Renal Biomarkers Market Outlook:

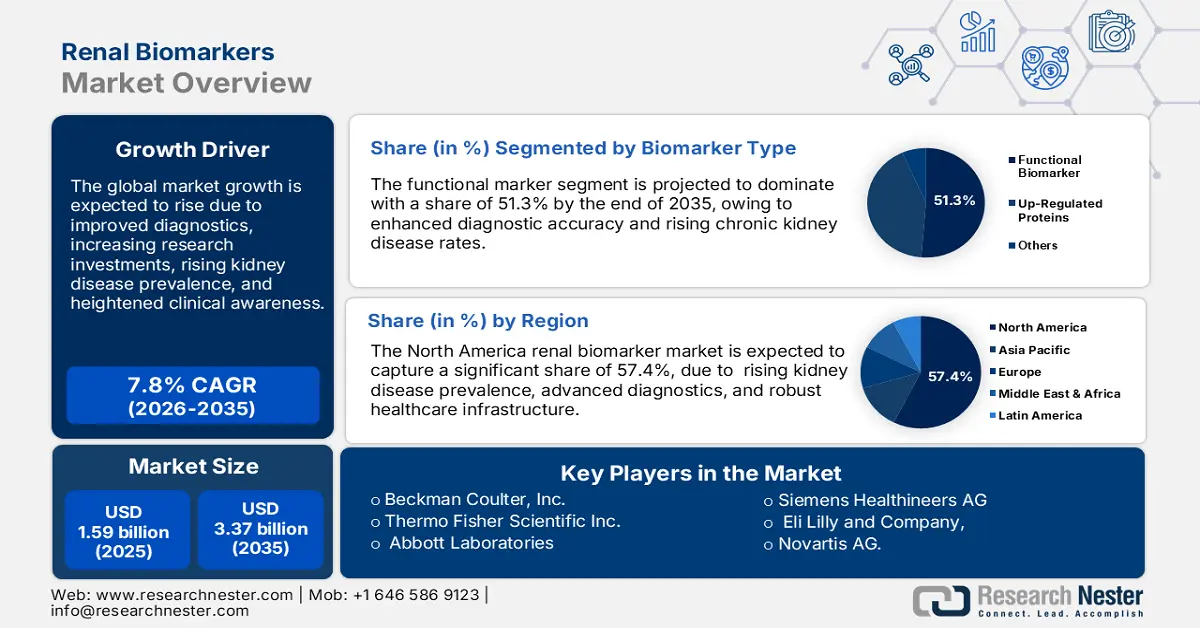

Renal Biomarkers Market size was over USD 1.59 billion in 2025 and is projected to reach USD 3.37 billion by 2035, witnessing around 7.8% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of renal biomarkers is evaluated at USD 1.7 billion.

The rising prevalence of lifestyle-related diseases such as obesity, hypertension, and diabetes significantly increases the risk of developing chronic kidney diseases (CKD). In May 2024, the CDC reported that 39.2% of individuals in the U.S. exhibited chronic kidney disease (stages 1-4), as determined by using the updated 2021 CKD-EPI equation. As these conditions become more widespread, the need for early observation and inspection of nephron function to prevent severe complications is growing. Urinary organ indicators offer a reliable, non-invasive solution for diagnosing and tracking metabolic regulator dysfunction in high-risk individuals, driving their adoption in clinical practice and fueling the progression of the renal biomarkers market.

Additionally, as the global continues to age, the prevalence of kidney-related disorders is rising due to the natural decline in nephrological function and increased susceptibility to conditions such as diabetes and hypertension. Older adults are particularly vulnerable to chronic kidney disease (CKD), making early diagnosis and continuous evaluation essential in preventing disease progression. Regular monitoring, lifestyle modifications, and timely medical interventions can help mitigate complications and improve overall kidney health in aging populations.

Key Renal Biomarkers Market Insights Summary:

Regional Highlights:

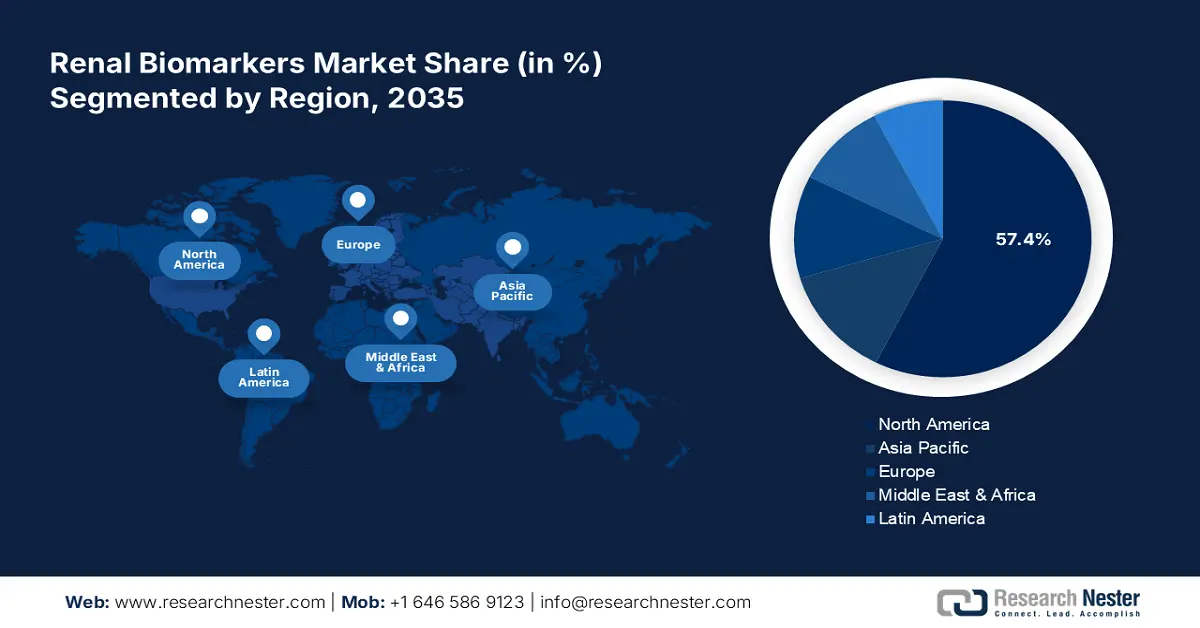

- North America leads the Renal Biomarkers Market with a 57.4% share, driven by the increasing prevalence of CKD and rising healthcare investments, ensuring sustained growth through 2026–2035.

Segment Insights:

- The Functional Biomarker segment is forecasted to hold more than 51.3% share by 2035, propelled by rising chronic kidney diseases and advancements in early diagnostic technologies.

- The Hospitals segment of the Renal Biomarkers Market is anticipated to capture a majority share from 2026 to 2035, driven by the increasing need for early CKD detection and hospital-based diagnostics.

Key Growth Trends:

- Diagnostic progression

- Growing financial commitments in healthcare

Major Challenges:

- Variability in biomarker accuracy and reliability

- Reimbursement and insurance challenges

- Key Players: Randox Laboratories, Sphingo Tec GmbH, Siemens Healthineers AG, Eli Lilly and Company.

Global Renal Biomarkers Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 1.59 billion

- 2026 Market Size: USD 1.7 billion

- Projected Market Size: USD 3.37 billion by 2035

- Growth Forecasts: 7.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (57.4% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, United Kingdom, China

- Emerging Countries: China, India, Japan, South Korea, Singapore

Last updated on : 13 August, 2025

Renal Biomarkers Market Growth Drivers and Challenges:

Growth Drivers

- Diagnostic progression: Advancements in genomics, proteomics, and AI-powered diagnostics are revolutionizing nephrological marker testing by improving sensitivity, accuracy, and non-invasiveness. These technologies enable earlier and more precise diagnosis of nephron dysfunction, allowing for timely interventions and personalized treatment plans. AI-driven analytics enhance data interpretation, making diagnostics faster and more reliable. These innovations are expanding the use of nephron markers in all clinical settings, propagating renal biomarkers market escalation, and improving patient outcomes.

- Growing financial commitments in healthcare: Increasing public and private investments in healthcare infrastructure, particularly in diagnostic technologies, are enhancing access to advanced urological disease indicators. For instance, as per the International Trade Administration in January 2024, medical infrastructure in India is expected to expand at a rate of 15.0% per year. These investments support the research, development, and deployment of innovative bioindicator tests, extending diagnostic capabilities in hospitals, clinics, and laboratories and ensuring broader adoption of renic biotags. As accessibility improves, more patients benefit from early interventions, fueling renal biomarkers market growth.

Challenges

- Variability in biomarker accuracy and reliability: Some urinary markers may produce inconsistent results across different patient populations or varying disease conditions, leading to concerns about their clinical reliability. Factors such as genetic diversity, comorbidities, and environmental influences can affect biotag performance, making standardization challenging. Inconsistent results can lead to misdiagnosis or delayed treatment, reducing confidence among healthcare providers. Addressing these issues through rigorous validation studies and improved disease indicator standardization is essential for increasing trust and promoting widespread adoption in clinical settings.

- Reimbursement and insurance challenges: Limited insurance coverage and inconsistent reimbursement policies for urinary diagnostic tests make them financially burdensome for patients, reducing accessibility to advanced diagnostics. Without adequate sources, healthcare providers may hesitate to recommend these tests, leading to lower adoption rates. This financial barrier slows renal biomarkers market augmentation and restricts innovation in prognostic marker research. Expanding insurance policies, government support, and standardized reimbursement frameworks are crucial to making nephritic biomarker testing more affordable and widely available for early filtration organ disease sensing.

Renal Biomarkers Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

7.8% |

|

Base Year Market Size (2025) |

USD 1.59 billion |

|

Forecast Year Market Size (2035) |

USD 3.37 billion |

|

Regional Scope |

|

Renal Biomarkers Market Segmentation:

Biomarker Type (Functional Biomarker, Up-Regulated Proteins)

By biomarker type, the functional biomarker segment is anticipated to account for more than 51.3% renal biomarkers market share by the end of 2035. The segment’s growth is due to the increasing prevalence of chronic nephric ailments and diagnostic technology advancements that facilitate early detection. These biomarkers provide valuable insights into kidney function, enabling timely intervention and personalized treatment strategies. Their adoption is further supported by heightened awareness among healthcare professionals regarding nephrological health. Consequently, expanding research and improved regulatory support drive rapid growth in this segment with a significant impact on patient outcomes.

End user (Diagnostic Labs, Outpatient Clinics, Research Centers, Hospitals)

Based on end user, the hospitals segment is slated to garner the majority of the renal biomarkers market share over the forecast period. The segment is growing due to the rising prevalence of chronic urinary disease (CKD) and the increasing need for early detection and continuous tracking. According to NLM in March 2022, chronic kidney disease impacted over 800 million people globally, or more than 10% of the global population. Hospitals offer advanced diagnostic facilities, ensuring accurate biomarker-based testing for better disease management. Additionally, growing government initiatives, improved healthcare infrastructure, and higher patient inflow for routine screenings and specialized treatments contribute to this segment’s expansion, making hospitals key adopters of the renal biomarkers market.

Our in-depth analysis of the global market includes the following segments:

|

Biomarker Type |

|

|

Technique |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Renal Biomarkers Market Regional Analysis:

North America Market Statistics

North America in renal biomarkers market is likely to hold more than 57.4% revenue share by 2035. The increasing prevalence of chronic kidney disease (CKD), fueled by factors such diabetes, hypertension, and an aging population, is driving the demand for advanced diagnostic tools. In May 2024, the CDC estimated that over one in seven adults in the U.S., roughly 35.5 million people, or 14%, had chronic kidney disease. This growing need for effective tracing and management of CKD is further supported by rising healthcare investments in North America. These investments bolster research and development in nephrological indicators, leading to enhanced treatment strategies and more accurate diagnostics, ultimately advancing the overall approach to renes disease management in the region.

The shift toward precision medicine in the U.S. which emphasizes tailored treatments based on individual clinical marker profiles, is driving the demand for accurate renic conditions. This growing need is further supported by increased funding for both public and private sectors, which accelerates the development of new molecular markers and advanced technology. As a result, research and innovation in the filtration organ diagnostics indicators category is thriving, propelling a substantial surge in the renal biomarkers market.

The healthcare system in Canada invests in initiatives to improve CKD diagnosis and management, creating opportunities for integrating nephron indicators into routine clinical practice. This coupled with collaborations between pharmaceutical companies, biotech firms, and research institutions, accelerates the development of new urinary organ screening diagnostics and treatment options. These efforts not only enhance the effectiveness of CKD care but also expand market opportunities, driving innovation and adoption of the advanced market in Canada.

Asia Pacific Market Analysis

In APAC, the renal biomarkers market is set to garner substantial revenue share, over the forecast period. The rise of local and multinational biotech firms investing in nephron markers is driving innovation, accelerating product development, and expanding the renal biomarkers market across Asia Pacific. Simultaneously, rapid urbanization, lifestyle changes, and an aging population are increasing the prevalence of uropoietic organ diseases, creating a growing demand for advanced diagnostic and monitoring solutions. These factors collectively contribute to the widespread adoption of tubular bio-indicators, enhancing early observation and personalized treatment options for metabolic regulator disease patients.

The aging population in China, combined with lifestyle changes such as high-sodium diets and sedentary habits, is driving a rise in CKD cases, increasing the demand for early observation and monitoring solutions. In January 2024, Frontiers Media S.A. predicted that there were approximately 119.5 million individuals in China suffering from chronic kidney disease. Simultaneously, the rapid expansion of the biotechnology and pharmaceutical sectors is fueling research and development in urological markers, leading to accelerated product innovation and commercialization. These factors together are strengthening the renal biomarkers market, improving diagnostic capabilities, and enhancing treatment strategies for excretory organ disease management in China.

The expanding healthcare infrastructure in India, backed by increased government spending and private sector investments, is enhancing access to advanced diagnostic technologies, including nephric marker testing. As per IBEF in November 2024, the hospital sector in India, which makes up 80% of the country's healthcare system, is projected to reach USD 132 billion by 2023. Simultaneously, the country’s rapidly growing biopharmaceutical sector is driving significant research and development in such screening techniques, fostering innovation and accelerating the commercialization of new diagnostic solutions. These combined efforts are strengthening the renal biomarkers market in India, improving early tracking and disease management while advancing precision medicine approaches for kidney-related conditions.

Key Renal Biomarkers Market Players:

- Beckman Coulter, Inc

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Thermo Fisher Scientific Inc.

- Abbott Laboratories

- Bioporto Diagnostics A/S

- Astute Medical, Inc.

- Randox Laboratories

- Sphingo Tec GmbH

- Siemens Healthineers AG

- Eli Lilly and Company

- Novartis AG.

Key companies are driving innovation in the renal biomarkers market by developing advanced diagnostic technologies, such as urine and blood-based tests, to detect the early stages of chronic kidney diseases (CKD). These companies are focusing on diagnostic markers such as protein/creatinine ratios and genetic markers, enabling personalized treatment plans and more effective evaluation. For instance, in January 2025, the FDA’s acceptance of a urine biomarker panel for drug-induced kidney injury marked a significant advancement, enhancing safety and early diagnosis in drug development trials for urological health. Additionally, they are exploring the potential of SGLT2 inhibitors and immunotherapies to enhance disease management, improve patient outcomes, and reduce healthcare costs. Such players are:

Recent Developments

- In December 2024, CORE Kidney, Boehringer Ingelheim, and Eli Lilly promoted blood and urine tests at the 2025 Rose Parade, advancing nephritic diagnostics through awareness and early CKD detection for at-risk patients.

- In January 2024, Merck’s Phase 3 KEYNOTE-564 trial showed KEYTRUDA’s potential in preventing nephric cell carcinoma recurrence, advancing nephron biomarkers by enhancing immunotherapy-based diagnostics for early observation and personalized treatment.

- Report ID: 7131

- Published Date: Aug 13, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Renal Biomarkers Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.