Hydrogenated Starch Hydrolysate Market - Regional Analysis

Asia Pacific Market Insights

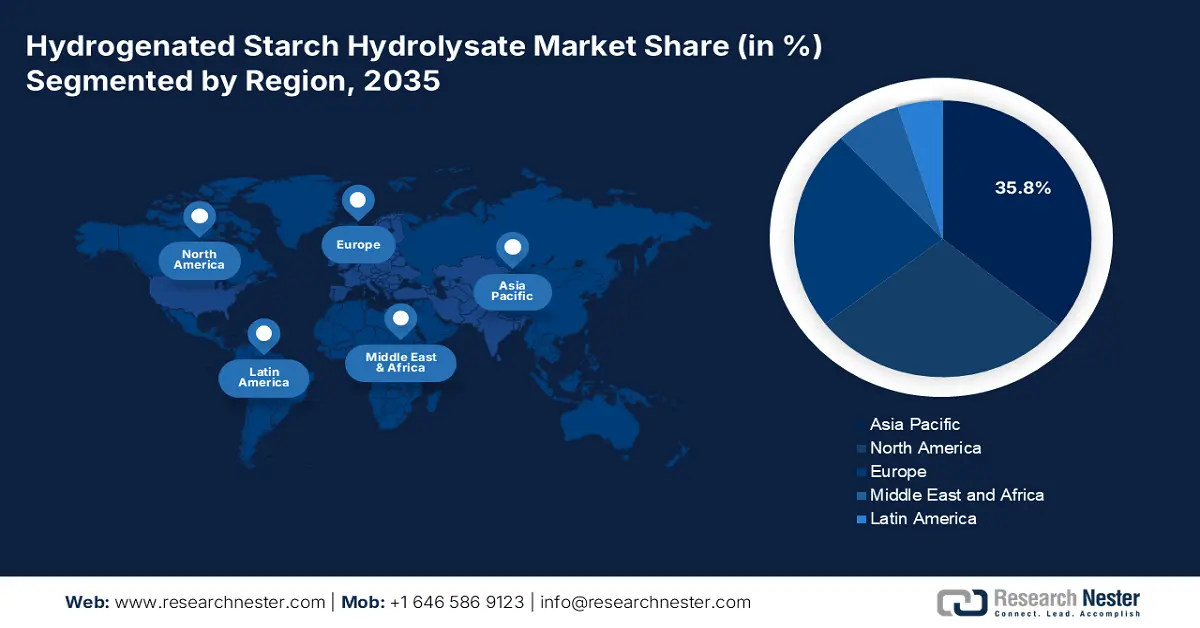

By 2035, the Asia Pacific market is expected to hold 35.8% of the market share, due to the increased demand for low-calorie sweeteners in food and beverage applications. China is expected to see growth from rising diabetic populations and health-focused consumers. Japan and South Korea follow in terms of market share, focusing on sugar-free chocolate and confectionery. India and Indonesia show rapid market growth due to urbanization and processed foods. Australia and Malaysia prefer natural sweeteners as alternatives to sugar, but solid performance for HSH is being seen in the pharmaceutical and other specialty industry segments.

China is the leader in the Asia Pacific HSH market with a 35.1% revenue market share in 2023, with growth driven by applications in food & beverages and pharmaceuticals. The diabetic population continues to drive demand for sugar alternatives. The 2021 International Diabetes Federation (IDF) Diabetes Atlas estimates that 140.9 million people in China between the ages of 20 and 79 have diabetes, making up 25% of the world's diabetic population. Overall, the major manufacturers in China continue to expand production capacity. The HSH market is projected to experience growth during the forecast period, in which government health initiatives and the availability of disposable income are driving growth.

China Sorbitol Trade in 2024

|

Exporting Country |

Value (USD Million) |

Importing Country |

Value (USD Thousand) |

|

South Korea |

$2.37M |

France |

$71.9 |

|

Chinese Taipei |

$1.76M |

South Korea |

$20.2 |

|

Malaysia |

$1.44M |

Brazil |

$5.63 |

|

United Arab Emirates |

$1.37M |

Belgium |

$3.7 |

|

Philippines |

$1.35M |

Japan |

$2.5 |

Source: OEC

India’s high-intensity sweetener (HSH) market is growing due to the rising occurrence of lifestyle diseases and demand for low-calorie and sugar-reduced products around the globe. Likewise, ongoing urbanization and the expanding food and beverage sector are driving new product development related to how sweeteners and functional ingredients are used in these products. According to a 2023 study by the Indian Council of Medical Research-India Diabetes (ICMR INDIAB), 10.1 crore people have diabetes. With 743 District and 6,237 Community NCD Clinics, the Government of India's NP-NCD under NHM enhances local healthcare by emphasizing diabetes prevention, early diagnosis, infrastructure, staff training, and population-based screenings. Consumer awareness of health and wellness trends is creating market shifts in the way HSH products are developed and adopted.

North America Market Insights

North America market is expected to hold 28.7% of the market share by 2035, due to its increased applications in the confectionery, bakery, and oral care segments. HSH, along with other sugar alcohols (i.e., polyols), has contributed immensely to the source sugar alcohols market, as outlined by the U.S. International Trade Commission. The leading producers of these polyols are expanding their production facilities to answer the growing demands of sugar alternatives, as many consumers have expressed a preference for low-calorie sweeteners. Importantly, HSH was eligible under the FDA's GRAS (Generally Recognized As Safe) statement for food.

In the U.S., consumption of hydrogenated starch hydrolysate (HSH) is mainly driven by the confectionery and sugar-free gum sectors. For these reasons, HSH is utilized as a safe alternative sweetener, with a low glycemic response recognized by the FDA. During the 2022/23 marketing year, U.S. corn use for glucose and dextrose was the highest of any category, but it was down 11.4 million bushels. Starch use was down 10.7 million bushels. HFCS was down 5.7 million bushels to 409.31 million bushels due to changes in consumer preferences. Total food, seed, and industrial use was 6.56 billion bushels. Exports were over 1.6 billion bushels, which brought total use to 13.77 billion bushels, at an average price of $6.54 per bushel. Also, recognition of the value of health and concerns surrounding obesity has positively impacted consumption in polyols, and companies have been forced to invest in new formulations and product launches to rely less on sugar.

The rising demand for natural, reduced-sugar ingredients across all segments of the food and beverage category is responsible for the growth in Canada's hydrogenated starch hydrolysate market. Within Canada's advanced and innovative confectionery, dairy, and pharmaceutical sectors, HSH provides bulk sweetness, moisture retention, and textural improvement, which constitutes the primary use of HSH in these industries. Governments supportive of initiatives to change eating habits through reforms to their food supply are strong advocates for reformulations to use of polyol-based sweeteners like HSH. Local producers and importers are emphasizing the company's efforts to satisfy local clean-label or sustainable solutions with publicly visible efforts to change the production and marketing of HSH, targeted towards the needs of Canadian manufacturers.

Europe Market Insights

The European market is expected to hold 23.5% of the market share due to its humectant nature and low glycemic index. Increasing consumer demand for sugar-reduction methods and clean-label ingredients assists with continuous adoption. Food and beverage producers utilize the humectant and stabilizing attributes of HSH to bring improved texture and shelf life. Major manufacturers are focusing on clean-label sweeteners and increasing the uptake of HSH in sugar-free gums and chocolates, especially in health-minded markets like Western Europe.

The hydrogenated starch hydrolysate market in Germany is supported by a developed food-processing sector that is driven by a reduced-sugar ideology. Manufacturers use hydrogenated starch hydrolysate in the formulation of confectionery and baked goods to satisfy brand equity around taste, sweetness, and texture. The trends of consumers with a focused health-conscious mindset (and government encouragement to reduce sugar) lend themselves to a broader purpose of hydrogenated starch hydrolysate. Collaboration and outreach at the local R&D level between ingredient suppliers and food brands will continue to provide opportunities for innovative developments in functional and specialty foods.

The hydrogenated starch hydrolysate market in the UK continues to expand with increased demand for low-sugar confectionery and beverages. Health awareness initiatives and reformulation efforts to reduce sugar content by food manufacturers, as well as versatility-of-product development, have led to new opportunities to include hydrogenated starch hydrolysate in a diverse range of formulation opportunities. Hydrogenated starch hydrolysate's ability to serve as a humectant, stabilizer, and bulking agent supports product developments in the bakery, dairy, and snack industries. The continued interest of food manufacturers and end-users within the gluten-free, clean label, and functional ingredient space, as well as domestic food technology innovation efforts, supports an increasingly dynamic and competitive hydrogenated starch hydrolysate market in the United Kingdom.

Relative Sweetness of Sugar Alcohols and Food Energy, Compared to Sucrose

|

Sweeteners |

Sweetness Relative to Sucrose |

Food Energy (kcal/g) |

|

Sucrose |

1 |

4 |

|

Erythritol |

0.8 |

0.21 |

|

Sorbitol |

0.6 |

2.6 |

|

Xylitol |

1 |

2.4 |

|

Maltitol |

0.9 |

2.1 |

|

Lactitol |

0.4 |

2 |

|

Isomalt |

0.5 |

2 |

|

Mannitol |

0.5 |

1.6 |

Source: USITC