Gasoline Direct Injection Market Regional Analysis:

APAC Market Insights

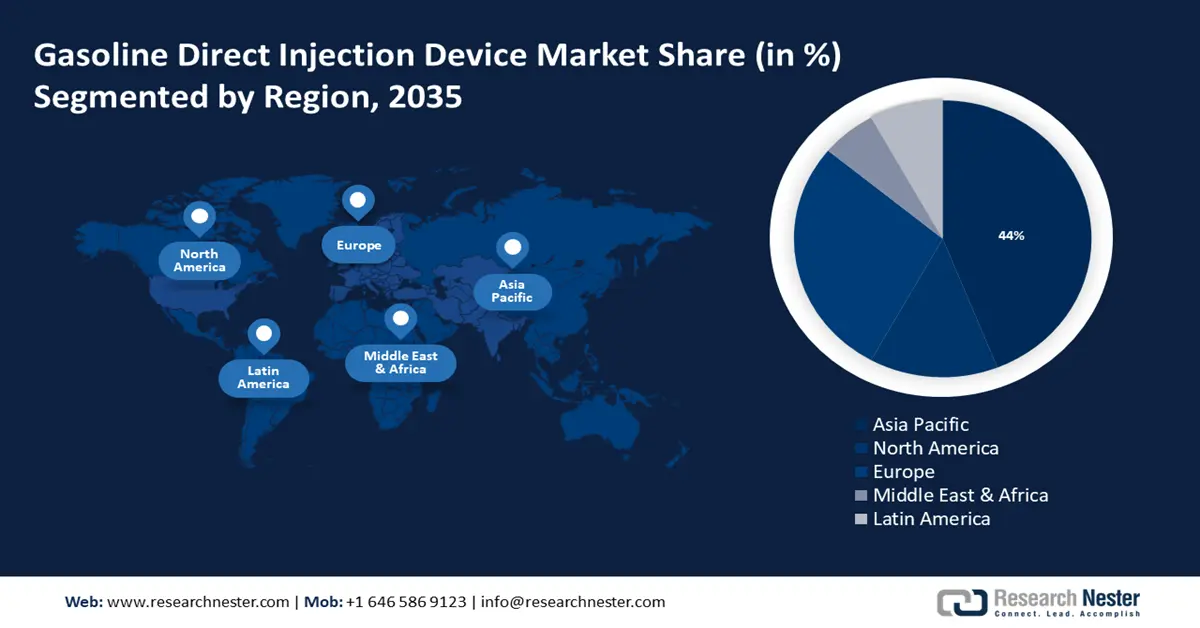

Asia Pacific industry is expected to dominate majority revenue share of 44% by 2035. The small passenger cars sector in Asia Pacific is experiencing growth, largely due to increased vehicle production in China, India, and Japan. According to Research Nester analysis and input from primary respondents, Asia Pacific is expected to be the largest market for small passenger cars.

This growth is driven by strong demand in the automotive industry, and the vehicle type segment is expected to have a positive influence on the market. Furthermore, the market is being driven by the increasing demand for fuel–efficient vehicles to meet strict emission regulations. As observed, the CO2 emissions from fuel combustion in the Asia Pacific totaled to around 17178.5 Mt Co2.

Throughout the forecast period, China is anticipated to dominate the Asia Pacific gasoline direct injection market. China is the largest automobile manufacturer in the world. Approximately 80 million cars will be manufactured globally in 2021. During that year, China's production made up around 32.5 percent of the total global car production. As a result, the market for gasoline direct injection in China is predicted to expand quickly. The cost of maintaining diesel automobiles would rise due to the impending emission rules.

Furthermore, South Korea has stringent emission standards to reduce pollution, driving the adoption of fuel–efficient technologies like GDI. South Korea has stringent emission standards to reduce pollution, driving the adoption of fuel–efficient technologies like GDI. In 2015, the Korean government set an average emission standard of 140g/km, which will be strengthened to 97g/km by 2020. The government’s policies incentivize automakers to integrate GDI systems to their vehicles to comply with these regulations. The government’s policies incentivize automakers to integrate GDI systems to their vehicles to comply with these regulations.

European Market Insights

The European region will also encounter huge growth for the gasoline direct injection market during the forecast period. The strict regulations for fuel efficiency and emission targets are projected to drive the highest growth in the Europe region in the coming years. To meet compliance standards, OEMs are increasingly embracing GDI systems. The presence of major automotive companies such as BMW AG, Daimler AG, and Audi AG in the region is expected to have a positive influence on the growth of GDI systems during the analysis period.

Germany is expected to dominate the gasoline direct injection system industry in Europe by growing at a CAGR of 9.6% during the forecast period. As a leading center for automotive production in the European Union, Germany is a major contributor to the gasoline direct injection market. Efforts towards reducing carbon emissions, while improving fuel economy are key factors that are supporting the adoption of gasoline direct injection systems in the country.

Additionally, France’s strong automotive industry is investing heavily in advanced technologies, including GDI systems, to enhance vehicle performance and efficiency. Leading automotive companies and suppliers are focusing on integrating GDI technology into new vehicle models.

Furthermore, the United Kingdom’s commitment to reducing carbon emissions has led to stricter regulations, The UK plans to cut emissions by 68% by 2030, encouraging the adoption of GDI systems for their efficiency in lowering emissions compared to traditional fuel injection systems.