Natural Gas Storage Market Outlook:

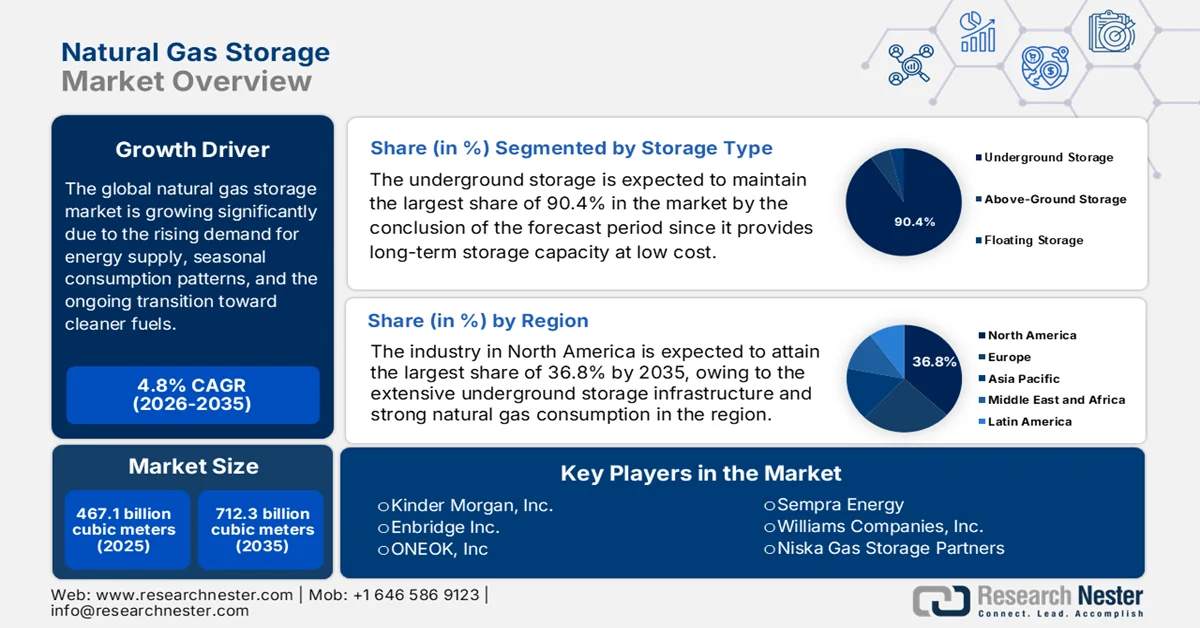

Natural Gas Storage Market size was valued at 467.1 billion cubic meters in 2025 and is projected to reach 712.3 billion cubic meters by the end of 2035, rising at a CAGR of 4.8% during the forecast period from 2026 to 2035. In 2026, the industry size of natural gas storage is assessed at 489.5 billion cubic meters.

The natural gas storage market is poised to witness continued growth owing to the rising demand for energy supply, seasonal consumption patterns, and the ongoing transition toward cleaner fuels. In this context, operators manage injections and withdrawals across key regions to support reliability as well as market stability. The official statistics by the U.S. Energy Information Administration (EIA) stated that from 2020 to 2025, U.S. natural gas exports showed strong growth, reaching a total of 8,973,194 million cubic feet in 2025. Pipeline exports to Canada and Mexico accounted for 3,464,907 million cubic feet, whereas the LNG shipments surged to 5,508,175 million cubic feet, supplying multiple international markets, which also include Europe and Asia Pacific. Meanwhile, in Europe as of October 2025, storage reached 83% full, which is equivalent to 85 billion cubic meters, up from 34% in April, supported by coordinated injections of 50 bcm over the summer.

U.S. Natural Gas Exports and Prices (2020-2025) by Type: Pipeline vs LNG

|

Type |

2020 |

2022 |

2023 |

2025 |

|

Total Exports |

5,284,678 |

6,906,432 |

7,610,034 |

8,973,194 |

|

Pipeline |

2,894,329 |

3,040,787 |

3,266,561 |

3,464,907 |

|

LNG |

2,389,963 |

3,865,643 |

4,343,027 |

5,508,175 |

|

Average. Price (USD/Mcf) |

3.70 |

9.64 |

5.45 |

6.04 |

Source: EIA

2023 U.S. Natural Gas Exports and Imports by Pipeline and LNG - Key Statistics

|

Type |

Destination / Source |

2023 Volume (Bcf/d) |

Change vs 2022 |

|

LNG Exports |

Global |

13.6 (December average) |

+1.3 (+12%) |

|

Pipeline Exports |

Canada |

2.8 |

+0.2 (+7%) |

|

Pipeline Exports |

Mexico |

6.1 |

+0.5 (+8%) |

|

Total Exports |

U.S. |

20.9 |

+10% |

|

Pipeline Imports |

Canada |

8.0 |

-0.3 (-3%) |

|

LNG Imports |

U.S. |

<0.1 |

- |

Source: EIA

Furthermore, the natural gas storage market dynamics are influenced by infrastructure development, strategic reserves management, and evolving regulatory frameworks. Besides, the continuous trade flows are contributing to the market by affecting the supply-demand balance and driving cross-border storage needs. In this context, World Integrated Trade Solution (WITS) states that in 2023, Norway emerged as the leading global supplier of natural gas in gaseous state, which contributed almost one-third of Europe’s total exports, underscoring its dominant role in the natural gas storage market. Belgium, Azerbaijan, and France followed as significant contributors, each supplying around 10% to 15% of global shipments, whereas Canada and the U.S. strengthened North America’s presence in international trade dynamics. Hence, these top exporters together ensured that most of the world’s natural gas demand was met through a mix of long-term contracts and flexible delivery arrangements.

Top 10 Countries by Natural Gas Shipments in Gaseous State Globally in 2023 - Export Volumes and Trade Value

|

Country |

Export Quantity (Kg) |

Trade Value (USD 1,000) |

|

Norway |

91,886,600,000 |

57,212,323.05 |

|

Belgium |

24,831,600,000 |

15,668,087.77 |

|

Azerbaijan |

19,453,300,000 |

13,678,344.14 |

|

France |

18,301,000,000 |

10,978,704.36 |

|

Canada |

16,091,300,000 |

9,653,121.92 |

|

U.S. |

12,838,300,000 |

7,701,647.25 |

|

UK |

5,957,460,000 |

3,610,742.10 |

|

Myanmar |

5,730,870,000 |

3,437,929.67 |

|

Germany |

6,356,250,000 |

3,163,016.03 |

|

European Union |

3,889,780,000 |

3,042,933.12 |

Source: WITS

Key Natural Gas Storage Market Insights Summary:

Regional Highlights:

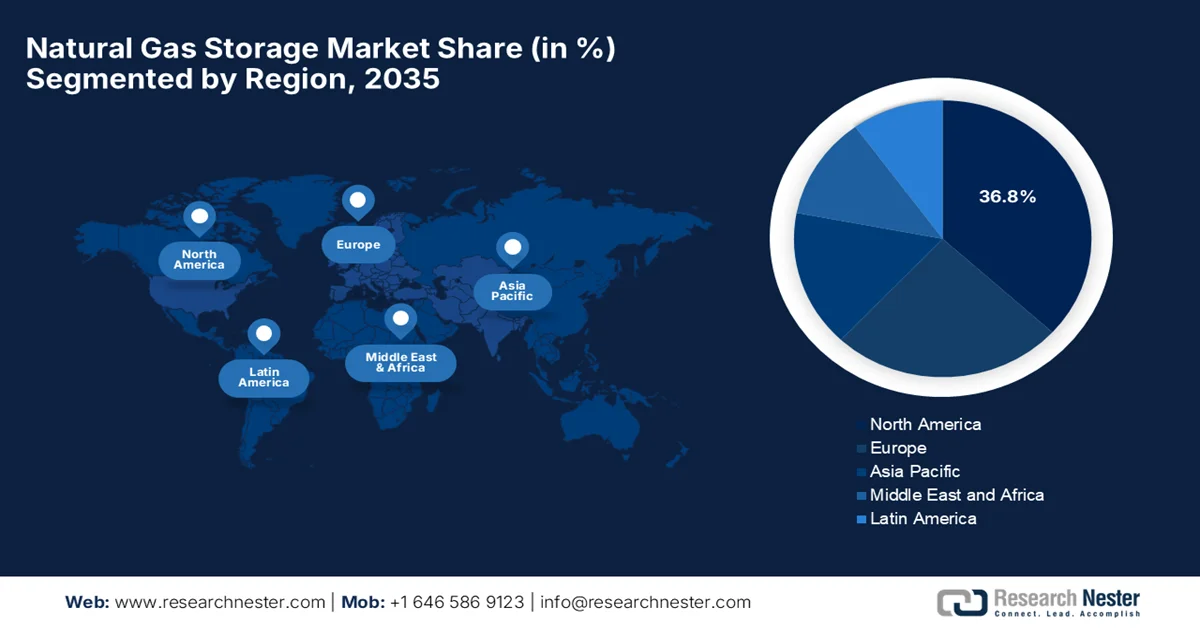

- North America natural gas storage market is projected to dominate with a 36.8% share by 2035, propelled by extensive underground storage infrastructure and strong natural gas consumption for power generation and heating

- Asia Pacific is anticipated to witness notable growth through 2035, spurred by increasing investments in underground storage facilities and a strategic shift toward cleaner energy sources

Segment Insights:

- Underground storage segment in the natural gas storage market is estimated to account for a 90.4% share by 2035, driven by its capability in providing large-scale, long-term storage capacity at relatively low cost

- Seasonal storage segment is expected to secure a significant share by 2035, fueled by the need to manage supply-demand imbalances across different seasons

Key Growth Trends:

- Rising global demand for natural gas

- Need for energy security and strategic reserves

Major Challenges:

- Geopolitical supply disruptions

- Complex regulatory compliance

Key Players: Kinder Morgan, Inc., Enbridge Inc., ONEOK, Inc., Sempra Energy, Williams Companies, Inc., Niska Gas Storage Partners, Centrica plc, Uniper SE, E.ON SE, ENGIE SA, Royal Vopak N.V., RAG Austria AG, NAFTA a.s., Gazprom, Vermilion Energy, Chiyoda Corporation, Samsung Heavy Industries, Worley Limited

Global Natural Gas Storage Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 467.1 billion cubic meters

- 2026 Market Size: USD 489.5 billion cubic meters

- Projected Market Size: USD 712.3 billion by 2035

- Growth Forecasts: 4.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (36.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Russia, Canada, Germany

- Emerging Countries: India, Australia, Japan, South Korea, Brazil

Last updated on : 23 March, 2026

Natural Gas Storage Market - Growth Drivers and Challenges

Growth Drivers

- Rising global demand for natural gas: Natural gas consumption is increasing across power generation, industrial, residential, and commercial sectors. As demand is continuously growing, storage facilities become essential to balance supply and demand fluctuations. According to International Energy Agency reports, in January 2026, the global gas demand growth is forecast to increase by 2% in 2026, and LNG supply rose by almost 7% in 2025. The report highlighted that investment momentum was strong, and more than 90 bcm/year of liquefaction capacity reached a final investment decision, led by the U.S., with more than 80 bcm. In 2026, LNG supply is expected to expand by over 40 bcm, which is more than 7% growth, supporting demand increases led by China and emerging economies in the Asia Pacific, hence benefiting the overall natural gas storage market.

- Need for energy security and strategic reserves: Governments and utilities across different nations are focused on building storage facilities to protect from supply disruptions, geopolitical risks, and any extreme weather conditions. In this context, storage acts as a buffer during emergencies or supply shortages, thereby attracting more pioneers to establish their footprint in the natural gas storage market. In March 2025, the government of Ireland sanctioned the state‑led strategic gas emergency reserve development to save energy security during the transition to renewables. It stated that this reserve will take the form of a floating storage and regassification unit, which is owned by Gas Networks Ireland, ensuring compliance with regional standards. In addition, it is positioned as a temporary, emergency‑only measure and avoids fossil fuel lock‑in while supporting continuity of supply for households and businesses.

- Growth of LNG trade and global gas markets: Expansion of the liquefied natural gas trade increases the need for storage near import-export terminals. Also, the LNG infrastructure requires tank storage, regasification terminals, and buffer storage facilities, benefiting the overall natural gas storage market. In April 2024, the article, which was published by the Institute for Energy Economics and Financial Analysis (IEEFA), stated that the global LNG trade is growing exponentially, which is driven by new liquefaction projects in the U.S., Qatar, Russia, and Canada. It stated that by 2028, total global liquefaction capacity is expected to reach 666.5 MTPA, which is a 40% increase from 2024. The U.S. became the largest LNG exporter in 2023, surpassing Australia, while China retained its position as the world’s largest LNG importer, hence driving significant demand for natural gas storage infrastructure worldwide.

Global LNG Trade Expansion 2023–2028: Country-Wise Imports, Exports, and Capacity Growth

|

Country |

2023 LNG Imports / Exports |

Change (YoY) |

|

U.S. LNG exports |

92.3 MTPA capacity |

Leading global exporter |

|

China LNG imports |

390 bcm |

+4% YoY |

|

Thailand LNG imports |

- |

+34% YoY |

|

Singapore LNG imports |

- |

+30% YoY |

|

Qatar LNG expansion |

32 MTPA North Field East |

1st phase 2025, 2nd phase 2030 |

Source: IEEFA

Challenges

- Geopolitical supply disruptions: The natural gas storage market is mostly sensitive to geopolitical events such as conflicts and issues in trade, which can ultimately disrupt supply and impact storage utilization. For example, any type of regional conflicts or sanctions on LNG-producing countries may reduce available imports, which creates pressure to maintain higher storage levels. On the other hand, the aspect of geopolitical instability affects investment in storage projects near volatile regions, which increases risk perception for operators as well as investors. Also, these supply disruptions can force emergency withdrawals, altering long-term planning and operational strategies. Therefore, nations that are dependent on imported gas face vulnerability, especially during peak demand seasons, highlighting the need for resilient storage and diversified supply networks

- Complex regulatory compliance: The natural gas storage market needs to operate under a complex, multi-layered regulatory frameworks that vary by country, region, and local jurisdiction. In this context, operators are compelled by environmental, safety, and reporting standards, which require multiple approvals for construction and operation. As the regulations continuously keep upgrading to address emissions, safety, and public health concerns, this increases compliance costs and extends project timelines. Besides any delays in permitting can cause disruptions to natural gas storage market expansion, especially for small or mid-sized operators. In addition, the administrative burden of adhering to multiple jurisdictions complicates cross-border or regional storage development.

Natural Gas Storage Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

4.8% |

|

Base Year Market Size (2025) |

467.1 billion cubic meters |

|

Forecast Year Market Size (2035) |

712.3 billion cubic meters |

|

Regional Scope |

|

Natural Gas Storage Market Segmentation:

Storage Type Segment Analysis

The underground storage is expected to maintain the largest share of 90.4% in the natural gas storage market by the conclusion of the forecast period. Its capability in providing large-scale, long-term storage capacity at relatively low cost is the main factor behind this dominance. Countries rely on underground reservoirs to balance seasonal supply and demand, especially during winter heating seasons. In May 2025, the U.S. EIA stated that in 2024, underground natural gas working storage capacity in the lower 48 U.S. states increased, which reflects the growing reliance on storage to balance energy needs. Besides, the demonstrated peak capacity rose by 1.7% (71 Bcf), whereas the working gas design capacity increased slightly by 0.1% (3 Bcf). Therefore, these metrics highlight the continuing importance of underground storage in ensuring a stable natural gas supply in the midst of changing natural gas storage market conditions.

Application Segment Analysis

In the application segment, the seasonal storage is expected to garner a significant share by the end of 2035. The growth of the sub segment mostly driven by the need to manage supply-demand imbalances across different seasons. In addition, there has been a rising residential and commercial heating demand during summer, winter, and fluctuating industrial consumption, which creates a critical role for seasonal storage in maintaining supply reliability. In November 2024, the government of China reported that the Nanpu No. 1 Gas Storage Facility, which is the country’s first offshore gas storage site operated by PetroChina Jidong Oilfield Company, began supplying natural gas to the Beijing-Tianjin-Hebei region for the 2024-2025 heating season. It has a total capacity of 1.814 billion cubic meters, and it is designed to store gas during low-demand periods and release it during peak winter usage, providing 350 million cubic meters to around 3.5 million households, hence benefiting the overall natural gas storage market.

End user Segment Analysis

Utility companies are projected to register themselves with a considerable revenue share in the natural gas storage market. They require stable gas supplies to deliver electricity, heating, and gas distribution services to residential and commercial consumers. In October 2025, the New York State Public Service Commission confirmed that the state’s utilities have adequate natural gas supply, delivery capacity, and storage inventory to meet peak winter demand for residential and commercial customers. It also mentioned that utilities hedged a significant portion of their gas and electricity needs and use storage and financial hedges to mitigate price volatility. In addition, these measures ensure reliable energy delivery, winter preparedness, and protection against market fluctuations while supporting customer affordability programs, hence denoting a positive natural gas storage market outlook.

Our in-depth analysis of the global natural gas storage market includes the following segments:

|

Segment |

Subsegments |

|

Storage Type |

|

|

Application |

|

|

End user |

|

|

Underground Storage |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Natural Gas Storage Market - Regional Analysis

North America Market Insights

North America natural gas storage market is forecasted to garner the largest share of 36.8% by the end of 2035. The region’s growth is largely propelled by extensive underground storage infrastructure and strong natural gas consumption for power generation and heating. The large number of underground storage sites across the U.S. and Canada also propels continued regional market growth. In February 2026, the U.S. Department of Energy approved a 12% export expansion at Cheniere Energy’s Corpus Christi LNG Terminal by adding 0.47 Bcf/d to non-FTA exports from Trains 8 and 9. This brings the terminal’s total export capacity to 4.45 Bcf/d, making it the second-largest LNG export project in the U.S. The expansion highlights U.S. leadership in LNG exports and supports global energy security, while Cheniere Energy continues to drive economic growth and reliable LNG supply, hence denoting a positive natural gas storage market outlook.

U.S. Liquefied Natural Gas (LNG) Facilities and Storage Capacity Trends 2021-2024

|

Year |

Number of Records |

In Service |

Capacity in Service (Thousand Gallons) |

Abandoned |

Capacity Abandoned (Thousand Gallons) |

Retired |

Capacity Retired (Thousand Gallons) |

|

2024 |

185 |

181 |

62,559,109 |

2 |

23,300 |

2 |

1,850 |

|

2023 |

184 |

176 |

60,445,807 |

6 |

23,300 |

2 |

4,009 |

|

2022 |

183 |

175 |

60,151,665 |

8 |

- |

- |

- |

|

2021 |

173 |

169 |

59,524,399 |

4 |

118,857 |

- |

- |

Source: PHMSA

The need to manage price volatility and the expansion of LNG export facilities are responsible for uplifting the natural gas storage market in the U.S. The need to balance supply with highly seasonal demand, fluctuating weather patterns, and the requirement for energy security also propels the country’s market growth. The sector is making a shift toward infrastructure expansion to accommodate these structural changes in demand, ensuring reliability. As of October 2024, data from the EIA in 2023, the U.S. consumed almost 32.5 trillion cubic feet (Tcf) of natural gas, representing 36% of total U.S. primary energy consumption. The largest share went to the electric power sector, which is 40%, followed by industrial at 32%, residential 14%, commercial 10%, and transportation 4% sectors. Besides, Texas, California, Louisiana, Pennsylvania, and Florida were the top consumers, together accounting for 39% of total U.S. natural gas usage, wherein electricity generation and space heating were the primary applications.

The natural gas storage market in Canada is witnessing immense growth, which is propelled by high inventory levels following exceptional production across the Western Canada Sedimentary Basin. The sector is increasingly influenced by the development of major liquefied natural gas export infrastructure on the West Coast, which is expected to alter regional demand and storage utilization patterns. In this context, IEA reported that in 2024, natural gas accounted for 40.2% of Canada’s total energy supply, with domestic production reaching 7,485,652 TJ, covering 150% of the country’s gas needs, whereas 33.2% of production was exported. This fuel is extensively used for electricity generation, heating, and industrial processes, contributing almost 16.4% of electricity generation and 42% of final consumer energy use. In addition, the report also stated that the country is dependent on both domestic production and imports, wherein pipelines and LNG infrastructure support supply and trade.

APAC Market Insights

The Asia Pacific natural gas storage market is growing at a notable pace as countries across the region are focused on energy security and seek to manage the ups and downs of seasonal demand. Nations such as China and Australia are making heavy investments in terms of new underground facilities with a prime focus on building much larger strategic reserves. This growth is being fueled by a massive shift away from coal toward cleaner-burning gas for power generation and industrial use. As stated by IEA, the Asia Pacific supplied almost 32,594,334 TJ of natural gas in 2023, accounting for 11.1% of its total energy mix, with domestic production covering 75.3% of demand at 24,553,764 TJ. China led both production and consumption, which was followed by Australia, Japan, and India, whereas the net imports made up 24.7% of the total gas supply. LNG technology and pipelines support imports, exports, and regional energy security.

The transition away from coal is the primary fueling factor for the natural gas storage market in China. The country is currently leading the world in the construction of new underground facilities, focusing on depleted oil and gas fields and high-turnover salt caverns. In addition, China is heavily investing in large-scale tanks at coastal liquefied natural gas terminals to manage its high volume of imports. The natural gas storage market is shifting from a basic infrastructure phase into a more structured system that balances domestic production, pipeline imports from Russia, and global shipments. As per the government data published in May 2024, China is efficiently expanding its natural gas storage network as part of the carbon peaking and neutrality strategy, with a goal to build six major storage centers and around 50 facilities with a combined working gas volume exceeding 100 bcm. This initiative is led by PipeChina, and it strengthens infrastructure to ensure reliable supply and energy security, hence denoting a positive natural gas storage market outlook.

The strong government backing for setting up large-scale underground storage is boosting the overall natural gas storage market in India. This move is also driven by the country's primary goal to increase the share of natural gas in its energy mix, particularly for the fertilizer, power, and urban distribution sectors. Press Information Bureau (PIB) in January 2026 stated that India has significantly expanded its natural gas infrastructure, with more than 25,400 km of pipelines supporting near-100% city gas distribution coverage nationwide and an additional 10,459 km under construction. Midstream reforms such as the Unified Pipeline Tariff have improved affordability, whereas household and industrial gas access have been strengthened by making sure that there is a reliable supply for cleaner cooking, CNG mobility, and industrial use. These efforts, coupled with governance reforms and integration with renewable energy pathways, solidify the country’s transition toward a gas-based, low-emission economy.

India’s 2023 Liquefied Natural Gas (LNG) Imports by Country: Trade Value & Volume

|

Country/Region |

Trade Value (USD ‘000) |

Quantity (Kg) |

|

World (Total) |

13,261,131.85 |

22,140,900,000 |

|

Qatar |

6,527,147.78 |

10,901,500,000 |

|

UAE |

2,231,903.76 |

3,044,820,000 |

|

U.S. |

1,431,695.47 |

3,176,180,000 |

|

Angola |

450,445.20 |

767,754,000 |

|

Oman |

448,696.52 |

810,383,000 |

|

Nigeria |

415,046.24 |

754,029,000 |

|

Russia - Federation |

296,400.34 |

421,676,000 |

|

Cameroon |

255,615.10 |

411,527,000 |

|

Algeria |

221,861.64 |

347,671,000 |

|

Australia |

214,007.22 |

349,003,000 |

|

Mozambique |

185,122.04 |

279,916,000 |

|

Trinidad and Tobago |

161,472.75 |

267,082,000 |

|

Egypt, Arab Rep. |

149,467.14 |

196,648,000 |

|

Equatorial Guinea |

144,654.90 |

217,897,000 |

|

Guinea |

46,410.64 |

69,107,200 |

|

Belgium |

37,688.42 |

64,213,900 |

|

China |

35,261.11 |

50,000,000 |

|

Singapore |

8,235.58 |

11,489,100 |

Source: WITS

Europe Market Insights

Europe natural gas storage market is anticipated to maintain a strong position in the global industry over the discussed timeframe. The region’s growth is mainly driven by a focus on maintaining high inventory levels to provide a buffer against global supply volatility. Strategic regulations impose mandates on specific filling targets ahead of certain seasons, which has transformed storage from a purely commercial tool into a critical pillar of national security. In September 2025, the European Union announced a regulation (EU) 2025/1733 amending (EU) 2017/1938 to strengthen the role of gas storage in securing supply ahead of the winter season, thereby extending storage-filling obligations until 2027 while also allowing flexibility to respond to market conditions. It aims to reduce dependence on Russia-based gas, ensure predictability and transparency in storage utilization, and balance energy security with market-based pricing, hence suitable for bolstering the overall regional natural gas storage market growth.

Germany natural gas storage market is one of the most influential in the region, which is serving as a critical energy hub for the entire continent. The country has implemented strict federal laws requiring storage facilities to meet specific fill levels ahead of the shortage periods. In this context, Clean Energy Wire in March 2026 reported that Germany is facing renewed pressure to create a national gas reserve as storage levels remain low and geopolitical tensions, particularly the Iran conflict, have pushed energy prices higher. Besides, the gas storage operator association INES recommends a strategic resilience reserve of at least 78 TWh to cover a 90-day interruption of pipeline supplies from Norway, Germany’s main gas supplier. LNG terminals are providing additional security, but the current storage levels are around 20%, which reflects the vulnerability in the system and the cost of USD 2.2 billion to USD 4.4 billion to build the proposed reserve.

Regional regulatory frameworks and mandatory storage targets drive the natural gas storage market in France. The natural gas price volatility and opportunities for cost optimization, which incentivize both public and private actors to manage storage efficiently, are reshaping the growth dynamics of the country’s market. In October 2023, the official statistics by EIA revealed that France had proved natural gas reserves of 590 Bcf as of January 2023, but produces virtually no dry natural gas domestically. The country consumed 1.5 Bcf of dry natural gas in 2021, and it relied entirely on imports to meet its needs. The report highlights that consumption in 2022 was lower due to unusually mild winter temperatures and the impact of Russia’s invasion of Ukraine. In addition, GRTgaz dominates national gas distribution, whereas EDF, a vertically integrated utility, serves as the leading alternative supplier of natural gas in France.

Key Natural Gas Storage Market Players:

- Kinder Morgan, Inc. (U.S.)

- Enbridge Inc. (Canada)

- ONEOK, Inc. (U.S.)

- Sempra Energy (U.S.)

- Williams Companies, Inc. (U.S.)

- Niska Gas Storage Partners (U.S.)

- Centrica plc (UK)

- Uniper SE (Germany)

- E. ON SE (Germany)

- ENGIE SA (France)

- Royal Vopak N.V. (Netherlands)

- RAG Austria AG (Austria)

- NAFTA a.s. (Slovakia)

- Gazprom (Russia)

- Vermilion Energy (Canada)

- Chiyoda Corporation (Japan)

- Samsung Heavy Industries (South Korea)

- Worley Limited (Australia)

- Petronet LNG Limited (India)

- Boardwalk Pipelines (U.S.)

- Vistra Corp. (U.S.)

- Petroliam Nasional Berhad (PETRONAS) (Malaysia)

- McDermott International, Ltd. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Kinder Morgan, Inc. is one of the largest energy infrastructure companies in North America, and it maintains a strong position in natural gas storage and transportation. The company makes heavy investments in expanding storage capacity, optimizing pipeline connectivity, and supporting emerging technologies such as carbon capture and hydrogen infrastructure to strengthen energy security.

- Enbridge Inc. is a prominent energy infrastructure company with major investments in natural gas transportation and storage. The firm is highly focused on expanding underground storage capacity and improving system reliability, along with the incorporation of low-carbon energy solutions into its operations.

- Centrica plc is one of the central natural gas storage operators in Europe through its subsidiary Centrica Storage, which manages underground storage assets used to balance seasonal demand and maintain supply security. Besides, this firm is exploring hydrogen-ready storage infrastructure and renewable energy integration to support the UK’s energy transition.

- Uniper SE is managing multiple underground storage facilities across Germany, Austria, and the UK. In addition, the company benefits from several large storage sites which are connected to major gas trading hubs, supporting both domestic consumption and cross-border supply.

- Gazprom operates one of the world’s largest networks of underground natural gas storage facilities. The firm’s storage infrastructure deliberately supports large-scale gas production and export operations, particularly across Europe and Asia.

Below is the list of some prominent players operating in the global natural gas storage market:

The natural gas storage market is considered to be a consolidated landscape that hosts both global energy infrastructure companies and specialized storage operators across underground storage, LNG terminals, and integrated midstream assets. Major pioneers such as Centrica plc, Enbridge Inc., and Kinder Morgan, Inc. maintain strong positions in this sector, which is due to extensive pipeline networks and large underground storage facilities. Strategic initiatives adopted by the leading players are mergers and acquisitions, long-term capacity contracts with utilities, and investments in hydrogen-ready and low-carbon gas storage technologies. In this context, in May 2025, Vistra announced a total of USD 1.9 billion acquisition of seven modern natural gas generation facilities totaling about 2,600 MW, thereby expanding its footprint across PJM, New England, New York, and California, and hence strengthening its industry‑leading generation portfolio.

Corporate Landscape of the Natural Gas Storage Market:

Recent Developments

- In January 2026, Gulf South Pipeline, a Boardwalk Pipelines subsidiary, announced the launch of an open season for new firm natural gas storage at its Petal Gas Storage facility to support LNG exports and ensure power‑sector reliability. The Petal facility offers high‑deliverability salt‑dome capacity in a critical Gulf Coast corridor.

- In December 2025, Uniper and Vermilion extended their partnership with a two‑year contract for Vermilion’s Germany natural gas production. Vermilion’s output of 2.4 billion kWh in 2025 can power around 220,000 households.

- Report ID: 3487

- Published Date: Mar 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Natural Gas Storage Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.