society. This is cultivating a surge in more personalized and effective curatives, fueling growth in this sector.

Canada is affiliating innovation in the ovarian cancer drugs market with its government fundings and academic excellence. Research institutions across the nation are drafting a cohort of R&D by discovering new development platforms and evaluation standards. For instance, in June 2023, researchers at the University of Saskatchewan introduced a clinical trial to identify new drug classes, evolving the pathway of OC treatment in Canada. This launch was backed by a total fund of USD 3.8 million, incorporating a USD 1.1 million grant from Genome Canada. Furthermore, the country is escalating its pace of innovation by fueling its genome sequencing industry with continuous financial support.

APAC Market Statistics

Asia Pacific is poised to register the fastest growth in the ovarian cancer drugs market during the analyzed timeframe. Continuous pharmaceutical expansion and enlarging patient pool are the two major growth factors of this region’s progression. Emerging landscapes in precision medicine, such as Japan, China, and India, are propagating with their greater capabilities in R&D and clinical trials. This has dragged the focus of many global leaders and inspired them to invest in this marketplace. For instance, in August 2023, AstraZeneca and Merck conjugately earned MHLW clearance for using the combination of LYNPARZA, Abiraterone, and Prednisolone to cure BRCA-mutated (BRCAm) castration-resistant prostate cancer with distant metastasis (mCRPC) in Japan.

India is one of the forefront holders in the cohort of innovation in the ovarian cancer drugs market. The country is witnessing a significant emergence in its biopharmaceutical industry to become the world’s biggest medicine supplier. Despite economic disparities, this landscape is producing more effective and affordable therapies at a notable pace with the help of government initiatives and heavy private investments. Thus, the profitable atmosphere of India is procuring new pioneers in this merchandise. For instance, in July 2024, Lupin Limited attained an Abbreviated New Drug Application allowance from the FDA for its Doxorubicin Hydrochloride Liposome Injection. Its 20 mg/10 mL and 50 mg/25 mL single-dose vials are intended to treat OCs.

China is augmenting the ovarian cancer drugs market with its strong emphasis on precision medicine and clinical trials. In this cohort, the government of this country has played a crucial role by investing in extensive R&D and expanding pharmaceutical capacity. For instance, the Pan-China 13th Five-Year Plan (2016–2020) highlighted the USD 9.0 billion contribution of the national government to precision medicine R&D. Such capital influx inspires both global and domestic pioneers in this field to cultivate tailored product lines for this country. Furthermore, the magnifying focus on improving healthcare accessibility and drug delivery is fostering a progressive environment for this merchandise.

Key Ovarian Cancer Drugs Market Players:

- Genentech Inc.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- GlaxoSmithKline plc

- Roche

- Johnson & Johnson

- ImmunoGen

- Janssen Pharmaceuticals, Inc.

- Eli Lilly and Company

- Pfizer

- Verastem Oncology

Key players in the ovarian cancer drugs market are proactively expanding their territory for globalization. For instance, in November 2024, AbbVie attained marketing rights for ELAHERE from the European Commission to expand its reach overseas. They are involved in the cohort of rigorous R&D to develop more effective targeted therapies for better outcomes and wide adoption. For instance, in July 2024, Shorla Oncology received a New Drug Application (NDA) allowance for its ready-to-dilute formulation, TEPYLUTE, from the FDA. The injectable therapeutic is designed to offer accuracy while targeting the malignant cells in the ovary, mitigating the complexity and volatility in disease management. Such key players are:

Recent Developments

- In January 2025, Verastem completed a new credit facility of up to USD 150.0 million and an equity investment of USD 7.5 million in collaboration with Oberland Capital. Additionally, the company partnered with IQVIA to strengthen the commercialization of avutometinib + defactinib for recurrent KRAS mutant low-grade serous ovarian cancer.

- In December 2024, GlaxoSmithKline revealed promising results from the FIRST-ENGOT-OV44 phase III trial on Zejula (niraparib) and Jemperli (dostarlimab). The combination showcased a significant reduction in ovarian cancer progression and enhancement in survival, with or without bevacizumab.

- Report ID: 7440

- Published Date: Aug 12, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Ovarian Cancer Drugs Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.