High Speed Steel Market Outlook:

High Speed Steel Market size was valued at USD 3.89 billion in 2025 and is projected to reach USD 6.71 billion by the end of 2035, growing at a CAGR of 5.7% during the forecast period, i.e., 2026-2035. In 2026, the industry size of high speed steel is assessed at USD 4.11 billion.

The primary growth driver for the high speed steel market is the growing demand for high-precision manufacturing in the auto and aviation sectors. Government data show massive public expenditures on advanced manufacturing equipment and infrastructure. For instance, the crude steel production grew from 109.137 million tons (MT) in 2019-20 to 144.299 MT in 2023-24. Crude steel production in 2023-24 registered a growth of 13.4% over 127.197 MT in 2022-23. Domestic crude steel capacity grew from 142.299 MTPA in 2019-20 to 179.515 MTPA in 2023-24. Production of total finished steel in 2023-24 was reported at 139.153 MT, registering a growth of 13.0% over the year. The consumption of total finished steel was 136.291 MT, marking a growth of 13.7% over the previous corresponding year, thus it subsequently follows the growth of demand for HSS. This government spending in the public sector and manufacturing sector upgrading, especially in high-density automobile and aerospace clusters, is propelling the world towards a greater HSS market size.

The U.S. government trade statistics show that the country mainly imported high-speed steel from China in 2023, followed by Brazil, Austria, and Sweden. As a result, leading steel mill operators have made incremental capacity additions. Between 2025 and 2027, a proposed worldwide growth of up to 6.7% (165 million metric tons [mmt]) in steelmaking capacity could degrade the global overcapacity issue if it materializes. Asian economies are expected to account for 58% of the new capacity, with notable increases from China and India. About 16% of the total tonnage expected to come online from 2025 onward involves some level of cross-border investment, with China playing a leading role in these initiatives.

Key High Speed Steel Market Insights Summary:

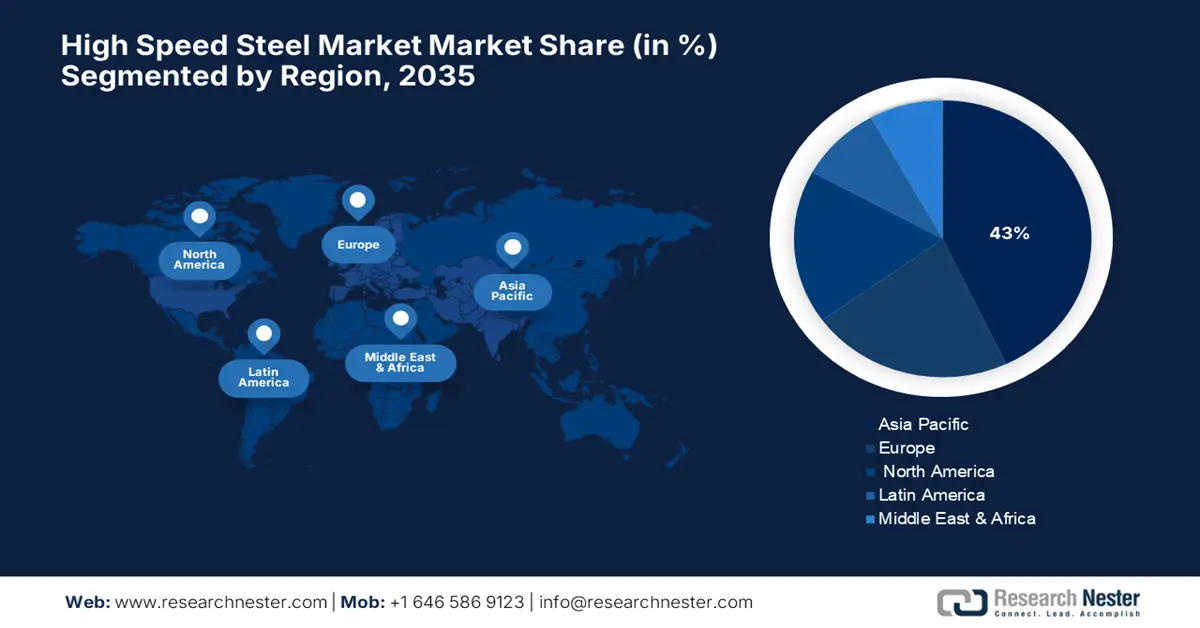

Regional Insights:

- The Asia-Pacific High Speed Steel Market is projected to hold around 43% of total revenue by 2035, propelled by rapid industrialization, expanding automotive and aerospace sectors, and significant investments in green manufacturing technologies.

- Europe is anticipated to secure nearly 22% share by 2035, owing to stringent environmental regulations and rising adoption of sustainable industrial tooling solutions.

Segment Insights:

- The bars & rods segment is anticipated to account for nearly 45% share of the High Speed Steel Market by 2035, spurred by their extensive utilization as raw materials in mass production of precision components and cutting tools.

- The automotive and aerospace segment is projected to capture a 42% revenue share by 2035, supported by expanding production volumes and the need for high-performance tooling materials in precision machining of engine and transmission parts.

Key Growth Trends:

- Rising demand in automotive manufacturing

- Growth of aerospace and defense industry

Major Challenges:

- Raw material price volatility

- Environmental regulations compliance

Key Players:Carpenter Technology Corporation, Sandvik AB, Böhler-Uddeholm (voestalpine), Hitachi Metals, Ltd., JFE Steel Corporation, Sumitomo Electric Industries, AK Steel Holding (now Cleveland-Cliffs), Universal Stainless & Alloy Products, Outokumpu Oyj, BGH Edelstahlwerke GmbH, POSCO, Tata Steel Limited, JSW Steel Limited, Malaysia Steel Works (KL) Bhd.

Global High Speed Steel Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.89 billion

- 2026 Market Size: USD 4.11 billion

- Projected Market Size: USD 6.71 billion by 2035

- Growth Forecasts: 5.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia-Pacific (43% Share by 2035)

- Fastest Growing Region: Asia-Pacific

- Dominating Countries: China, United States, Japan, Germany, India

- Emerging Countries: South Korea, Indonesia, Vietnam, Mexico, Brazil

Last updated on : 9 September, 2025

High Speed Steel Market - Growth Drivers and Challenges

Growth drivers

- Rising demand in automotive manufacturing: With unique hardness, wear resistance, and performance retention at high temperatures, the automotive sector has a large role in the consumption of high-speed steel (HSS). The first HSSs to be widely employed in the automotive sector were high-strength low-alloy steels. High tensile strengths of up to 800 MPa are possessed by these steels. They are designed to have particular mechanical qualities rather than a particular chemical composition. With expanding high speed steel market for electric and hybrid vehicles, OEMs and suppliers increasingly depend on high speed steel market cutting solutions as automotive manufacturers look to gain efficiencies and reduce downtimes. This is forcing automotive OEMs and suppliers to continue making investments in HSS applications.

- Growth of aerospace and defense industry: Precision machining is key to the production of engine components crucial in aircraft, along with landing gear and structural components. In the aerospace and defense sectors, cutting operations often involve high-stress applications, making HSS an increasingly vital material. As global travel surges, economic forces evolve, and defense budgets expand, the demand for precision and durability in machining intensifies. HSS stands out for its resilience under extreme conditions, supporting the industry's growth and technological advancement. Its role is becoming central to meeting the rigorous performance standards required in modern manufacturing. With investments in capital for next-generation components, aircraft manufacturers have entered the realm of advanced tooling solutions.

- Regulatory changes prompting equipment upgrades for enhanced durability: Updated regulatory regimes have increased certification and reporting requirements for hazardous substances. Facilities are now in the process of redesigning and modernizing existing machining and processing lines. In February 2024, the government rolled out several initiatives in the steel industry to encourage self-reliance. Under the Union Budget 2023-24, the government allocated Rs. 70.15 crore (US$8.6 million) to the Ministry of Steel. As a result, these initiatives, coupled with rising demand for corrosion-resistant, durable HSS tooling, are driving the need for solutions that perform reliably in increasingly demanding environments. Manufacturers are seeking tools that not only withstand extreme conditions but also uphold regulatory compliance and operational efficiency. This shift underscores the strategic importance of advanced HSS in high-performance sectors.

1. Emerging Trade in High Speed Steel Market

Bars and rods of high-speed steel (HSS) are semi-finished materials that are commonly used in the making of cutting tools like drills, taps, milling cutters, and saw blades. HSS bars and rods can have excellent hardness, wear resistance, and heat resistance, so they provide the base material for precision machining and high-performance industrial applications.

Top exporters of Bars and Rods of High Speed Steel Market in 2023

|

Exporter |

Trade Value (USD thousands) |

Quantity (Kg) |

|

European Union |

182,126.67 |

9,602,550 |

|

Austria |

131,285.91 |

8,079,080 |

|

France |

116,309.89 |

6,238,090 |

|

Sweden |

85,728.95 |

3,966,860 |

|

China |

82,455.10 |

8,633,670 |

|

Germany |

56,857.12 |

10,018,800 |

|

Japan |

47,917.03 |

3,060,710 |

|

United States |

23,792.48 |

3,303,340 |

|

Brazil |

19,723.58 |

1,407,420 |

|

Spain |

18,627.83 |

5,180,790 |

Source: WITS

Challenges

- Raw material price volatility: Volatility of the prices of base raw materials such as tungsten, molybdenum, and cobalt injects volatility into the production costs. Volatility has the effect of increasing manufacturing costs in a volatile way, making it difficult for manufacturers to provide stable prices. Producers are thus most likely to delay investment or transfer costs to consumers, limiting market growth and inhibiting the adoption of advanced HSS products.

- Environmental regulations compliance: Coercive environmental regulation of the production effluent and waste disposal requires costly production upgrading. Regulatory enforcement by institutions like the EPA and ECHA raises capital and operational expenses. Compliance is unaffordable for most small producers, reducing competitiveness in the sector and, more so, shrinking the supplier base, hence stifling innovation and supply in the HSS industry.

High Speed Steel Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.7% |

|

Base Year Market Size (2025) |

USD 3.89 billion |

|

Forecast Year Market Size (2035) |

USD 6.71 billion |

|

Regional Scope |

|

High Speed Steel Market Segmentation:

Form Segment Analysis

Bars & rods are expected to possess the highest high speed steel market share of almost 45% of the market for high-speed steel by 2035. This is prompted by the enormous growth in the use of bars and rods as the raw material for the mass production of precision components and cutting tools. The U.S. Geological Survey reports that the total steel goods used for industrial machining applications are in high-tech manufacturing industries. The bars & rods can be shaped with ease into complex tool geometries needed in automotive and aerospace tooling. Industry statistics from the U.S. Department of Commerce report that the import of steel bars for tooling applications grew, and the demand for improved quality of input material is increasing.

End use Segment Analysis

Automotive and aerospace are the largest segments projected to capture a 42% revenue share by 2035. This industry's growth is driven by rising production volumes in the automotive and aerospace industries, where high-performance tooling materials are required for safety-critical components and precision machining of engine and transmission parts, and lightweight alloys are essential. High-speed steel tools enable efficient machining at high speed and temperature without downtime and additional cost. Stringent environmental laws for car emissions are compelling producers towards light alloys that require advanced HSS tooling in the processing.

Application Segment Analysis

Cutting tools are the largest segment projected to capture a 35% revenue share by 2035. It is widely applied to manufacture drills, taps, end mills, and reamers. There is a high number of HSS cutting tools that are applicable in automotive, aerospace, and general engineering, which have very stringent requirements for durability and precision. HSS tools have such attributes (i.e., hardness, wear resistance, and strength at high temperature) that are not easily matched in other tools.

Our in-depth analysis of the global high speed steel market includes the following segments:

| Segment | Sub-Segments |

|

Product Type |

|

|

Application |

|

|

End use |

|

|

Form |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

High Speed Steel Market - Regional Analysis

Asia Pacific Market Insights

The APAC high speed steel market is expected to capture nearly 43% of the total revenue in 2035. Industrial development, automotive, aerospace, and process industries growth, along with government emphasis on green industrial processes, are driving the huge share. APAC nations are investing heavily in next-generation manufacturing technology and environmental compliance regulation solutions, fueling spectacular growth in high-performance HSS tooling applications. Expansion in sectors requiring strong corrosion-resistant equipment is fueling demand.

India high speed steel market is experiencing growth in industrialization and green-friendly regulations to enable sustainable manufacturing. The Department of Science & Technology (DST) and relevant ministries have increased year-on-year release of funds on green process technologies in the recent past. The Federation of Indian Chambers of Commerce & Industry (FICCI) puts the number of companies that have switched to green process technologies are driving demand for good Government plans like "Make in India" and state subsidies to drive the switch to better machining solutions in these sectors, making India a rapidly expanding market.

India’s Finished Steel (Alloy + Non-Alloy) Production, Trade, and Consumption

|

Year |

Production (MT) |

Import (MT) |

Export (MT) |

Consumption (MT) |

|

2020-21 |

96.204 |

4.752 |

10.784 |

94.891 |

|

2021-22 |

113.597 |

4.669 |

13.494 |

105.752 |

|

2022-23 |

123.196 |

6.022 |

6.716 |

119.893 |

|

2023-24 |

139.153 |

8.320 |

7.487 |

136.291 |

Source: steel.gov

Europe Market Insights

Europe is expected to share almost 22% of the high speed steel market in 2035, led by robust industrialized economies in Germany, France, and other prominent economies. Europe's Environment Agency (EEA) has also imposed stringent controls on emissions from industrial production, which require sophisticated tooling solutions such as high-speed steel in order to sustain productivity and keep environmental effects at a minimum. Investment in sustainable industrial processes and green technologies has grown more than 13% every year due to European industries employing HSS products that are corrosion- and wear-resistant to meet specifications and enhance productivity.

In Germany, greening policies in industrial sectors were the top concern for the Federal Ministry for the Environment, Nature Conservation, Nuclear Safety and Consumer Protection (BMUV), which in 2023 had over a billion euros set aside to promote cleaner production technology. Other German manufacturing companies are increasingly applying sophisticated HSS tooling in machining operations and assembly lines for both performance requirements and rigorous environmental protection, strengthening Germany's domestic high speed steel market dominance further.

North America Market Insights

Global high-speed steel of around 18% is forecast to be held in North America by 2035. With strong aerospace and manufacturing sectors, demand increased in the U.S. and Canada. The U.S. Environmental Protection Agency states that since 2020, investments in clean industrial technology have increased at the federal and state levels, with the main focus on emission reductions and sustainable manufacturing. According to the U.S. Chemical Safety and Hazard Investigation Board (CSB), there has been an increased transition toward tooling materials such as HSS for higher productivity while adhering to strict safety regulations.

On August 23, 2025, domestic raw steel production in the U.S. was 1,780,000 net tons, with a 78.6% capability utilization rate, which is a 3.1% increase from 1,726,000 net tons and a 77.7% utilization rate in the same week of 2024. Compared to the previous week ending August 16, 2025, raw steel production increased by 0.3%, from 1,774,000 net tons and a 78.3% capability utilization. Year-to-date raw steel production through August 23, 2025, totaled 57.7 million net tons at a 76.6% capability utilization, up 1.3% from 56.9 million net tons for the same period in 2024.

Key High Speed Steel Market Players:

- Carpenter Technology Corporation

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Sandvik AB

- Böhler-Uddeholm (voestalpine)

- Hitachi Metals, Ltd.

- JFE Steel Corporation

- Sumitomo Electric Industries

- AK Steel Holding (now Cleveland-Cliffs)

- Universal Stainless & Alloy Products

- Outokumpu Oyj

- BGH Edelstahlwerke GmbH

- POSCO

- Tata Steel Limited

- JSW Steel Limited

- Malaysia Steel Works (KL) Bhd

The global high speed steel market is dominated by a handful of multinational players primarily headquartered in the USA, Europe, and Japan. Companies like Carpenter Technology and Sandvik maintain leadership through continuous innovation in alloy compositions and production technologies, focusing heavily on R&D to enhance durability and environmental compliance. Japanese manufacturers such as Hitachi Metals and JFE Steel are increasingly investing in automation and precision tooling to support sustainable manufacturing trends. Regional players in India and Malaysia are expanding capacity to meet growing domestic demand while adopting international quality standards. Strategic mergers, joint ventures, and emphasis on eco-friendly product development are key to sustaining competitive advantage.

Top Global Manufacturers in the High Speed Steel (HSS) Market:

Recent Developments

- In July 2025, Metal Bulletin reported that global demand for high speed steel surged by 18% in 2024, driven primarily by the automotive and aerospace sectors. However, rising raw material costs, especially tungsten and cobalt, pressured manufacturers to innovate alloy compositions for cost efficiency and sustainability. Major players like Sandvik and Carpenter Technology are investing heavily in advanced coatings and heat treatment processes to improve tool life and reduce environmental impact.

-

In June 2022, MINING.COM reported that Sandvik secured a significant contract with South32 to supply an underground mining equipment fleet for its greenfield Hermosa critical minerals project in Arizona, USA. The majority of the order consists of battery-electric vehicles (BEVs), marking Sandvik’s largest-ever BEV order. The fleet includes various BEVs and conventional equipment, with deliveries expected to begin in the fourth quarter of 2026 and continue through 2030.

- Report ID: 7929

- Published Date: Sep 09, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

High Speed Steel Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.