Surgical Blade Market Outlook:

Surgical Blade Market size was over USD 218.57 million in 2025 and is projected to reach USD 359.43 million by 2035, growing at around 5.1% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of surgical blade is assessed at USD 228.6 million.

The primary growth driver of the surgical blade market is the rising prevalence of chronic diseases such as cardiovascular diseases, diabetes, and cancer which often necessitate surgical interventions, driving demand for surgical blades. According to the United States Department of Health and Services, an estimated 129 million people in the U.S. have at least one major chronic condition (heart disease, cancer, diabetes, obesity, or hypertension).

Moreover, older adults often require surgeries for age-related health conditions, including orthopedic issues (hip or knee replacements), and cataracts. This creates a steady demand for surgical tools including blades. Aging populations also encourage governments and healthcare providers to expand infrastructure and services, further driving demand for surgical blades.

Key Surgical Blade Market Insights Summary:

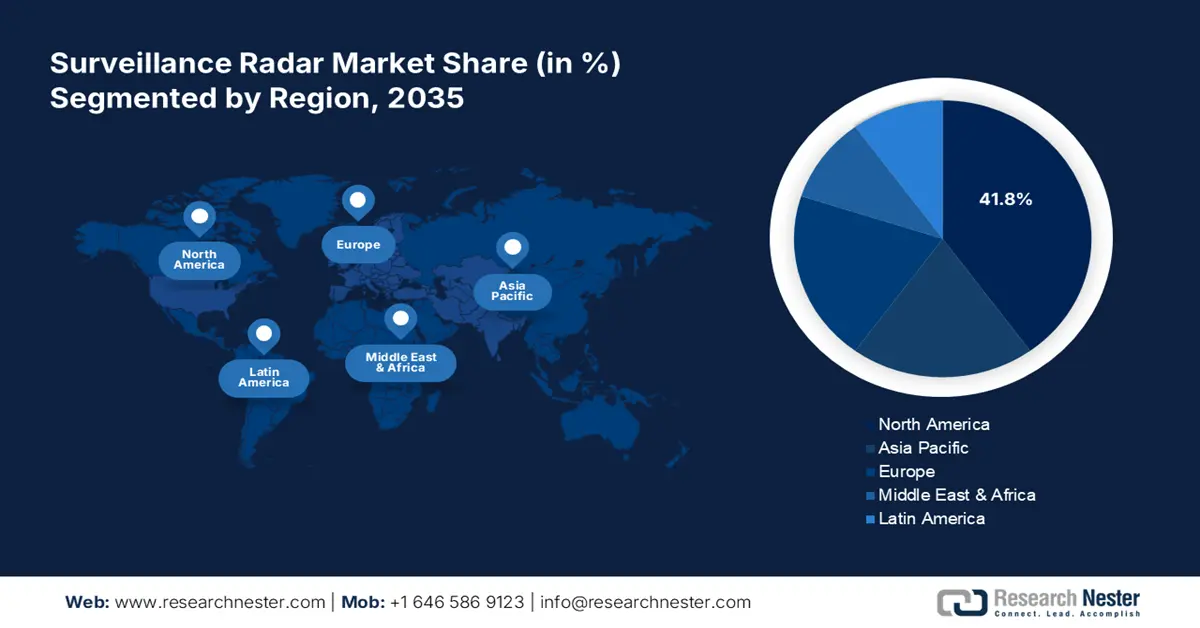

Regional Highlights:

- North America leads the surgical blade market with a 38.2% share, driven by high surgical volumes, advanced healthcare systems, and innovation, fostering growth through 2026–2035.

Segment Insights:

- The Stainless Steel segment is anticipated to hold a significant share by 2035, driven by its strength, durability, and corrosion resistance for surgical applications.

- The Sterile segment is expected to secure a 77.4% share by 2035, driven by increasing demand for sterile surgical blades due to heightened hygiene awareness and growing surgical procedures worldwide.

Key Growth Trends:

- Rising adoption of minimally invasive surgery (MIS)

- Technological advancements

Major Challenges:

- High competition and price pressure

- Risk of infections and complications

- Key Players: Johnson & Johnson Service, Inc., Conmed Corporation, Integra LifeSciences, Smith & Nephew, Becton, Dickinson and Company (BD), and B. Braun Melsungen Ag.

Global Surgical Blade Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 218.57 million

- 2026 Market Size: USD 228.6 million

- Projected Market Size: USD 359.43 million by 2035

- Growth Forecasts: 5.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.2% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: China, India, Japan, South Korea, Brazil

Last updated on : 14 August, 2025

Surgical Blade Market Growth Drivers and Challenges:

Growth Drivers

- Rising adoption of minimally invasive surgery (MIS): MIS techniques require surgical blades that are highly precise and tailored for smaller incisions. Increased adoption of MIS for procedures in cardiology, orthopedics, gynecology, urology, and general surgery contributes to the steady growth of the surgical blade market. This trend is particularly notable in developed and emerging economies where healthcare infrastructure is evolving. According to a 2024 report on global cardiac surgical volume, more than 1 to 1.5 million cardiac surgical procedures are estimated to occur yearly.

Moreover, disposable surgical blades are used in MIS to maintain sterility and prevent cross-contamination. This shift toward single-use products accelerates surgical blade market growth, especially in infection-sensitive environments. - Technological advancements: Developing high-quality materials like stainless steel and carbon steel ensures durability, sharpness, and corrosion resistance. Coatings like diamond-like carbon (DLC) and ceramic coatings enhance cutting efficiency and reduce soft tissue injuries. Modern surgical blades feature ergonomically designed handles and grip mechanisms for improved control and reduced fatigue during long procedures.

Blades designed for laparoscopic robotic-assisted, and other minimally invasive procedures ensure precision in confined surgical spaces. Thin, flexible, and micro-sized blades are increasingly in demand for delicate procedures. Moreover, smart technologies, such as sensors, can be integrated to monitor tissue resistance or provide real-time feedback to surgeons during procedures. - Rising cosmetic and aesthetic procedures: Procedures such as facelifts, liposuction, and rhinoplasty are becoming more common due to growing societal emphasis on appearance and self-confidence. This rise in demand drives the need for precision surgical instruments, including high-quality surgical blades, to ensure optimal results. According to the British Association of Aesthetic Plastic Surgeons, Women underwent 93% of all cosmetic procedures recorded in 2022, a rise of 101% from 2021.

Aesthetic procedures like micro-needing, dermabrasion, and skin resurfacing often require surgical blades for fine and accurate incisions. Specialized blades tailored for minimal scarring and precise cuts are in high demand.

Challenges

- High competition and price pressure: Intense competition among manufacturers leads to price wars, affecting profit margins and discouraging investment in innovation. Low-cost alternatives from unregulated surgical blade markets can undercut established players, impacting the quality perception of surgical blades.

- Risk of infections and complications: Improper handling or use of reusable surgical blades can lead to infections or cross-contamination, impacting their adoption in certain settings. Safety concerns may drive healthcare facilities to explore alternative technologies.

Surgical Blade Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

5.1% |

|

Base Year Market Size (2025) |

USD 218.57 million |

|

Forecast Year Market Size (2035) |

USD 359.43 million |

|

Regional Scope |

|

Surgical Blade Market Segmentation:

Product (Stainless Steel and High-grade Carbon Steel)

By product, the stainless steel segment is predicted to dominate surgical blade market share of around 45.5% by the end of 2035. Stainless steel blades are known for their strength, durability, and resistance to corrosion, making them ideal for surgical applications. These properties ensure long-lasting performance and maintain sharpness during procedures. Stainless steel is highly compatible with various sterilization techniques, including autoclaving and chemical treatments, ensuring safe and repeated use without compromising quality. This is crucial in reducing surgical site infections, a priority in modern healthcare.

Additionally, surgical blades made from stainless steel provide superior precision and consistent sharpness, which are critical for complex surgical procedures, including cardiovascular and neurosurgeries. Stainless steel surgical blades are used in diverse medical fields such as general surgery, dermatology, and orthopedics, due to their adaptability to various blade designs and configurations.

Material (Sterile and Non-Sterile)

In surgical blade market, sterile segment is anticipated to hold revenue share of more than 77.4% by 2035. Sterile surgical blades are individually packaged and pre-sterilized, reducing the risk of cross-contamination and surgical site infections. With increasing awareness of hygiene in surgical environments, the adoption of sterile blades has become a standard practice globally. The growing number of surgeries both elective and emergency, has led to higher demand for sterile blades. This trend is particularly prominent in developed healthcare systems like those in the U.S., Europe, and Japan.

Furthermore, global healthcare regulations increasingly mandate the use of sterile medical instruments. For instance, ISO standards and guidelines by the World Health Organization (WHO) encourage the use of sterile equipment to prevent healthcare-associated infections.

Our in-depth analysis of the global surgical blade market includes the following segments:

|

Product |

|

|

Material |

|

|

End use |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Surgical Blade Market Regional Analysis:

North America Market Forecast

North America in surgical blade market is expected to dominate around 38.2% revenue share by the end of 2035. The growth of the market can be attributed to its advanced healthcare systems, high surgical volumes, and emphasis on safety and innovation. The region is a hub for medical innovations, with constant improvements in surgical blade materials and designs, such as laser-sharpened stainless steel blades and blades tailored for robotic-assisted surgeries.

The U.S. is experiencing significant growth, driven by a rising number of surgical procedures and the growing demand for high-quality medical equipment. Annually, the country records approximately 35 million hospital stays, many involving surgical interventions. For instance, about 350,000 coronary artery bypass graft (CABG) surgeries and 750,000 laparoscopic cholecystectomies are performed each year. These procedures rely heavily on precision instruments like surgical blades.

Also, the prevalence of chronic conditions such as cardiovascular diseases, obesity, and cancer is fueling demand for surgeries. As of 2022, over 18 million U.S. adults were reported to have coronary artery disease, with 70% undergoing surgical treatment.

In Canada the surgical blade market is poised for steady growth, driven by an increasing number of surgical procedures, rising healthcare expenditures, and the growing prevalence of chronic and lifestyle diseases. The country’s healthcare infrastructure is also expanding, supporting an increase in surgeries and medical treatments. The government is investing in healthcare services and technologies, further promoting market growth.

Europe Market Analysis

The surgical blade market in Europe is poised for steady growth, driven by the rising number of surgical procedures, advancements in healthcare technologies, and an aging population that requires increased medical interventions. The market has benefited from the growing demand for precision and safety in surgeries, which is propelling the need for high-quality surgical blades, particularly those made from materials like stainless steel and high-grade carbon steel.

In Europe countries like Germany, the UK, and France, are key contributors to the surgical blade market due to their strong healthcare infrastructure and significant medical research activities. The healthcare sector’s expanding focus on minimally invasive procedures is further boosting the demand for surgical blades. Moreover, the region’s regulations, ensuring high standards of sterilization and safety in medical devices, are promoting the growth of sterile surgical blades, which dominate the market segment.

Key Surgical Blade Market Players:

- Medtronic Plc

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Johnson & Johnson Service, Inc.

- Conmed Corporation

- Integra LifeSciences

- Smith & Nephew

- Becton, Dickinson and Company (BD)

- B. Braun Melsungen Ag

- Cadence Inc

- Integer Holdings Corporation

- Planatome, LLC

- Olympus Corporation

- Entrepix Medical, LLC

Key players in the surgical blade market are driving growth through several strategic initiatives that include product innovation, geographic expansion, strategic partnerships, and a strong focus on quality standards. These efforts not only expand the market but also ensure that surgical blades are integral to the advancements in modern surgical practices.

Here are some key players in the market:

Recent Developments

- In October 2020, Entrepix Medical, LLC, a medical technology firm focusing on adapting superior nano-polishing technology used in microchip manufacture to surgical instruments, announced the introduction of Planatome Technology. This proprietary technology results in a completely different, patient-focused surgical blade with an ultra-smooth, precise, and consistent cutting surface that significantly reduces surgically-induced tissue stress.

- In June 2020, Olympus, a global technology leader in inventing and delivering breakthrough solutions for medical and surgical procedures, announced the commercial availability of two single-use electrosurgical knives for Endoscopic Submucosal Dissection.

- Report ID: 6713

- Published Date: Aug 14, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Surgical Blade Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.