Hyperconnectivity Market Outlook:

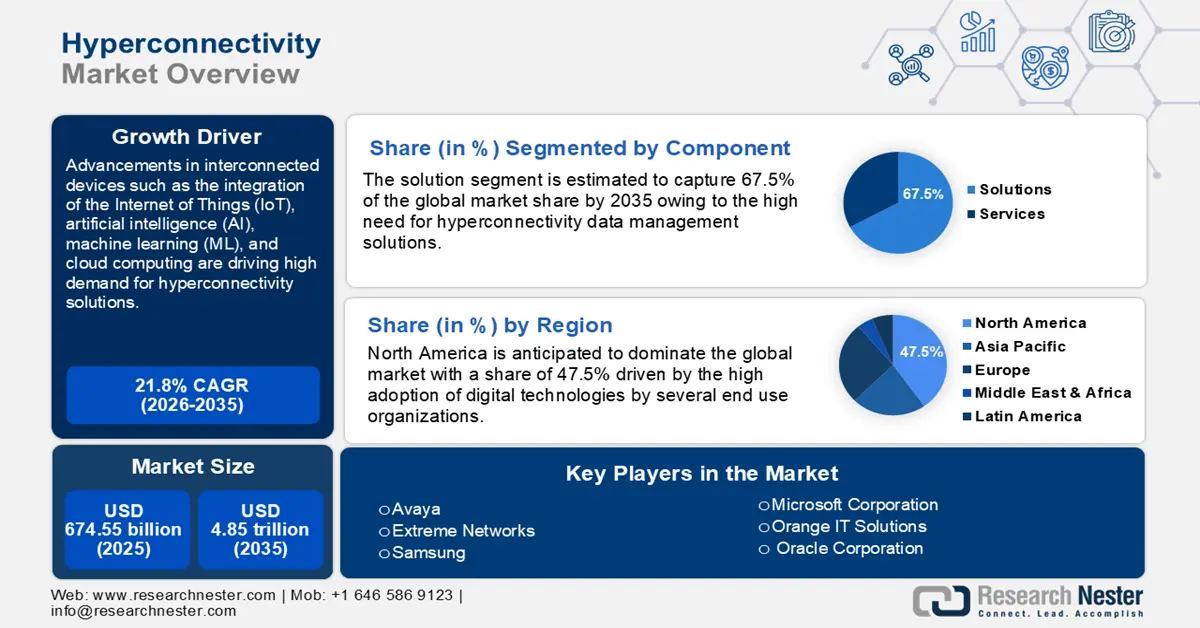

Hyperconnectivity Market size was valued at USD 674.55 billion in 2025 and is set to exceed USD 4.85 trillion by 2035, registering over 21.8% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of hyperconnectivity is estimated at USD 806.9 billion.

Advancements in interconnected devices such as the integration of the Internet of Things (IoT), artificial intelligence (AI), machine learning (ML), and cloud computing are positively influencing market growth. The rise in remote jobs, the growing popularity of live streaming platforms, and innovations in wearable electronics are also augmenting the sales of hyperconnectivity solutions.

Social media platforms are gaining widespread popularity across the globe and are becoming a key channel for communication, interaction, and storage of data. All social media platforms are connected through hyperconnectivity enabling real-time access to any happenings. For instance, according to a report published by the National Center for Biotechnology Information, currently, there are over 3.6 billion social media users and this number is expected to reach 4.4 billion by 2025, globally. After Facebook, YouTube is the second most actively used social media platform across the world with more than 2562 million users.

Key Hyperconnectivity Market Insights Summary:

Regional Highlights:

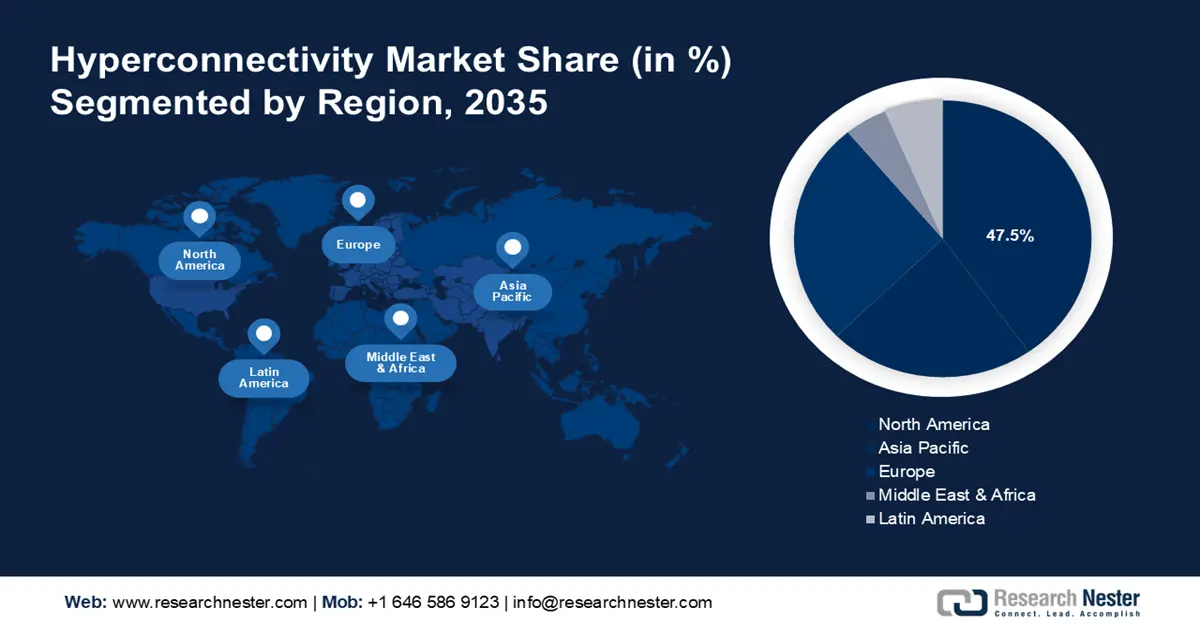

- North America hyperconnectivity market will dominate around 47.50% share by 2035, driven by the rapid adoption of digital technologies by end-use organizations.

- Asia Pacific market will capture a 26.50% share by 2035, driven by growing adoption of IoT to enhance business operations.

Segment Insights:

- The hyperconnectivity solutions segment in the hyperconnectivity market is expected to achieve a 67.50% share by 2035, fueled by the proliferation of IoT devices automating processes across industries.

- The hyperconnected cloud platforms segment in the hyperconnectivity market is anticipated to achieve a 55.50% share by 2035, driven by the rise in remote work and demand for cloud-based collaboration tools.

Key Growth Trends:

- Rise of hyperconnected urban freight networks

- Expanding smart cities and infrastructure development projects

Major Challenges:

- Security and privacy risks

- High costs associated with hyperconnectivity infrastructure development

Key Players: Cisco Systems, Inc., IBM Corporation, Microsoft Corporation, Intel Corporation, Qualcomm Incorporated, Nokia Corporation, Ericsson AB, Huawei Technologies Co., Ltd., AT&T Inc., Verizon Communications Inc.

Global Hyperconnectivity Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 674.55 billion

- 2026 Market Size: USD 806.9 billion

- Projected Market Size: USD 4.85 trillion by 2035

- Growth Forecasts: 21.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (47.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: China, India, Japan, Singapore, South Korea

Last updated on : 18 September, 2025

Hyperconnectivity Market Growth Drivers and Challenges:

Growth Drivers

-

Rise of hyperconnected urban freight networks: Road freight transport remains one of the top GHG pollutant sectors, after aviation and maritime shipping. Reducing the carbon emissions associated with these industry verticals continues to be a major challenge. The EU has had some relative success in decoupling freight and transportation carbon byproducts from economic growth, but it is still responsible for more than a quarter of overall emissions. Hyperconnectivity in urban logistics offers a higher involvement of local actors that can provide more sustainable and denser networks, enabling powerful improvements in the supply chain.

Hyperconnected supply chains directly influence the flow of goods - both from the source company and its customers. For its shareholders including suppliers, OEM, dealers, and customers, it offers massive opportunities for topline growth by faster customer acquisition and retention, while minimizing operational cost and facilitating seamless supply chain operations (transport, warehousing, sourcing, and planning). The TCS Hyperconnected Supply Chain employs telemetry, which facilitates quicker substitute detection and reduced lead time. This procurement solution delivers on the promise of a resilient hyperconnected workbench for detecting legitimate stocks, price fluctuation checks, gathering counterfeit avoidance certificates, and intercepting volatile inventory for pre-empting stocking.

Furthermore, the EU-funded CLUSTERS 2.0 project is a benchmark of government initiatives for developing low-capital goods handling and transhipment solutions, which has laid the groundwork for the EU’s sustainable transportation strategy to shift to 50% railway by 2050. It is a hyperconnected open network of freight clusters and links hubs’ functions via the internet. It falls under the umbrella of The EU’s Trans-European Transport Network (TEN-T) policy that addresses the robust development of a Europe-wide network of railway lines, inland waterways, roads, maritime shipping routes, airports, ports, and railroad terminals for logistics-related activities. - Expanding smart cities and infrastructure development projects: Smart cities and infrastructure development projects are anticipated to offer lucrative opportunities for hyperconnectivity solution producers. Such projects employ advanced technologies to enhance urban living conditions, improve public services, and optimize resource management. Smart roads, bridges, and public transport systems are equipped with advanced sensors and connectivity. Hyperconnectivity enables the seamless integration of data from various sources such as traffic cameras and public databases, aiding in real-time decision-making and management. For instance, Egypt is witnessing the fourth-generation infrastructure development for projects such as international sports, district offices, bus rapid transit (BRT), and art & culture.

- Hyperconnectivity making home smarter: Smart home trends are set to boost the demand for hyperconnectivity solutions in the coming years due to their convenience and energy efficiency. Smart home systems and devices such as home theatres, voice assistants, televisions, room heaters, AC, and more through advanced connectivity technologies. Hyperconnectivity allows the seamless automation of tasks based on user’s preference for example automation of lighting that turns on sensor detection. Hyperconnected solutions also offer real-time access to data and analytics that aid in making informed decisions about building operations.

Challenges

-

Security and privacy risks: The growing number of connected devices and systems is leading to privacy and security concerns. The interconnected nature of devices increases vulnerability risks and one affected device potentially compromises others. Connected devices and networks have a high chance to serve as entry points for several attackers.

-

High costs associated with hyperconnectivity infrastructure development: Deploying and maintaining infrastructure for hyperconnectivity including 5G networks and edge computing facilities is complex and expensive. 5G networks require dense deployment of base stations and cell towers to support high-speed and low-latency communication, which increases the overall investment costs. Also, 5G networks are more power-intensive than previous generations which again leads to high operational costs.

Hyperconnectivity Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

21.8% |

|

Base Year Market Size (2025) |

USD 674.55 billion |

|

Forecast Year Market Size (2035) |

USD 4.85 trillion |

|

Regional Scope |

|

Hyperconnectivity Market Segmentation:

Product Segment Analysis

Hyperconnected cloud platforms segment in the hyperconnectivity market is anticipated to exhibit share of over 55.5% till 2035. Hyperconnected cloud platforms offer scalable and flexible transformation facilities, and the rise in remote work and distributed teamwork culture is augmenting the demand for cloud-based collaboration tools and platforms. Hyperconnected cloud solutions offer seamless communication and collaboration, essential for remote and hybrid work environments. Several organizations are also increasingly adopting digital transformation strategies to improve operational efficiency, customer engagement, and overall competitiveness. For instance, Sunlight is a UK-based start-up that offers cloud-based hyper-converged infrastructure software effective in data storage, management, and networking.

Component Segment Analysis

Hyperconnectivity solutions segment is predicted to dominate hyperconnectivity market share of over 67.5% by 2035. The growing network of IoT devices that connect and exchange data with each other via the Internet is gaining popularity across several industries including healthcare, automotive, BFSI, telecommunications, and manufacturing. The proliferation of IoT devices is transforming industries and driving high demand for advanced hyperconnectivity software solutions. IoT devices often automate processes by triggering actions based on data inputs, hyperconnected software solutions support these automated workflows by optimizing operations and reducing manual interventions.

Our in-depth analysis of the global market includes the following segments:

|

Component |

|

|

Product |

|

|

Organization Size |

|

|

Industry Vertical |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Hyperconnectivity Market Regional Analysis:

North America Market Insights

North America industry is predicted to hold largest revenue share of 47.5% by 2035, owing to the rapid adoption of digital technologies by several end use organizations to enhance their operational efficiency. The healthcare sector in North America is witnessing swift advancements in telemedicine, remote monitoring, and IoT devices. Hyperconnectivity solutions facilitate these innovations by ensuring reliable and secure connectivity between patients, healthcare providers, and medical devices.

The U.S. hyperconnectivity market is anticipated to expand at a high CAGR from 2024 to 2035 due to the increasing adoption of wireless communication networks such as 5G and fiber optic infrastructure. Canada is witnessing the emergence of several new telehealth and IoT medical device companies, which is driving high demand for hyperconnectivity solutions.

APAC Market Insights

By the end of 2035, Asia Pacific hyperconnectivity market is predicted to hold over 26.5% revenue share. End use organizations in the region are widely adopting IoT technologies to enhance their business operations, which is further driving the need for advanced and reliable hyperconnectivity solutions. India, China, Japan, and South Korea are high-growth marketplaces in Asia Pacific.

India is an opportunistic market for hyperconnectivity solution providers due to the rise in remote and hybrid work environments. The COVID-19 pandemic accelerated the shift toward remote and hybrid work models, hyperconnectivity offers scalability, flexibility, and efficient productivity across dispersed teams in an organization.

Hyperconnectivity Market Players:

- Avaya

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Extreme Networks

- Samsung

- International Business Machines Corporation

- Microsoft Corporation

- Orange IT Solutions

- Oracle Corporation

- PathPartner Technology

- Broadcom Inc.

- Fujitsu Limited

- NTT Docomo

- CommScope

- NTT Communications

The hyperconnectivity market is characterized by the presence of established producers and the emergence of new companies. Industry giants are adopting several organic and inorganic marketing strategies such as new product launches, collaborations & partnerships, mergers & acquisitions, and regional expansion to earn high market revenues. Collaboration with other players is expected to lead to the development of innovative hyperconnectivity solutions.

Some of the key players include:

Recent Developments

- In January 2024, Samsung demonstrated its SmartThings hyperconnectivity features for business-centric displays and a new Google EDLA-certified 'WAD' interactive display at Integrated Systems Europe (ISE) 2024, Barcelona.

- In August 2024, Nokia announced that it is selected by TM to build a dedicated international optical Dense Wavelength Division Multiplexing (DWDM) network in Malaysia. This project is set to aid in enhancing growing data traffic management and improving data center connectivity.

- In August 2023, CommScope unveiled the SYSTIMAX Constellation, an edge-based enterprise power and data platform. It allows the development of scalable 10G with fault-managed power networks to incrementally reduce cost, space, labor, and time, thereby, lowering the overall network carbon footprint.

- Report ID: 6420

- Published Date: Sep 18, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Hyperconnectivity Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.