Air compressor Market Outlook:

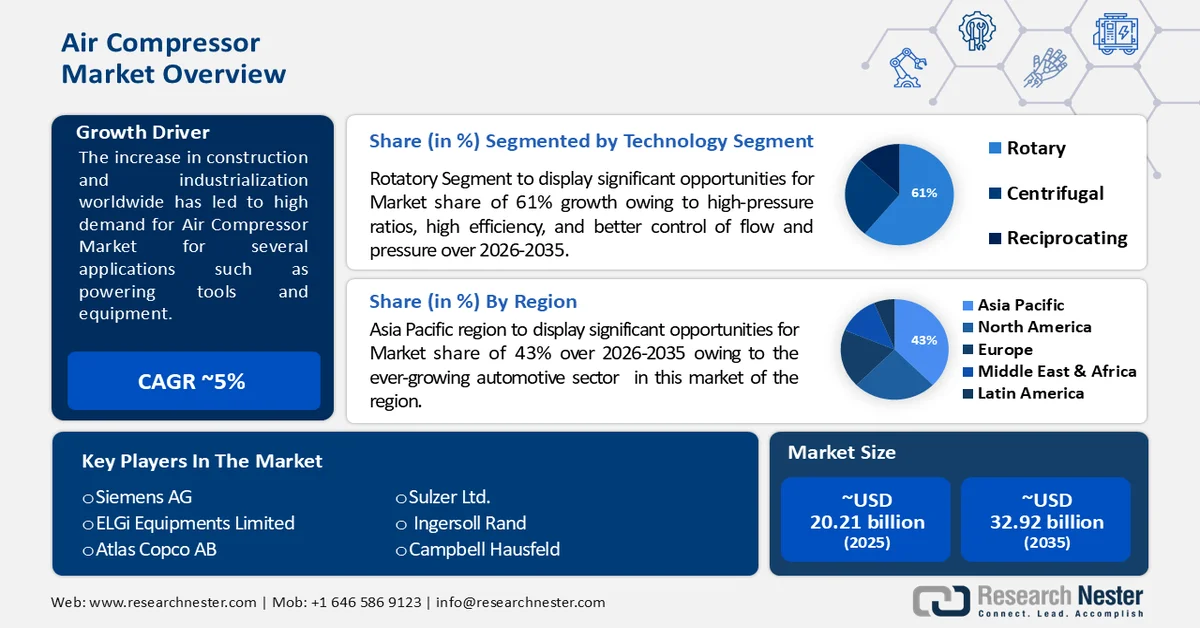

Air compressor Market size was over USD 20.21 billion in 2025 and is anticipated to cross USD 32.92 billion by 2035, witnessing more than 5% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of air compressor is estimated at USD 21.12 billion.

The market growth is impelled by increase in the construction and industrialization worldwide, as several industries are expected to expand along with may construction projects, and this can lead to high demand for air compressors as for several applications such as powering tools and equipment. As the construction sector holds the largest in the world economy, with about USD 10 trillion spent on construction-related goods and services every year, the growth averaged 1 percent a year over the past two decades as compared with 2.8 percent for the total world economy and 3.6 percent for manufacturing.

Furthermore, oil, mining, and gas industries have frequently demanded the air compressors for heavy tasks such as flushing mediums, aerating mud during underbalanced drilling, and air-pigging pipelines, which generally require high-pressure air to power such instruments and equipment in industries such as automotive, construction, and manufacturing.

Key Air compressor Market Insights Summary:

Regional Highlights:

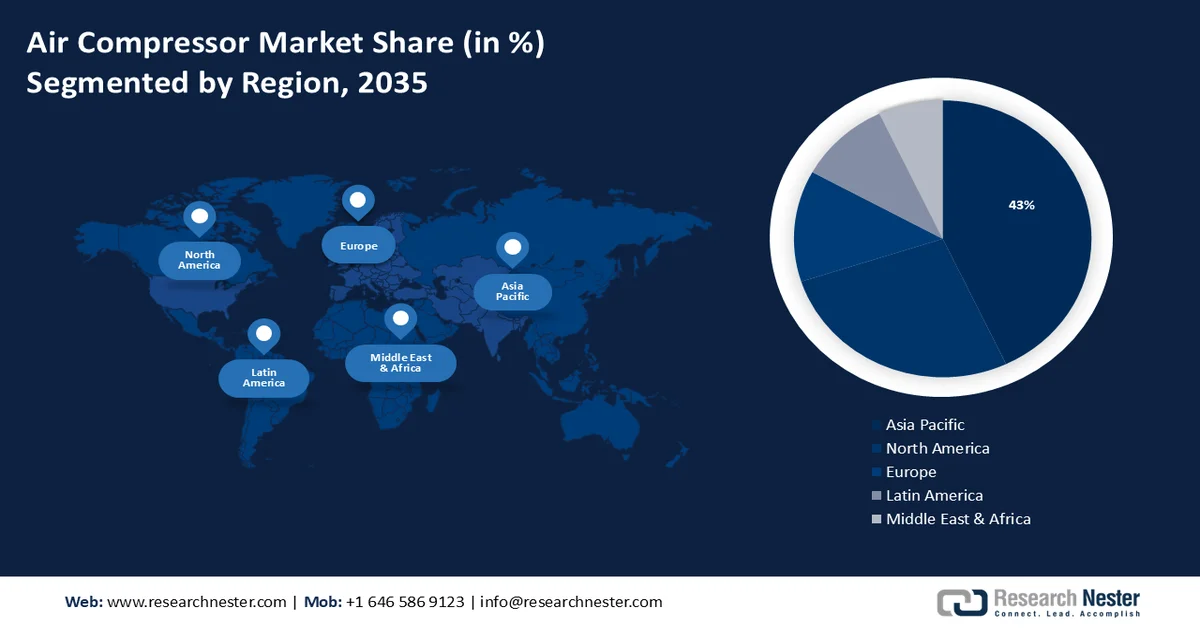

- Asia Pacific in the air compressor market is anticipated to surpass a 43% share by 2035, impelled by rising demand from refineries and steel manufacturing plants alongside expanding LNG and infrastructure investments.

- North America is projected to witness lucrative CAGR through 2035, stimulated by increasing adoption of energy-efficient solutions across manufacturing, energy, and automotive industries.

Segment Insights:

- The rotatory technology segment of the air compressor market is projected to capture a 61% revenue share by 2035, propelled by high-pressure ratios, superior efficiency, and enhanced control of flow and pressure.

- The oil-free segment is anticipated to secure a notable share by 2035, driven by improved energy efficiency and reduced maintenance requirements resulting from the absence of oil and use of dry powder lubrication.

Key Growth Trends:

- Increasing industrial automation and advanced production methods

- Increasing adoption of industrial and commercial sectors

Major Challenges:

- Increased maintenance costs and downtime

- Increased electricity costs

Key Players: Axis Communications AB, Honeywell Security Group, Bosch Security Systems Inc., Hangzhou Hikvision Digital Technology C0., Ltd., Mobotix AG, Zhejiang Dahua Technology Co., Ltd, Geovision Inc., FLIR Systems Inc., Avigilon, Nowon Technologies Pvt Ltd..

Global Air compressor Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 20.21 billion

- 2026 Market Size: USD 21.12 billion

- Projected Market Size: USD 32.92 billion by 2035

- Growth Forecasts: 5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (43% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: Brazil, South Korea, Mexico, Indonesia, Vietnam

Last updated on : 25 February, 2026

Air compressor Market - Growth Drivers and Challenges

Growth Drivers

-

Increasing industrial automation and advanced production methods- Automation and advanced production methods require compressed air for various operations, including power tools, vacuum pumps, air conditioning, and ventilation. This will drive the growth of the air compressor market as they are a crucial component in these processes. Automation is said to rise global productivity by 0.8% to 1.4% annually.

- Increasing adoption of industrial and commercial sectors- like manufacturing, construction, mining, oil and gas, and more: As the global industrial and commercial sectors expand, the demand for air compressors for various applications will grow.

- Growing focus on sustainable energy solutions- As the global focus on reducing greenhouse gas emissions and promoting sustainable energy solutions increases, air compressors have also gained momentum as a renewable source of energy, as they can produce compressed air using power generated through renewable sources like wind, solar, etc.

- Increasing demand from developing regions- The air compressor market is expected to see significant growth in emerging economies, where the industrial and construction sectors are witnessing rapid development. The increasing industrial and commercial activity in these regions is expected to drive the demand for air compressors.

- Growing technological advancements- The air compressor market is also expected to undergo rapid technological advancements, as advancements in automation, robotics, and other fields will translate to the development of advanced air compressors with improved efficiency and performance.

- Rising environmental concerns- The growing awareness about the negative environmental impact of air pollution, greenhouse gas emissions, and other pollutants, will drive the demand for air compressors that are energy efficient and have low emissions.

- Increasing adoption of green building practices- The growing popularity of green building practices, along with the rising focus on sustainability, will also drive the market for air compressors as they can produce compressed air using renewable sources of energy.

challanges

-

Increased maintenance costs and downtime- Poor maintenance practices and low maintenance can lead to increased air compressor replacement costs and more downtime for the equipment.

-

Increased electricity costs- Poor compression efficiency and poor maintenance can lead to increased electricity costs associated with air compressor operation.

-

Environmental regulations- Air compressor emissions are subject to increasing regulations around the world, as air compression can often lead to air pollutants. Proper maintenance can help reduce emissions and comply with governmental regulations.

Air compressor Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5% |

|

Base Year Market Size (2025) |

USD 20.21 billion |

|

Forecast Year Market Size (2035) |

USD 32.92 billion |

|

Regional Scope |

|

Air compressor Market Segmentation:

Technology Segment Analysis

The rotatory technology is estimated to account for revenue share of 61% by 2035, owing to high-pressure ratios, high efficiency, and better control of flow and pressure. Moreover, rotary compressors used in the process industry use electric motor drivers. Compressors used in portable service use internal combustion engines. The use of rotary positive displacement compressors provides various advantages such as longer running time, lower maintenance and service costs, and lower energy consumption. This will allow for greater efficiency in the use of the available energy resources, leading to lower greenhouse gas emissions, as well as lower costs and improved competitiveness. Moreover, this allows for the production and availability of compressors with a wide range of configurations, sizes, and specifications, offering a greater choice for consumers. This can enable the selection of compressors as per the specific application and requirements, leading to more effective and efficient use of the system.

Lubrication Segment Analysis

The oil-free segment is set to garner notable share by 2035, as absence of oil and the use of dry powder lubrication can improve overall efficiency, reducing energy consumption and running costs. The use of dry powder lubricant does not require regular servicing and maintenance, reducing the downtime and costs associated with maintenance. Moreover, the oil-free design is a more eco-friendly and sustainable approach, as it reduces the use of oils or lubricants and decreases the risk of oil leakage or spills that can impact the environment.

Our in-depth analysis of the global market includes the following segments:

|

Technology |

|

|

Lubrication |

|

|

End-users |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Air compressor Market - Regional Analysis

APAC Market Insights

The air compressor market share in Asia Pacific is estimated to cross 43% by 2035, impelled by increasing demand for compressors from refineries and steel manufacturing plants. Countries like China are undergoing rapid industrialization, leading to a surge in energy demand and industrial activities, thereby boosting the demand for compressors in the manufacturing sector. Moreover, the region's growing investments in LNG, chemical, mining projects, and infrastructure development are fueling the demand for air compressors in various industries such as automotive, construction, electronics, and more. China is one of the world's most important nations in 2021, which contributed to the rise in LNG consumption. Natural gas LNG imports were approximately 94 billion cubic meters in 2020 and 109.5 billion cubic meters in 2021. This surge in demand caused China to overtake Japan as the world's largest importer of LNG. Demand has increased as a result of Chinese LNG buyers signing long-term contracts for more than 20 million tons per year.

North American Market Insights

The North American air compressor market is poised to observe lucrative CAGR during the forecast timeframe, led by demand for energy-efficient solutions in various industries like manufacturing, energy, and automotive. Furthermore, environmental regulations and a growing focus on sustainability are pushing industries to adopt energy-efficient air compressors to comply with regulations and reduce emissions. Additionally, the expansion of end-use industries like automotive production and food processing is creating a higher demand for air compressors in North America.

Air compressor Market Players:

- Siemens AG

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- ELGi Equipments Limited

- Atlas Copco AB

- Sulzer Ltd.

- Ingersoll Rand

- Campbell Hausfeld

- Doosan Infracore Portable Power

Recent Developments

- with the introduction of more powerful LS190-260 Series units, Sullair, a pioneer in the compressed air solutions business since 1965, announced the expansion of its well-liked and incredibly effective LS Series lubricated rotary screw industrial air compressors.

- Kaeser Kompressoren SE in Germany and Kaeser Compressors, Inc. in the US are celebrating one year of only using green energy in their operations. Not only are all Kaeser compressors made entirely of renewable energy, but Kaeser also matches its energy usage in Germany and the US with renewable energy.

- Report ID: 1192

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Air compressor Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.