Silicon Carbide Market - Regional Analysis

North America Market Insights

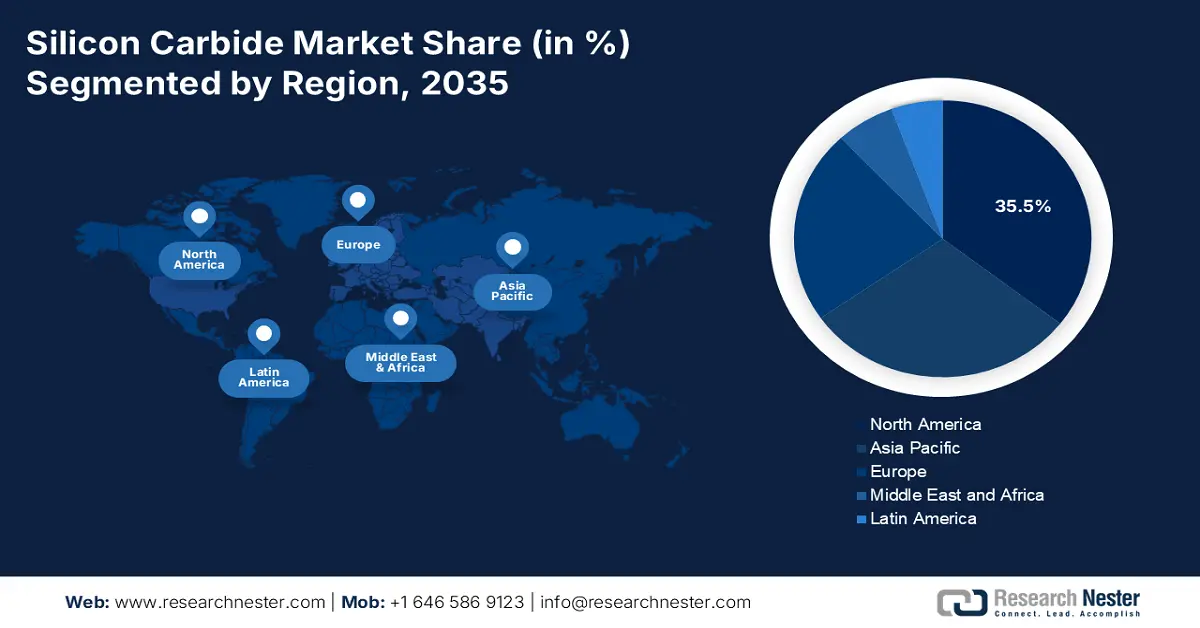

North America’s market is anticipated to grow with the largest revenue share of 35.5% during the forecast years from 2026 to 2035, attributed to governmental initiatives on high-technology materials, energy security, and sustainability of chemicals. Wide bandgap semiconductors, such as SiC, are formally identified as strategic technologies by the U.S. Department of Energy (DOE), and it emphasizes the capability of such materials to enable increased power density, shorter switching, and efficiency improvements in grid and transportation systems. Additionally, one of the largest drivers is federal funding, where in August 2022, DOE declared it would fund university and national laboratory activities in clean energy technology and low-carbon manufacturing at a sum of USD 540 million, with SiC research being one of the areas of emphasis in semiconductor innovation. There are also environmental regulations that push the regional SiC market by promoting sustainable chemical processes. The EPA Green Chemistry Challenge Program has documented various innovative technologies adopted in 2021, which have resulted in quantifiable reductions in hazardous waste and are in line with the safer chemical manufacturing practices in support of SiC wafer processing requirements.

Furthermore, the NIST report states that advanced metrology systems that have been developed to serve high-voltage, high-speed, SiC power devices, such as 10-kV MOSFETs with a continuous current of 2A (50A/cm 2) and 10-kV PiN diodes in operation with 40 A (80 A/cm 2), are selected to provide accurate performance and reliability test results. These criteria minimise the risk of commercialization and help to promote the increasing use of SiC in the energy transition of North America, electric vehicles, and industrial markets by facilitating powerful, efficient electronics of power. Together, these factors, including an increase in government spending on R&D, sustainability requirements, and adoption of SiC in new manufacturing and chemical development, are making North America a major growth centre in the global SiC market.

The U.S. market is projected to lead the North American region with the largest share by 2035, mainly driven by the federal laws and the technical standards promoting the growth of advanced power electronics. The CHIPS and Science Act of 2022 permitted the allocation of USD 52.7 billion to broaden domestic semiconductor capacity, where wide-bandgap semiconductor materials like SiC are also included in the research and manufacturing priorities. In addition, in direct response to decreasing the risk of commercialization by removing a barrier to manufacturers, the National Institute of Standards and Technology (NIST) is making progress in metrology programs to enhance the reliability and measurement standards of SiC devices. Moreover, crystalline silica, which is a major component in semiconductor processing, has imposed limiting exposure levels on the Occupational Safety and Health Administration (OSHA) of chemicals, so that safer manufacturing habits are adhered to. For instance, OSHA has imposed permissible exposure limits (PEL) of respirable crystalline silica, which stipulates a limit of 50 micrograms per cubic meter (µg/m³) of silica concentration in the air, which is to be allowed during an 8-hour work shift to make the manufacturing process in semiconductor processing and other industries safer. All these combines to have a robust federal funding, technical infrastructure, and workplace safety regulations as the U.S. pathway to leading the world in the adoption of SiC in industrial, automotive, and grid implementation.

The market in Canada is likely to expand steadily over the forecast years by 2035, owing to the robust clean technology innovation and advanced materials research by the federal government. In 2022-23, Natural Resources Canada has given out more than 350 energy innovation projects, some of which are advanced semiconductor and chemical process projects, which indirectly support SiC adoption with a budget of CAD 115 million. Sustainable manufacturing is also becoming a priority in Canada, as the 2030 Emissions Reduction Plan developed by the government is aimed at a 40% reduction of greenhouse gases by 2030, which will necessitate the usage of power electronics based on SiC in renewable energy and electrified transport. Additionally, the involvement of Canadians in international semiconductor alliances will guarantee access to important materials and technologies, thereby facilitating the adoption of the same domestically. With the added focus on clean-energy ambitions alongside strategic investment in research and development, Canada is establishing a solid base in SiC integration of the chemical and energy industries.

Asia Pacific Market Insights

The Asia Pacific market is expected to grow rapidly, with a revenue share of 29.8% during the projected years from 2026 to 2035, driven by the high demand for electric cars, renewable energy systems, and industrial power electronics. The wide-bandgap semiconductors, such as SiC, are being emphasized in regional energy and manufacturing strategies to enhance energy efficiency and greenhouse gas emissions reduction. For instance, according to the Congressional Research Service report, the Asia Pacific is at the forefront of the world semiconductor manufacturing scene with strong government-based investments in engineering materials such as silicon carbide (SiC) to improve power electronics to promote energy efficiency and electrification. The region comprises more than 70% of the worldwide capacity for semiconductor wafer fabrication, and semiconductor fabrication is used to propel the adoption of SiC in electric vehicles and the renewable energy industry. This is the leading role in production and long-term policy support, making the Asia Pacific play a significant role in developing the global SiC market.

Similarly, there has been a large growth in investment into the production of advanced materials and sustainable chemical processes, and, at the regional level, there are programs of investment in clean-energy adoption, practices in low-carbon industries, and high-efficiency power electronics. For example, the Asian Development Bank (ADB) has funded clean energy projects in Asia with a loan of USD 65 million to Nepal to support the energy access and efficiency improvement project, which installed 1000 solar-powered streetlights and distributed 1 million compact fluorescent lamps. The measures are expected to cut carbon dioxide emissions by 15,000-20,000 tons/year, indicating the regional investments in energy-efficient technologies and sustainable practices, which indirectly facilitate the adoption of silicon carbide in power electronics. Meanwhile, the metrology and device reliability standards are being developed in research institutions and standards bodies in the region, and the commercialization of high-performance SiC modules is accelerating.

By 2035, China’s market is likely to dominate the Asia Pacific region with a substantial revenue share, owing to significant investment in silicon carbide (SiC) technologies to boost its semiconductor and chemical sectors. In 2023, China made breakthroughs in 50 technologies dubbed as 50 foundations under the leadership of the State Council Information Office, such as the production of SiC. In addition, in the State Council of China National 13th Five-Year Plan, strategic emerging industries, such as new materials, such as silicon carbide (SiC), have priorities, and the scale of their industries will grow to more than 15% of GDP by the year 2020. The strategy aims to enhance the ability to innovate and create industrial clusters at the global scale in favor of the faster development of SiC as an important material in the Chinese semiconductor and clean energy industries. Additionally, the Ministry of Ecology and Environment is encouraging the use of green chemistry to cut the number of harmful wastes in the production of chemicals. This has been backed by heavy investment in research and development, making China a major player regarding the use of SiC in chemical processes.

The market in India is expected to grow with the fastest CAGR from 2026 to 2035, attributed to the growing introduction of silicon carbide (SiC) technology to the chemical industry via government policies. The India Semiconductor Mission (ISM) provides fiscal subsidies to project expenses of setting up SiC-related facilities, such as compound semiconductor fabrication plants and packaging units. For example, the government under ISM has approved 10 semiconductor projects in six states, with a total cost of about 1.60 lakh crore. Such projects include different semiconductor manufacturing processes such as fabrication, packaging, and testing. It is also worth noting that the ISM has contributed to the development of the first commercial-scale semiconductor plant in the country in Odisha, and it specializes in Silicon Carbide (SiC) technologies. Additionally, the government has spent 234 crores on chip design projects in 2025 that facilitated innovation in SiC applications. Moreover, the production of specialty chemicals has been growing steadily in the Department of Chemicals and Petrochemicals, and there has been a dramatic expansion of exports between the FY 2018-19 and FY 2022-23. These efforts indicate that India is increasingly concerned with the application of SiC technologies in order to make its chemical sector efficient and sustainable.

Europe Market Insights

The European market is projected to grow with a substantial revenue share of 22.7% over the forecast years, owing to the demand for electric cars (EVs), renewable energy systems, and the growth of power electronics. The research and innovation devoted to climate change and sustainable development, as well as sustainable chemical technologies, is funded by Horizon Europe, with an indicative budget of €93.5 billion in 2021-2027. This is a significant investment that supports the development of silicon carbide (SiC) technologies in the European power electronics and clean energy industries, which also strengthens the leadership of the continent in advanced semiconductor materials. Additionally, the European Chemicals Agency (ECHA) and the European Chemical Industry Council (CEFIC) have played a key role in establishing regulatory frameworks that promote the use of SiC in other industrial uses. Furthermore, the National Semiconductor Strategy by the UK government promises up to 2023-25 and up to £200 billion, and by 2030, a decade later, 1 billion to expand domestic semiconductor manufacturing, including in compound semiconductors such as silicon carbide (SiC). The investment helps the UK in its advantages in the field of R&D, design, and manufacturing in order to speed up the development of SiC in the fields of power electronics and advanced technology.

Moreover, German chemical industries are determined to ensure that by 2050, they will have attained a climate-neutral scenario by investing more in sustainable and green chemical technologies. The nation focuses on the increased market need for environmentally friendly chemical solutions that are advanced by the innovation and regulatory measures to mitigate carbon emissions and promote the use of the circular economy. These eco-friendly innovations form the foundation of sophisticated technology for the development of such materials as silicon carbide (SiC), which makes Germany a pioneer in clean technologies and energy-saving devices with semiconductors.