Aerospace and Defense Propulsion System Market Outlook:

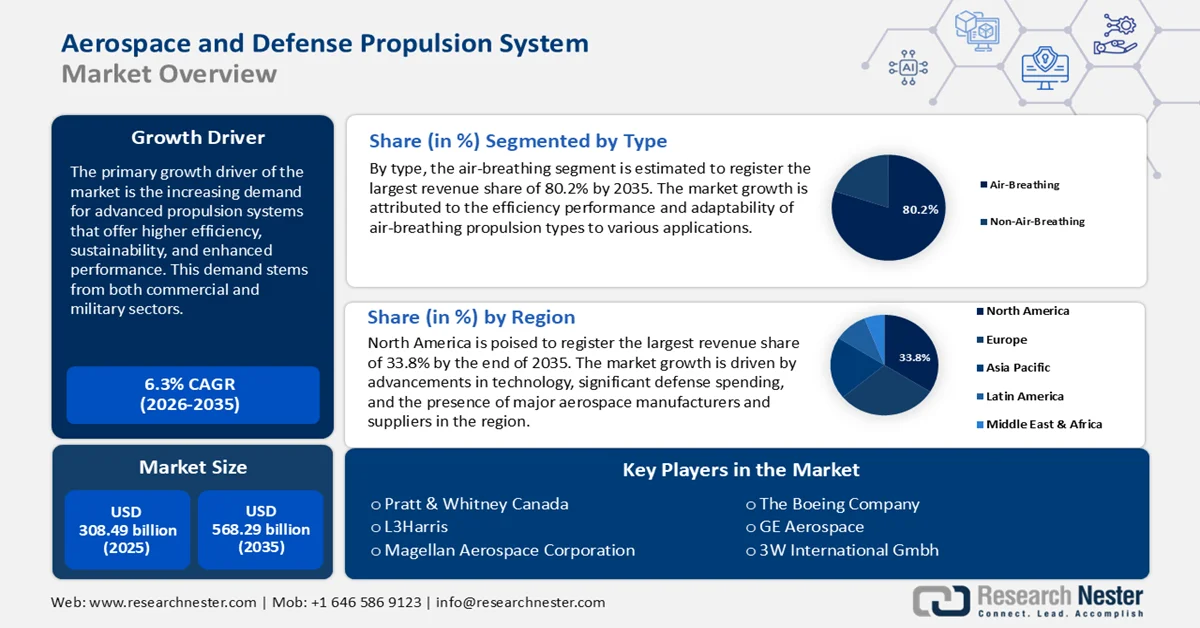

Aerospace and Defense Propulsion System Market size was valued at USD 308.49 billion in 2025 and is expected to reach USD 568.29 billion by 2035, expanding at around 6.3% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of aerospace and defense propulsion system is evaluated at USD 325.98 billion.

The primary growth driver of the market is the increasing demand for advanced propulsion systems that offer higher efficiency, sustainability, and enhanced performance. This demand stems from both commercial and military sectors. The push for sustainability, advancements in propulsion technologies, growing defense spending, and expansion of space exploration collectively drive the market. According to the Peter G Peterson Foundation, the Office of Management and Budget estimates that the U.S. spent USD 820 billion on national defense in fiscal year 2023, accounting for 13% of overall federal spending.

Key Aerospace and Defense Propulsion System Market Insights Summary:

Regional Highlights:

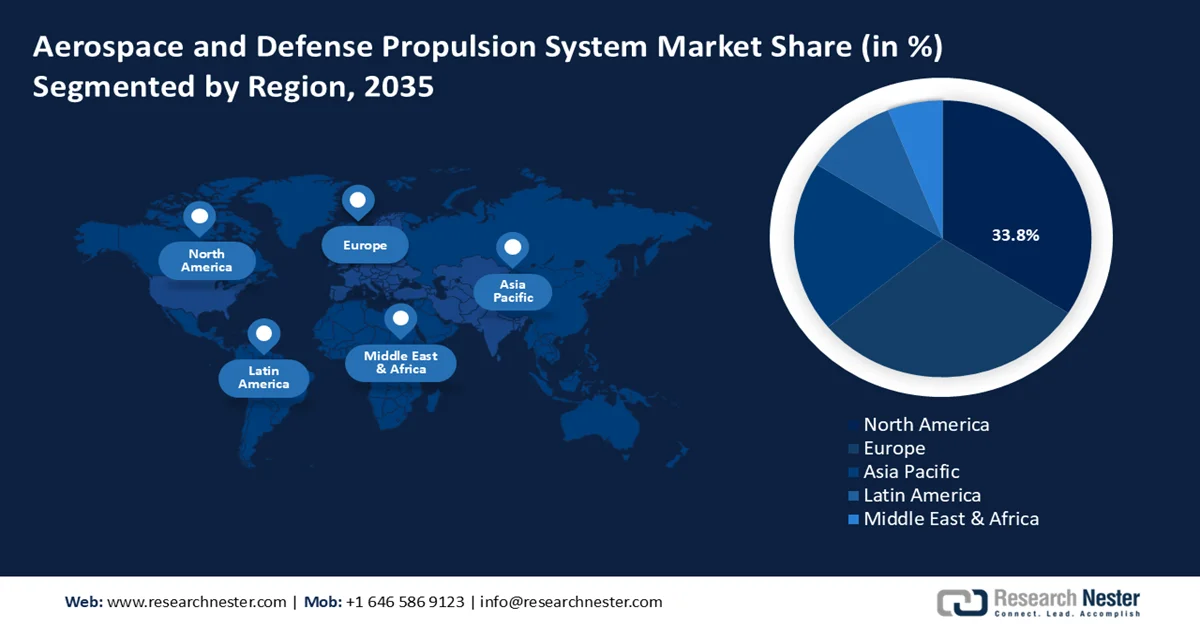

- North America is projected to hold more than 33.8% revenue share by 2035, stimulated by advancements in technology, significant defense spending, and the presence of major aerospace manufacturers and suppliers in the aerospace and defense propulsion system market.

- Europe is expected to achieve the fastest revenue growth by 2035, owing to robust government support, a strong industrial base, and a focus on sustainability.

Segment Insights:

- The air-breathing segment is projected to account for more than 80.2% share by 2035, impelled by the efficiency performance and adaptability of air-breathing propulsion types to various applications in the aerospace and defense propulsion system market.

- The unmanned aerial vehicles (UAVs) segment is anticipated to hold a 19.4% share by 2035, fueled by the rising use of UAVs in military and commercial operations.

Key Growth Trends:

- Rising demand for fuel efficiency and sustainability

- Technical advancements

Major Challenges:

- High research and development costs

- Complex regulatory and certification processes

Key Players: Cardax, Inc., Novartis AG, Eli Lilly and Company, Novo Nordisk A/S, Bayer AG, AstraZeneca.

Global Aerospace and Defense Propulsion System Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 308.49 billion

- 2026 Market Size: USD 325.98 billion

- Projected Market Size: USD 568.29 billion by 2035

- Growth Forecasts: 6.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (33.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Russia, France, United Kingdom

- Emerging Countries: China, India, Japan, South Korea, Brazil

Last updated on : 25 February, 2026

Aerospace and Defense Propulsion System Market - Growth Drivers and Challenges

Growth Drivers

-

Rising demand for fuel efficiency and sustainability: The increasing focus on fuel efficiency and sustainability is a key driver of growth in the aerospace and defense propulsion system market. Companies are developing hybrid-electric engines that combine traditional propulsion systems with electric technologies to reduce fuel consumption and emissions. Hybrid-electric engines can lower carbon dioxide equivalent emissions by 1.61-4.71 gigatons by 2050, saving USD 1.55-4.49 trillion in fuel and operating costs throughout the automobiles' lifetimes. Electric propulsion systems are gaining traction in urban air mobility (UAM) applications and smaller aircraft. Also, increased adoption of sustainable aviation fuel (SAF) and biofuels reduces the carbon footprint of traditional engines, spurring demand for engines compatible with alternative fuels.

Additionally, organizations such as the International Civil Aviation Organization (ICAO) and the European Union are enforcing stricter emissions standards under initiatives like the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA). This regulatory pressure not only ensures adherence to global standards but also provides opportunities for manufacturers to gain a competitive edge and align with the growing demand for greener aviation and defense solutions.

- Technical advancements: Technological advancements in propulsion systems are fundamentally reshaping the aerospace and defense sectors. Innovations in fuel efficiency, materials, electric and hybrid technologies, hypersonic propulsion, and space exploration are driving aerospace and defense propulsion system market growth. Technological advancements also support next-generation military systems like stealth aircraft and hypersonic weapons, driving demand for cutting-edge propulsion solutions.

Moreover, AI-powered algorithms analyze complex data to optimize engine designs for efficiency, durability, and performance, reducing development time. In the aerospace industry, AI algorithms can reduce the time needed for designing propulsion systems by up to 50% through advanced simulations and generative design techniques. AI-based simulation tools can cut development costs by up to 20-30% by enabling faster iteration and testing of propulsion system designs.

- Advancements in aerospace manufacturing: Advancements such as additive manufacturing (3D printing) are revolutionizing the way propulsion components are designed and manufactured. It allows for the creation of intricate geometries that are difficult to achieve with traditional manufacturing techniques. This leads to weight and cost reduction, and faster prototyping and iteration.

Innovations in material science, such as the development of heat-resistant alloys, composite materials, and advanced ceramics, are directly impacting the propulsion system. These materials allow for engines that can operate at higher temperatures and pressures, improving both performance and efficiency.

Challenges

-

High research and development costs: Developing cutting-edge propulsion technologies requires significant investment in research and development (R&D). The costs associated with designing, testing, and certifying new propulsion systems can be prohibitively high. This financial burden is particularly challenging for smaller players in the aerospace and defense propulsion system market and can slow down innovation, especially in sectors like hybrid and electric propulsion.

-

Complex regulatory and certification processes: Aerospace and defense propulsion systems must meet strict regulatory standards set by authorities such as the Federal Aviation Administration (FAA) or the European Union Aviation Safety Agency (EASA) for commercial applications, and the Department of Defense (DoD) for military systems. The lengthy and complex certification processes for new technologies can delay product development and entry into the market. Compliance with safety, environmental, and operational standards adds a layer of cost and time to the development cycle.

Aerospace and Defense Propulsion System Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.3% |

|

Base Year Market Size (2025) |

USD 308.49 billion |

|

Forecast Year Market Size (2035) |

USD 568.29 billion |

|

Regional Scope |

|

Aerospace and Defense Propulsion System Market Segmentation:

Type Segment Analysis

The air-breathing segment is anticipated to hold aerospace and defense propulsion system market share of more than 80.2% by 2035. The market growth is attributed to the efficiency performance and adaptability of air-breathing propulsion types to various applications. Air-breathing engines, such as jet engines, ramjets, scramjets, and combined-cycle propulsion systems, rely on atmospheric oxygen for combustion, eliminating the need to carry oxidizers onboard. This design reduces overall weight and improves fuel efficiency, making these systems ideal for various applications.

Fighter jets and other defense platforms rely on air-breathing engines for high thrust-to-weight ratios and adaptability to supersonic or hypersonic speeds. A hot test of a ramjet engine conducted by the Indian Space Research Organization (ISRO) in 2022 revealed that the scramjet engine outperforms the ramjet engine as it runs well at hypersonic speeds and allows for supersonic combustion. Air-breathing provides a technological foundation for low-cost space transportation technology. This technology represents a crucial step toward the development of reusable launch vehicles. The propellant mass of the launch vehicle accounts for 86% of its total mass and 70% of the fuel is oxidizer. Since these engines use atmospheric oxygen, which is available up to 50 kilometers above the earth's surface, they can save about 70% of the propellant carried in the vehicles.

Application Segment Analysis

In aerospace and defense propulsion system market, unmanned aerial vehicles (UAVs) segment is poised to capture revenue share of around 19.4% by the end of 2035. The market growth is attributed to the increasing use of UAVs in military and commercial applications. UAVs are extensively used for reconnaissance, surveillance, intelligence gathering, and combat missions. The demand for propulsion systems tailored to specific mission profiles, such as long endurance, high payload capacity, and stealth, is boosting market growth.

UAVs are increasingly adopted in the commercial sector for tasks like infrastructure inspection, agriculture, logistics, and environmental monitoring. These applications demand cost-effective and efficient propulsion solutions that can enhance operational range and reliability.

Our in-depth analysis of the aerospace and defense propulsion system market includes the following segments:

|

Type |

|

|

Application |

|

|

End use |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Aerospace and Defense Propulsion System Market - Regional Analysis

North America Market Insights

North America in aerospace and defense propulsion system market is projected to hold more than 33.8% revenue share by 2035. The market growth is driven by advancements in technology, significant defense spending, and the presence of major aerospace manufacturers and suppliers in the region. The region is expected to maintain its leadership in the aerospace and defense system market due to ongoing innovation. The integration of electrification and sustainable propulsion solutions is likely to be a major trend in the coming years.

The U.S. has the highest defense budget in the world, supporting projects that demand advanced propulsion systems such as fighter jets, hypersonic weapons, long-range missile systems, and drones. Major manufacturers like Boeing and General Electric Aviation drive innovations in propulsion systems for commercial aircraft, focusing on fuel efficiency and reduced emissions. High demand for next-generation airliners like Boeing’s 737 MAX and 777C is creating opportunities for propulsion technologies.

Canada ranks among the top aerospace nations globally, with leading companies like Bombardier, Pratt & Whitney Canada, and Magellan Aerospace contributing to the development of propulsion systems. a focus on designing and manufacturing engines for regional and business jets, helicopters, and UACs boosts market growth. Moreover, the Government of Canada’s commitment to modernizing its military, including investment in fighter aircraft and naval vessels, increases demand for propulsion systems.

Europe Market Insights

The aerospace and defense propulsion system market in Europe is poised to register the fastest revenue growth by 2035. The market in Europe is a highly competitive and innovation-driven sector, underpinned by robust government support, a strong industrial base, and a focus on sustainability. The region’s aerospace and defense industries are global leaders in developing advanced propulsion technologies for commercial aviation, military applications, and space exploration.

The UK’s significant defense budget and ongoing modernization programs are driving demand for advanced propulsion systems for fighter jets, UAVs, and missile systems. Projects like the Tempest Future Combat Air System (FCAS) are central to the development of cutting-edge propulsion technologies, including variable-cycle engines. Moreover, the country is increasing its investment in UAVs for defense and civilian applications, driving demand for lightweight, high-efficiency propulsion systems.

Germany plays a significant role in developing propulsion technologies for military, commercial aviation, and space exploration. Government support, partnerships with the European Union, and strong industrial capabilities position Germany as a leader in aerospace and defense propulsion system market. As a major contributor to Airbus, Germany supports the development of advanced propulsion systems for commercial aircraft, such as the A320neo family, focusing on fuel efficiency and emissions reductions. The demand for sustainable aviation solutions drives R&D in hybrid-electric and SAF-compatible engines.

Aerospace and Defense Propulsion System Market Players:

- Bombardier Inc.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Pratt & Whitney Canada

- L3Harris

- Magellan Aerospace Corporation

- The Boeing Company

- GE Aerospace

- 3W International Gmbh

- Spirit AeroSystems

- Aero Engine Corporation of China

- CFM International

- Lockheed Martin Corporation

- MTU Aeroengines

Key players in the market are driving its growth through innovation, strategic partnerships, and investment in advanced technologies. The companies play a critical role in addressing the evolving demands of military, commercial, and space propulsion systems.

Here are some key players in the aerospace and defense propulsion system market:

Recent Developments

- In July 2023, L3Harris Technologies completed the acquisition of Aerojet Rocketdyne, creating a fourth business sector for the corporation. In December 2022, L3Harris reached a definitive deal to acquire Aerojet Rocketdyne, highlighting its ability to bolster the defense industrial base, increase competition, and expedite innovation for a major merchant provider of propulsion systems.

- In June 2023 Solvay joined Spirit AeroSystems (Europe) Limited as a strategic partner at their Aerospace Innovation Centre (AIC) in Prestwick, Scotland. The AIC brings together Spirit's industrial, academic, and supply-chain partners to conduct joint research on sustainable aviation technology. Both firms plan to focus on composite development to satisfy future aircraft performance, cost, and production requirements.

- Report ID: 6733

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.