Haptoglobin Reagent Market - Regional Analysis

North America Market Insights

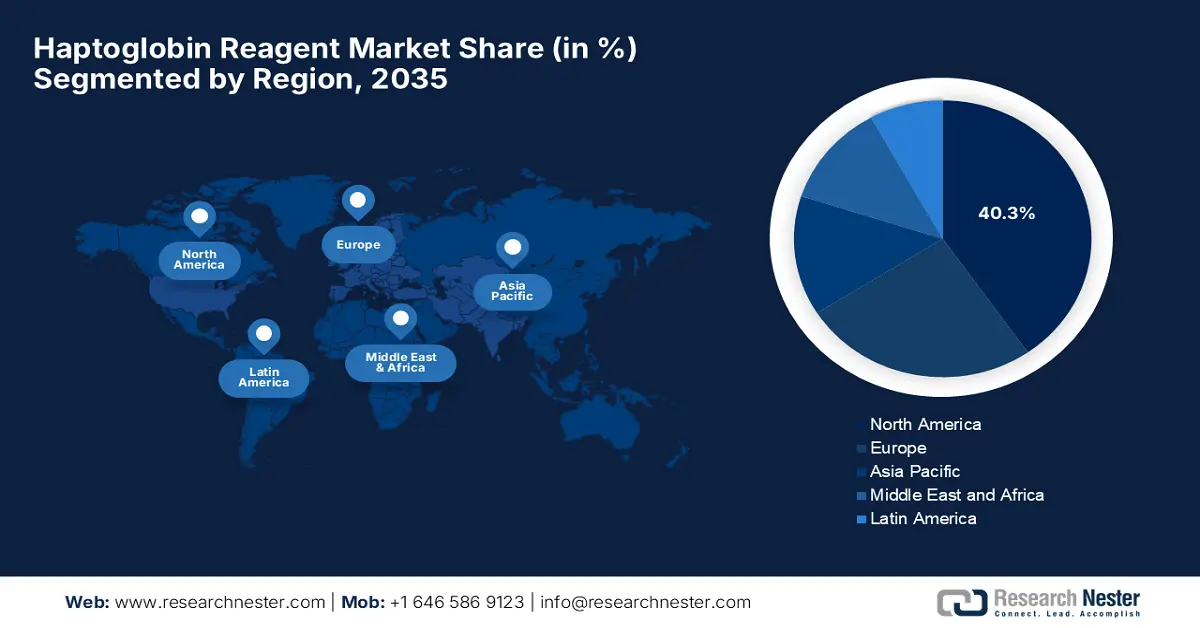

North America leads the industry and is expected to reach a market share of 40.3% by the end of 2035. The region’s market is mainly driven by Canada and the U.S., supported by policy-driven reimbursement reforms, high per capita healthcare spending, and early access to diagnostics. As of the September 2024 CMS article, the total health care spending surpassed a substantial USD 4.9 trillion in the U.S. in 2023, thereby marking a 7.5% increase from the previous year. Also, the healthcare spending currently accounts for 17.6% of the country’s GDP, which denotes the presence of huge investments in health services, diagnostics, and treatment.

The haptoglobin reagent market in the U.S. expands steadily and is aided by robust federal funding and structured insurance frameworks. Demanding market is also supplemented by the elderly population and the occurrence of hemolytic diseases, which keep aggravating the high diagnostic throughput. In April 2024, the article published by NIH stated that securing reimbursement for diagnostic tests in the U.S. requires a strategic approach focusing on coverage, coding, and payment. It also stated that success depends on generating strong clinical evidence and engaging stakeholders to demonstrate the test’s medical necessity and value.

Canada is also maintaining a strong position in the regional market owing to the advancements in healthcare infrastructure and a growing focus on early disease detection and monitoring. Novartis in February 2025 reported that it received Health Canada approval for Fabhalta, which is the first oral treatment for adults with paroxysmal nocturnal hemoglobinuria. The firm further highlighted that this therapy offers enhanced control of red blood cell destruction, thereby addressing unmet needs left by existing treatments, marking a pivotal advancement in managing hemolytic blood disorders in the country.

APAC Market Insights

The Asia Pacific is the fastest-growing region in the haptoglobin reagent market, which is driven by the rising incidence of hemolytic disorders, growing diagnostic infrastructure, and increased government healthcare investments. Countries including China, India, and Japan are the key players in the APAC region, aided by strong policy-driven spending, whereas Malaysia and South Korea are the fastest-growing countries, contributing due to the rising health diagnostics and hospital automation. The region is expanding significantly owing to the advancements in terms of healthcare digitization, integrated diagnostic networks, and bulk reagent tenders.

China dominates the regional market, owing to a rise in government expenditure and centralized procurement by hospitals, and increased national diagnostic coverage under the public healthcare plans in the country. In December 2023, Fujirebio Holdings reported that it signed an agreement with Sysmex Corporation for the mutual supply of reagent raw materials, including antigens and antibodies used in immunoassays, thereby enhancing supply chain resilience and efficiency by leveraging shared raw material assets.

India has a stronger potential in the haptoglobin reagent market deliberately backed by heightened demand for diagnostic testing both in hospitals and laboratories across the country. In December 2025, the country’s government reported that it had taken a few steps to strengthen the country’s diagnostic and epidemic preparedness infrastructure by establishing 163 Viral Research & Diagnostic Laboratories under a Central Sector Scheme, wherein INR 324 crore (USD 38.9 million) was allocated for the same. Of these, 11 labs have been designated regional centers with advanced BSL-3 facilities for detecting high-risk pathogens.

Europe Market Insights

The market is expanding significantly in Europe, driven by the rise in diagnostic precision demand, the aging population, and government investment in personalized medicine. Further, countries like France, Germany, and the UK are leading the regional market due to the early adoption of the immunoturbidimetric and biosensor-based diagnostic platforms. For instance, in March 2023, Hemcheck notified that it received evaluation and distributor orders for its blood and hemolysis-related diagnostic products across several countries in the region, which include France, the UK, Finland, and Iceland, hence denoting a positive market outlook.

Germany accounts for the highest market share in Europe, indicating a well-established diagnostic infrastructure and elevated laboratory test penetration. The country also benefits from a strong focus on early disease detection and monitoring, especially for conditions such as hemolysis and inflammation. Moreover, the country hosts the presence of leading diagnostic companies and ongoing biomedical research, which are providing an encouraging opportunity for continued innovation and integration of reagents like haptoglobin in routine clinical practice.

The U.K. also garnered a huge opportunity in the haptoglobin reagent market, efficiently backed by a well-structured public healthcare system and growing adoption of biomarker-based diagnostics. The country’s government in February 2025 reported that it is committed to improving care for the 3.5 million people living with rare conditions by enhancing early diagnosis, increasing healthcare professional awareness, and ensuring better-coordinated, accessible specialist care, hence making it suitable for standard market growth in the upcoming years.