Silicon Dioxide Market Regional Analysis:

North America Market Insights

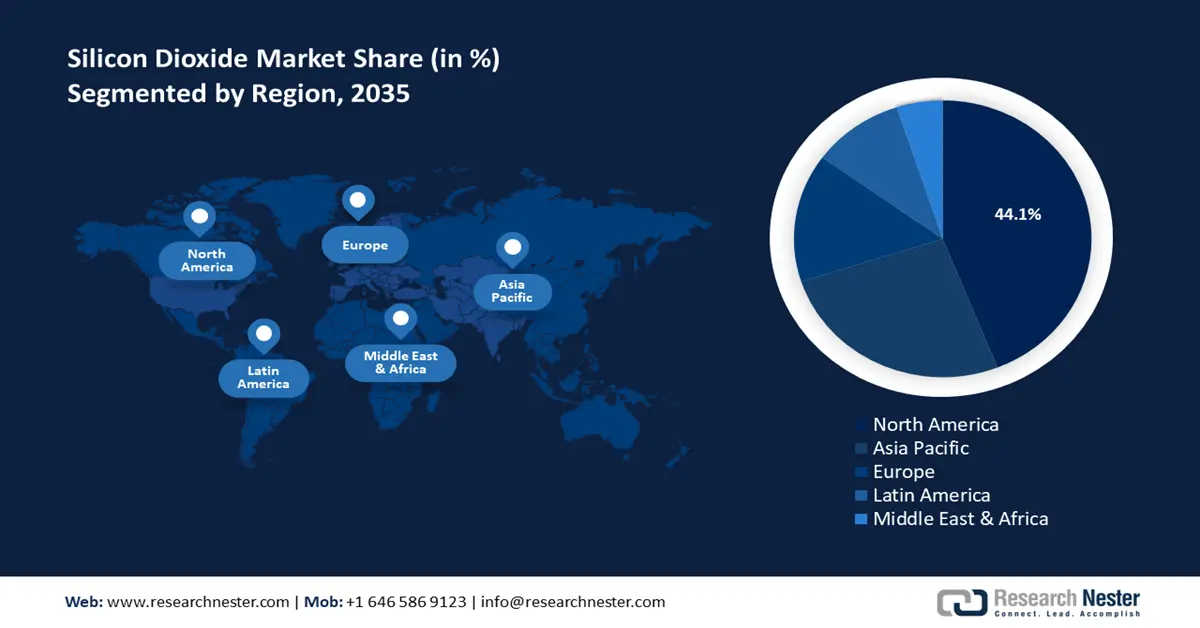

By 2035, North America silicon dioxide market is likely to account for around 44.1% share. The growth of the regional market is owing to rising investments by industry leaders to expand production capacity in the region, benefiting the regional supply chain and reducing downtimes. The U.S. and Canada dominate the region’s market share.

The heightened acquisition deals and portfolio expansions in North America are a major indicator of the profitability of the silicon dioxide market. For instance, in November 2023, the Sio Silica Corporation announced entering a definitive agreement with the Pyrophyte Acquisition Corporation., for a business combination that reflected an enterprise value of USD 708 million and equity value of USD 758 million. The combined business is poised to supply high-purity quartz silica which is a critical mineral in the global net zero transition.

The U.S. silicon dioxide market holds the largest revenue share in North America. The country’s supportive regulatory ecosystem for businesses has led to major players in the industry investing to expand the production of silica in the country. Additionally, the U.S. has cemented itself as a significant exporter of silica and quartz sands in the world, with the Observatory of Economic Complexity estimating exports worth USD 70.1 million and imports worth USD 2.79 million, resulting in a positive trade balance of USD 67.3 million. The surplus indicates strong domestic production capacity, ensuring a stable and reliable supply chain for end use industries that use silica in large quantities.

Furthermore, the rising demand for food-grade silica to be used as a stabilizer in beer production is a key driver of the market. The U.S. Brewer’s Association estimated the country’s beer industry at USD 117 billion, indicating profitable opportunities for food-grade silica suppliers.

Canada is exhibiting robust growth in the silicon dioxide market. The thriving mining industry of Canada provides a steady supply of high-purity silica, catering to diverse applications in the electronics and construction sectors in the country. Furthermore, Canada benefits from the presence of industry leaders such as Sio Silica Corporation and LaPrairie Group. Furthermore, Canada’s push to expand renewable energy production is poised to boost the manufacturing of solar panels that require silicon, and silicon dioxide remains a crucial early-stage component in silicon production.

Furthermore, expansion by companies in Canada to emerging markets is poised to benefit the domestic silicon dioxide sector. For instance, in November 2024, Homerun Resources Inc., reported the discovery of HPQ silica sand in multiple locations in Brazil, and the average drilling results are reported at 99.23% silicon dioxide. The successful drilling operation is expected to benefit the supply of high-purity silica from Canada.

APAC Market Insights

The APAC silicon dioxide market is poised to exhibit the fastest growth during the forecast period. The region’s revenue share is led by China and India. The booming industrialization and urbanization trends in APAC have heightened construction activities and contributed to increasing demand for silica in the construction sector. Additionally, led by China, India, and Japan, APAC has positioned itself as a hub of the semiconductor sector necessitating a steady supply of silica.

Global players are identifying the potential in the APAC silicon dioxide market, evidenced by acquisitions in the region. For instance, in October 2024, Momentive Technologies announced the acquisition of Sibelco’s spherical alumina and spherical silica businesses located in South Korea to strengthen its work on thermal fillers used in thermal interface materials (TIMs) and expand the ceramics powder product portfolio.

China registered a dominant revenue share in the Asia Pacific silicon dioxide market. The major driver of the market’s dominant share in China is the expansion of applications in end use industries. China is a global leader in the production of electronics and semiconductors, necessitating a constant supply of high-purity silicon dioxide. Furthermore, in September 2024, the Observatory of Economic Complexity estimated China’s silicon dioxide exports at USD 60 million and imports at USD 18.3 million, indicating a positive trade balance. With the country seeking to continue its establishment as a global powerhouse for crucial mineral exports, the domestic market within the country promises lucrative opportunities.

Additionally, companies from China are looking to expand the production line for silicon dioxide. For instance, in February 2023, Xinyi Solar Energy Holding Co., Ltd., announced plans of USD 3 million worth of investments in the silica sand mining operations in the Bangka-Belitung Islands of Indonesia.

India is expected to increase its revenue share in the APAC silicon dioxide market. A key opportunity for the market in India is to fill the supply chain gap that can occur due to rising geopolitical tensions between the U.S. and China, with the former banning the import of silica-based solar materials from the latter. This provides an opportunity for companies within India to increase their production to support the global supply chain, as well as for global companies to invest in India.

Companies in India are investing to increase production capacities to leverage the favorable market trends. For instance, in November 2023, Vesuvius expanded its operations by inaugurating alumina-silica (AlSi) and basic monolithic manufacturing facilities in the country. The development is in alignment with the ambitious Make in India goals of the country, which focuses on improving domestic manufacturing, and the government-backed incentives are beneficial to boost production lines in the country.