Agricultural Films Market Outlook:

Agricultural Films Market size was valued at USD 14.1 billion in 2025 and is projected to reach USD 31.1 billion by 2035, growing at a CAGR of 9.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of agricultural films is assessed at USD 15.4 billion.

The market is poised for steady growth owing to the need to enhance crop productivity and support sustainable farming practices. Films such as mulch, greenhouse covers, and silage wraps help regulate temperature and extend growing seasons, making them highly essential for modern and protected cultivation. In this context, based on the government data from the U.S. Department of Agriculture, the University of Wisconsin, funded by the USDA’s National Institute of Food and Agriculture through an AFRI allocation of USD 1,000,000, is conducting a project from 2023 to 2026 to develop 100% biobased and fully soil-biodegradable mulch films from renewable woody biomass such as poplar wood and forest residues. It also stated that the project is mainly focused on optimizing film fabrication, characterizing their mechanical and mulching performance, and evaluating their environmental and economic feasibility through techno-economic analysis and life cycle assessment.

Furthermore, the international agricultural films market is embracing biodegradable, compostable, and eco-friendly materials, allowing the firms to comply with evolving environmental regulations. In this context, the European Bioplastics in October 2024 officially reported that the European Union included soil-biodegradable mulch films, coating agents, and water retention polymers in the Fertilising Products Regulation (FPR 1009/2019). So, these products must meet strict biodegradability criteria as outlined in the Delegated Acts to make sure they meet environmental safety standards and promote healthier soils. Moreover, the soil-biodegradable mulch films, proven for more than 20 years to match the agronomical efficiency of conventional plastics, eliminate the need for post-harvest retrieval, recycling, or disposal. Their inclusion in the FPR supports sustainable agriculture, encourages innovation, and addresses the issue of microplastic accumulation in soils, hence positively impacting market growth.

Key Agricultural Films Market Insights Summary:

Regional Highlights:

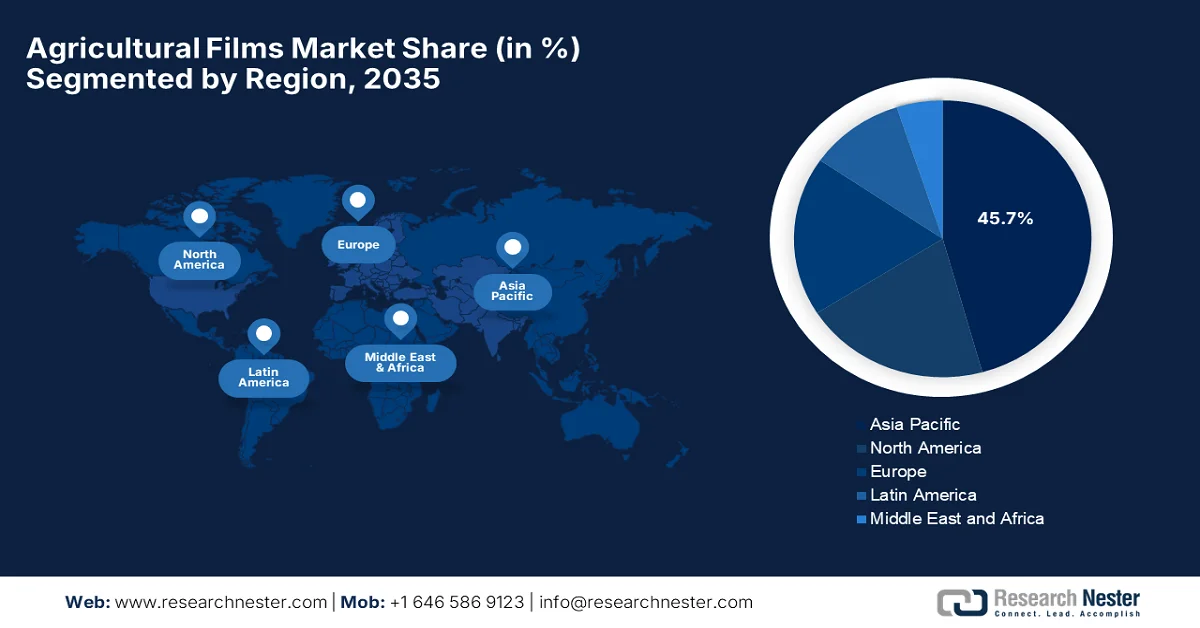

- The Asia Pacific agricultural films market is projected to dominate by capturing a 45.7% share by 2035, underpinned by rising population pressure and escalating food demand that are encouraging governments to promote film-based solutions to boost agricultural output.

- North America is expected to register the fastest growth over the forecast period, supported by the accelerating adoption of precision and sustainable farming practices that are expanding the use of advanced agricultural films to enhance crop quality and yields.

Segment Insights:

- The LLDPE subsegment in the agricultural films market is estimated to account for a leading 40.6% share by 2035, reinforced by its high tensile strength, flexibility, UV stability, and cost efficiency that enable durability across diverse climatic conditions.

- Mulch films are anticipated to witness notable growth through the forecast years, stimulated by their extensive application in soil moisture retention, temperature regulation, and weed suppression that directly supports higher crop productivity.

Key Growth Trends:

- Growing global food demand & crop yield optimization

- Expansion of protected cultivation

Major Challenges:

- Environmental and regulatory challenges

- Supply chain and raw material volatility

Key Players: Berry Global Group, Inc. (U.S.), BASF SE (Germany), ExxonMobil Chemical (U.S.), Dow Inc. (U.S.), RKW Group / RKW SE (Germany), Coveris Group (Austria), Armando Alvarez Group (Spain), Trioplast Industrier AB (Sweden), Kuraray Co., Ltd. (Japan), Novamont S.p.A. (Italy), Ginegar Plastic Products Ltd. (Israel), Plastika Kritis S.A. (Greece), British Polythene Industries (BPI) (UK), Polifilm Group (Germany), AB Rani Plast Oy (Finland), Uflex Ltd. (India), Jindal Poly Films Ltd. (India), Polyplex Corporation Ltd. (India).

Global Agricultural Films Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 14.1 billion

- 2026 Market Size: USD 15.4 billion

- Projected Market Size: USD 31.1 billion by 2035

- Growth Forecasts: 9.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (45.7% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, Germany, France

- Emerging Countries: India, Brazil, Mexico, Vietnam, Indonesia

Last updated on : 6 February, 2026

Agricultural Films Market - Growth Drivers and Challenges

Growth Drivers

- Growing global food demand & crop yield optimization: The expanding global population and increasing pressure on food production are primary drivers for the agricultural films market. Based on the official statistics reported by FAO, agricultural production in December 2024 during the time span of 2010 to 2023, the worldwide fruit and vegetable production reached 2.1 billion tonnes in 2023, which marks a 1 % increase from 2022. Therefore, this growth reflects constant efforts from governments and farmers to meet rising global demand driven by population growth, dietary diversification, and nutrition-focused policies. On the other hand, over the last decade, production has steadily expanded, which indicates pressure on supply to keep pace with consumption, and it motivates farmers to adopt yield-enhancing technologies such as mulches, greenhouse films, and other precision horticultural methods, benefiting the international market growth.

- Expansion of protected cultivation: Protected agriculture, such as greenhouses, high tunnels, and shade houses, is widely adopted to overcome climate challenges and extend growing seasons. In this context, films used in these systems enhance microclimate control, enabling year-round cultivation of high-value crops, fostering a favorable business ecosystem for the market. In this context USDA in February 2024 officially reported that, within a duration of 10 years, controlled environment agriculture in the U.S., including greenhouses, vertical farms, hydroponics, and aquaponics, more than doubled in operations by increasing from 1,476 to 2,994, whereas the production volumes increased 56% to 7.86 million hundredweight. In addition, the data highlighted that CEA systems allow growers to control temperature, light, wind, and precipitation by addressing adverse weather and pests, enhancing both yield and crop quality.

- Water conservation & resource efficiency: Agricultural films are best known to improve water-use efficiency by reducing evaporation and maintaining soil moisture. This makes them significant in water-scarce regions where proper irrigation and water conservation are highly essential, making it suitable for the agricultural films market upliftment. In this context government of China in March 2024 reported that the country faces severe water scarcity, with per capita water resources being 35% of the world's average and two-thirds of cities experiencing shortages. Besides, in a span of 10 years, water-use efficiency improved, in which the farmland irrigation efficiency rose from 0.530 to 0.576, and total water consumption remained stable under 610 billion m³ despite a near-doubling of GDP. In addition, the government has prioritized water conservation through various strategies, such as nationwide policies, campaigns, and the 2023 water conservation regulations, efficiently promoting water-saving agriculture and irrigation efficiency.

Challenges

- Environmental and regulatory challenges: The conventional polyethylene and polypropylene, the key agricultural film types, mostly contribute to soil and water pollution when they are not properly disposed of. This causes microplastic accumulation in the agricultural lands, whereas the growing environmental awareness has led to strict regulations on single-use plastics as well as mandatory recycling or biodegradable alternatives in most of the countries. Therefore, compliance with country-specific disposable laws increases production expenses and limits material options for manufacturers. In addition, the aspect of inconsistent recycling infrastructure in developing regions causes hurdles to widespread adoption of biodegradable or recyclable films. In this context, companies need to focus on the balance of regulatory compliance with cost-effectiveness while developing sustainable alternatives for the welfare of the market.

- Supply chain and raw material volatility: The reliance of polymers such as LLDPE, LDPE, and HDPE, whose prices fluctuate owing to crude oil volatility and global supply chain disruptions, is the major challenge for the agricultural films market. Therefore, this affects manufacturing costs, margins, and ultimately pricing for farmers. Also, the geopolitical tensions highlighted vulnerabilities in sourcing raw materials, especially in regions that are mostly dependent on imports. In addition, any delays in terms of shipping and logistics can hinder timely delivery during planting or harvesting seasons, which is highly essential for crop protection films. In this context, manufacturers must maintain a resilient supply chain and optimize inventory management by balancing cost pressures. Hence, these supply challenges pose a consistent risk to profitability and market growth in both developed and emerging regions.

Agricultural Films Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.2% |

|

Base Year Market Size (2025) |

USD 14.1 billion |

|

Forecast Year Market Size (2035) |

USD 31.1 billion |

|

Regional Scope |

|

Agricultural Films Market Segmentation:

Material Segment Analysis

The LLDPE subsegment is projected to dominate with the largest share of 40.6% by 2035, owing to its excellent tensile strength, flexibility, UV resistance, and cost-effectiveness, enabling long service life in diverse climates. In this context, SABIC, in October 2024, reported that it has partnered with iyris and Napco National to develop a high-tech agricultural greenhouse roofing solution using LLDPE from its TRUCIRCLE portfolio for Saudi Arabia’s national food production initiative. Besides, these films were produced with advanced recycling of post-consumer plastics, delivering high tensile strength, UV stability, and thermal control through Iyris’ SecondSky technology. Such collaborations amongst major industry players reflect the prominence of circular LLDPE solutions, which can enhance agricultural sustainability and food security in diverse climates, contributing to the agricultural films market growth.

Product Type Segment Analysis

The mulch films, which are a type of product, are expected to grow at a considerable rate in the market. The growth of the segment is mainly propelled by its widespread utilization to retain soil moisture, regulate soil temperature, and suppress weeds, directly improving crop yields. Also, their advantages in terms of soil management and broad use in horticulture and row crops worldwide are also propelling the continued growth of the subtype. Based on the government data published by the Ministry of Information & Broadcasting, India’s Union Cabinet in August 2024, approved the Clean Plant Programme (CPP) under the Mission for integrated development of horticulture, with a total investment of ₹1,765.67 crore (USD 210 to 215 million) to enhance fruit crop quality and productivity nationwide. Besides, the programme focuses on providing virus-free, certified planting material through nine clean plant centers, by strengthening nurseries, farmer incomes, and export competitiveness.

Application Segment Analysis

In the application segment crop protection/horticulture subsegment is forecasted to grow with a significant share over the forecasted years. The increasing adoption among growers of protected cultivation and soil conservation techniques to meet food demand is the key factor behind this leadership. Also, these films extensively support controlled environments and yield optimization for fruits, vegetables, and flowers. The government-backed initiatives and institutional programs are solidifying this trend by proactively promoting protected cultivation practices such as greenhouses, shade nets, and mulching to enhance productivity and climate resilience. As a result, crop protection and horticulture applications continue to command a strong share in the agricultural films market due to their direct impact on yield stability, quality improvement, and resource efficiency, hence denoting a wider segment scope.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Material |

|

|

Product Type |

|

|

Application |

|

|

End use |

|

|

Functionality |

|

|

Thickness |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Agricultural Films Market - Regional Analysis

APAC Market Insights

The Asia Pacific agricultural films market is forecasted to be the dominating region, capturing a share of 45.7% during the forecasted period. The rising population, coupled with increasing food demand are the main factor driving this leadership. Governments across the region are promoting these films to accelerate agricultural production in order to meet this demand. In this context, FFTC revealed that the FY2023 White Paper highlights challenges from rising food prices, climate change, and Japan’s aging population, reflecting the urgent need for a sustainable and resilient food system. It also mentioned the policy measures, which include legal revisions, fiscal allocations of ¥2.2683 trillion (USD 16.55 billion) for agriculture, and additional supplementary budgets of ¥818.2 billion (USD 5.97 billion), supporting infrastructure, smart agriculture, and disaster resilience. Furthermore, the future contributions are mainly focused on strengthening food security, the Green Food System Strategy for environmental sustainability, and supporting rural communities.

The increasing adoption of plastic mulch and greenhouse films are responsible factor for the growth of the market in China. The constant government backing in terms of protected cultivation methods is readily accelerating the demand. Based on the government data from SCN in January 2024, Sichuan Province is deliberately promoting the scientific use, recycling, and disposal of plastic mulch films to protect farmland and support ecological revitalization, adopting the completely biodegradable films on more than 11.5 million mu (767,000 ha), with ¥375 million (USD 27.4 million) in government funding. Besides, it also observed that the province has successfully established a three-tiered recycling network of 8,883 outlets, subsidized farmers (over ¥40 per mu) and disposal companies (up to ¥2,800 per ton), and processes waste film into reusable materials. Hence, such instances encourage both domestic and international players in the country to develop environmentally secure films.

Subsidy Rates for Mulch Films in Qianjiang City (RMB & USD)

|

Mulch Film Type |

Covered Crops |

Subsidy Amount |

Subsidy Amount (USD) |

|

Thickened High-Strength |

Fruit trees |

15 RMB |

2.10 USD |

|

Thickened High-Strength |

Watermelon, greenhouse vegetables, open-field crops, medicinal herbs, potatoes |

30 RMB |

4.20 USD |

|

Fully Biodegradable |

Potatoes, greenhouse vegetables |

60 RMB |

8.40 USD |

Source: HBQJ, March 2025

The government’s preference for modern agriculture and favorable schemes are the key factors driving the upliftment of the agricultural films market in India. These initiatives provide financial assistance, encouraging farmers to opt for technically advanced farming procedures. In this context, in August 2024 government of India reported that it is proactively promoting sustainable and organic farming through initiatives such as NMSA, PKVY, and MOVCDNER with a collective aim to enhance soil health, climate resilience, and long-term food security. As of June 2024, MOVCDNER has released ₹1,150.09 crore (USD 140 million) by covering 172,966 hectares and benefiting 189,039 farmers, whereas PKVY has allocated ₹2,078.67 crore (approximately USD 253 million) across 38,043 clusters covering 8.41 lakh hectares. On the other hand, programs such as PM-PRANAM and Large Area Certification have supported natural farming on 4.09 lakh hectares and certified 77,145 hectares in Andaman, Lakshadweep, Ladakh, and Sikkim. Hence, these constant administrative efforts are strengthening farmer income and the resilience of India’s agricultural systems, thereby expanding the use of agricultural films.

India Fruits & Vegetables Production and Exports: Official Statistics (2021-22)

|

Category |

Data |

Notes |

|

Vegetable Production (2021-22) |

204.61 million tonnes |

India is the 2nd largest producer globally |

|

Fruit Production (2021-22) |

107.10 million tonnes |

Up from 97.97 million tonnes in 2018-19 (CAGR 3%) |

|

Area under Vegetable Cultivation |

11.28 million hectares |

Major states: UP, MP, WB, Bihar, Gujarat, Odisha, Maharashtra |

|

Area under Fruit Cultivation |

7.09 million hectares |

Major states: Andhra Pradesh, Maharashtra, MP, UP, TN, Karnataka, Gujarat |

|

Fresh Fruits & Vegetables Exports (2021-22) |

USD 1,527.6 million (₹11,412.5 crore) |

Fruits: USD 750.7 million, Vegetables: USD 767.01 million |

|

Processed Fruits & Vegetables Exports (2021-22) |

USD 1,724.88 million (₹12,858.66 crore) |

Vegetables incl. pulses: USD 610.69 million |

|

HortiNet-Mango |

38,000 farmers, 66,000 farms |

Digital traceability system |

|

HortiNet-Vegetables |

10,000 farmers, 10,000 farms |

Covers 43 vegetables |

|

Kisan Rail Services |

157 trains on 18 routes |

Transport perishable produce; 50% subsidy under Operation Greens |

|

Export Target (2022-23) |

USD 23.56 billion |

Agricultural & processed food sector; 40% achieved in first 4 months |

Source: IBEF

North America Market Insights

The North America agricultural films market is predicted to witness the fastest growth during the discussed timeframe. The growth of the region is highly fueled by the fact that farmers in the region are increasingly adopting innovative agricultural practices, including sustainable and precision farming techniques. Among these practices, the use of modern agricultural films is gaining traction to enhance crop quality and yield. In this context the findings from USDA official data revealed that Washington State University, supported by the USDA Specialty Crop Research Initiative (SCRI), is conducting a project from 2022 to 2026 to improve end-of-life management of polyethylene (PE) mulch in strawberry systems, with a cumulative award of USD 8.01 million. In this context, the project aims to provide sustainable solutions that maintain horticultural benefits, reduce plastic pollution, and offer strategies applicable to other specialty crops, hence making it suitable for standard market growth.

Farmers in the country are utilizing mulch, silage, and greenhouse films to boost crop productivity and improve soil management, fostering a favorable business ecosystem for the U.S. market. In addition, the expansion of horticulture and high-value crop cultivation efficiently supports strong market adoption, encouraging key pioneers to enhance their product offerings. In this context, in July 2024, Revolution Sustainable Solutions announced the acquisition of Norflex, which is one of the major producers of agricultural and industrial film products. This strategic move is expected to add Norflex’s Agriseal silage wrap and robust stretch and shrink film lines, enhancing Revolution’s ability to provide high-performance solutions. Hence, such strategic moves from players will position the U.S. as a predominant leader in eco-friendly film utilization.

Canada agricultural films market has gained enhanced exposure due to the expansion of protected agriculture in Ontario, Quebec, and British Columbia. Also, there has been an increased demand for mulch films and sustainable alternatives with a prime focus on boosting crop production. In this context Canada government report estimates show that the country’s greenhouse vegetable and mushroom operations contribute USD 3.4 billion in farm gate sales and more than USD 2.5 billion in exports in 2024. Besides, during the same year, Canada had 974 greenhouse vegetable operations producing 866,484 metric tons, which is a 5 % increase from 2023, with exports rising 17 % to USD 1.95 billion; mushrooms also saw growth in production and export, reaching 148,569 metric tons and were valued at USD 749.9 million. Hence, these trends reflect significant capital investment in technology and a prime focus on meeting growing domestic and international demand.

Canada’s Greenhouse Vegetable Imports by Commodity (Volume in Metric Tons, 2020-2024)

|

Commodity |

2020 |

2021 |

2022 |

2023 |

2024 |

2024 Share (%) |

|

Tomatoes |

66,996 |

75,306 |

77,847 |

87,047 |

91,812 |

49.6 |

|

Peppers |

49,150 |

52,738 |

61,062 |

73,526 |

72,513 |

39.2 |

|

Cucumbers |

21,105 |

25,412 |

18,360 |

21,893 |

19,229 |

10.4 |

|

Lettuce |

68 |

64 |

142 |

493 |

1,497 |

0.8 |

|

Total |

137,319 |

153,521 |

157,411 |

182,959 |

185,051 |

100.0 |

Source: Government of Canada

Number of Greenhouse Vegetable Operations in Canada by Province (2020-2024)

|

Province |

2020 |

2021 |

2022 |

2023 |

2024 |

2024 % Share |

|

Atlantic provinces |

65 |

74 |

65 |

67 |

72 |

7.4% |

|

Quebec |

230 |

236 |

212 |

250 |

260 |

26.7% |

|

Ontario |

315 |

321 |

387 |

380 |

382 |

39.2% |

|

Prairie provinces |

98 |

103 |

99 |

96 |

96 |

9.9% |

|

British Columbia |

150 |

158 |

167 |

167 |

163 |

16.7% |

|

Canada (Total) |

858 |

892 |

930 |

960 |

974 |

100.0% |

Source: Government of Canada

Europe Market Insights

Europe agricultural films market is anticipated to represent consistent growth during the discussed timeframe, owing to the funding grants, robust regulatory framework that has been constantly promoting sustainability and environmental protection. On the other hand, the heightened demand for biodegradable mulch and silage films, aligned with regional farmers’ shift toward sustainable practices, is also prompting market expansion. The CELLAGRI project, which was funded by the European Innovation Council with a €3.97 million (approximately USD 4.3 million) contribution, is developing cellulose-based mulch films with nature-inspired microfluidic water-management structures for agriculture and horticulture. Furthermore, the project is targeting TRL 5 and the project includes real field tests and scalable roll-to-roll production, aiming to provide cost-effective, bio-based, and widely adoptable sustainable agricultural films.

The advanced farming technologies and strong commitment to sustainability are the key factors driving the agricultural films market in Germany. Farmers in the country are extensively using reusable and recyclable greenhouse and silage films to enhance yields and minimize waste. On the other hand, the tightening plastic regulations spurred demand for biodegradable films, whereas significant investment in research and innovation focused on recycling agricultural films. The widespread adoption of precision farming technologies optimizes film usage and improves crop productivity in Germany. The country also benefits from government incentives and EU-funded projects, whereas the rising consumer demand for environmentally responsible produce has encouraged farmers to integrate eco-friendly films into everyday operations, hence denoting a positive market outlook.

The increasing adoption of protected agriculture and sustainable farming practices is fueling the growth of the UK agricultural films market. Growers in the country are focusing on greenhouse and mulch films to extend growing seasons and reduce labor inputs. In this context, in April 2025, the country’s Government announced a £45.6 million (USD 52 million) investment to support the development and adoption of innovative agricultural technologies, which are mainly aimed at boosting food production, farmer profits, and sustainability. It also mentioned the key measures, which were ADOPT competition, allocating £20.6 million (USD 23.5 million) to help farmers trial new technologies on their farms, bridging the gap between innovation and real-world application. Also, these efforts form part of the government’s plan for change, with a main concentration on strengthening food security, promoting sustainable practices, and supporting the rural economy in the country.

Key Agricultural Films Market Players:

- Berry Global Group, Inc. (U.S.)

- BASF SE (Germany)

- ExxonMobil Chemical (U.S.)

- Dow Inc. (U.S.)

- RKW Group / RKW SE (Germany)

- Coveris Group (Austria)

- Armando Alvarez Group (Spain)

- Trioplast Industrier AB (Sweden)

- Kuraray Co., Ltd. (Japan)

- Novamont S.p.A. (Italy)

- Ginegar Plastic Products Ltd. (Israel)

- Plastika Kritis S.A. (Greece)

- British Polythene Industries (BPI) (UK)

- Polifilm Group (Germany)

- AB Rani Plast Oy (Finland)

- Uflex Ltd. (India)

- Jindal Poly Films Ltd. (India)

- Polyplex Corporation Ltd. (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Berry Global Group, Inc. has registered itself as one of the most prominent global suppliers of engineered plastic films, which also includes agricultural films such as mulch, greenhouse, and silage wraps. Simultaneously, the company has an extensive manufacturing footprint with facilities existing across the globe, and it focuses on sustainability, circular economy, and innovations such as high‑recycled content products.

- BASF SE is based in Germany and its agricultural films business leverages chemical and polymer expertise to deliver exceptional solutions, which include biodegradable mulch films and UV-stabilized greenhouse films. Besides the firm’s products, which support sustainable farming practices by readily enhancing crop performance and addressing soil contamination concerns through its biodegradable biopolymer technologies.

- Dow Inc. is considered to be a major player in advanced polymer technologies for agricultural films, concentrating on durability, weather resistance, and performance under various types of agronomic conditions. In addition, Dow’s films aim to improve crop yields and reduce environmental impact through a very enhanced UV resistance and mechanical strength.

- RKW Group has a strong portfolio in agricultural films such as mulch, silage, and greenhouse coverings. It operates globally and makes continued investments in terms of sustainable and high-performance film solutions, making it suitable for both traditional and modern farming requirements.

- Coveris Group is yet another central player in this field and produces a broad range of flexible films for agriculture, such as silage stretch and protective crop covers, by combining technical performance with sustainability. The company has a very strong presence in Europe and focuses on product customization, quality, and long-standing customer relationships to support agribusinesses with highly suited film solutions.

Below is the list of some prominent players operating in the global market:

The global agricultural films market is considered to be extremely competitive, in which the leading players, such as Berry Global, BASF, and Dow, are vying to strengthen their international market presence. These key pioneers are making heavy investments in R&D to improve UV resistance, durability, and biodegradable options in response to environmental regulations. On the other hand, capacity expansions, biodegradable material development, collaborations, and regional production localization to meet diverse agronomic requirements are some of the main strategies opted for by these players. Berry Global in March 2024 reported that it has expanded recycling capacity across its Europe-based facilities in the UK, Germany, and Poland by increasing recycled plastic output by approximately 6,600 tonnes per year, with a prime focus of meeting rising demand for high-performance films with this recycled content.

Corporate Landscape of the Agricultural Films Market:

Recent Developments

- In November 2025, Cosmo First Limited reported that it had entered a 50-50 strategic joint venture with Filmax Corporation to introduce multiple Cosmo First business verticals into the South Korean market and bring Filmax products to global markets.

- In 2025, Harnois Greenhouses reported that in partnership with Plastika Kritis, it had launched high-performance polyethylene greenhouse films, which include Suncooler, Polydispersive, EVO AC AR, and CHAMELEON, designed to optimize light, climate, and crop productivity.

- Report ID: 2739

- Published Date: Feb 06, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Agricultural Films Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.