Semiconductor Foundry Market - Regional Analysis

APAC Market Insights

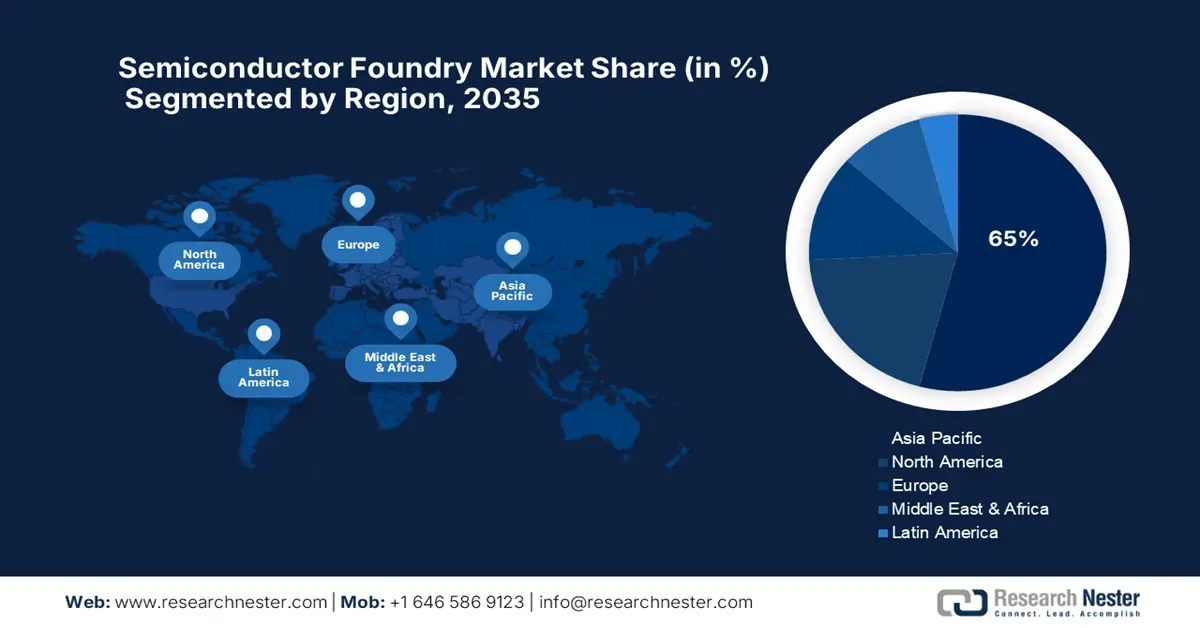

Asia Pacific semiconductor foundry market is anticipated to maintain around 65% market share during the forecast period. The region's leadership is based on the record size and efficiency of foundries in Taiwan and South Korea, which produce the overwhelming majority of the world's most advanced logic chips. These are supplemented by a huge and highly integrated equipment and materials supply chain, and a strong and growing base of Chinese manufacturing.

China is aggressively pursuing technological independence in semiconductors, backed by a long-term national policy and massive state-guided investment. This aims to reduce foreign dependence on technology and develop an entirely indigenous supply chain for both mature and advanced nodes. In a firm demonstration of this, the government established its third and largest national integrated circuit industry investment fund in May 2024. With a registered capital of approximately USD 47.5 billion, its new Big Fund is dedicated to accelerating the country's push towards making its semiconductor dreams a reality.

India is emerging as a significant player in the semiconductor foundry market, driven by the government's ambitious plan to welcome investment and foster an indigenous manufacturing ecosystem. The Make in India program and the India Semiconductor Mission are making things favorable for new ventures. Furthermore, new state-of-the-art semiconductor design hubs, such as the cutting-edge 3-nanometer chip design, were set up in Noida and Bengaluru in May 2025. This is a milestone, as India had already achieved 7nm and 5nm designs. Moreover, this step strategically positions India to be a semiconductor innovation and manufacturing center.

North America Market Insights

North America is set to record a strong CAGR of 13% from 2026 to 2035, driven by a record wave of public and private investment that aims to rebalance the continent's semiconductor production on an equal footing with Asia. The U.S. CHIPS and Science Act has released hundreds of billions of dollars in capital, attracting massive investments from the world's leading foundry powers to build new, state-of-the-art fabs. This strategic push to enhance supply chain resilience and re-shore advanced manufacturing is making the region a top semiconductor manufacturing hotspot.

The U.S. is the epicenter of this manufacturing renaissance, and the CHIPS Act is driving a series of new fab announcements. In a landmark deal, the U.S. Department of Commerce reached a tentative accord in April 2024 to provide Samsung with as much as USD 6.4 billion in direct funding. This government support underpins Samsung's massive investment of over USD 40 billion to construct a new complex of state-of-the-art semiconductor facilities in Taylor, Texas, that will introduce state-of-the-art logic production, R&D, and packaging capability to America.

Canada is strategically positioning itself in the North America value chain of semiconductors by building on its strengths in the areas of compound semiconductors, advanced packaging, and R&D. The government is actively building its domestic industry through targeted investments from programs like the Strategic Innovation Fund. In March 2025, the government made a contribution of $8 million to Teledyne for the modernization of its semiconductor tools in its Bromont, Quebec, plant and to establish Canada's position on the global technology supply chain.

Europe Market Insights

Europe is likely to garner significant growth between 2026 and 2035 as a result of the European Chips Act, a multi-billion-euro initiative to double the continent's share in international semiconductor production. The ambitious plan is attracting top investments from world-foundry titans and fostering the growth of the local ecosystem with particular focus on serving the region's strong automobile and industrial sectors. The goal is to enhance Europe's technological autonomy and reduce its reliance on outside chip supplies, and strengthen the industrial base to become more solid and competitive.

Germany is emerging as the hub of Europe's semiconductor production plans with a series of massive investment projects unveiled by the world's leading chipmakers. For instance, Intel and the German Government signed a renewed letter of intent in June 2023 for Intel's planned wafer fabrication plant in Magdeburg. The renewed agreement will see Intel increase its investment to over €30 billion for the plant, which will be significantly subsidized by the government to accommodate Europe's most advanced semiconductor production complex.

The UK is pursuing a targeted strategy focused on leveraging its current strengths in the design of chips, compound semiconductors, and R&D to secure its position in the global supply chain. In May 2023, the UK Government launched its National Semiconductor Strategy, a ten-year plan that commits up to £1 billion over the period. This strategy will cultivate the domestic chip industry by stepping up investment in R&D, improving access to prototyping, and stimulating the development of the UK's leading chip design ecosystem.