Advanced IC Substrates Market Outlook:

Advanced IC Substrates Market size was valued at USD 21.12 billion in 2025 and is expected to reach USD 56.8 billion by 2035, registering around 10.4% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of advanced IC substrates is evaluated at USD 23.1 billion.

The advanced integrated circuit substrates are gaining traction due to the rapid industry shift toward cutting-edge packaging solutions such as fan-out wafer-level packaging, flip-chip ball grid arrays, and embedded bridge packaging. These solutions enable miniaturization, better electrical performance, and are a cost-effective alternative to address the growing requirements for compact and powerful electronic devices. Companies are introducing innovative IC substrates and are accelerating chip performance and efficiency. For instance, in December 2024, Broadcom unveiled the industry-leading F2F (Face-to-Face) packaging solution named XDSiP. The platform unifies 6,000 mm² of silicon elements with up to 12 High Bandwidth Memory (HBM) stacks into a single package to meet the high-efficiency and low-power demands of AI chips.

The next-generation packaging solutions require advanced IC substrates to enable advanced signal integrity and efficient power usage, and effective heat dissipation capabilities. Companies such as Broadcom, Taiwan Semiconductor Manufacturing Company, and Electronic Design Automation are actively working toward improving substrate design procedures and manufacturing techniques for AI-based systems, high-performance computing, and 5G applications. The rapidly expanding semiconductor technologies, coupled with rising advanced IC substrates market competition, are propelling the advancements in IC substrates and making them essential for semiconductor packaging development.

Key Advanced IC Substrates Market Insights Summary:

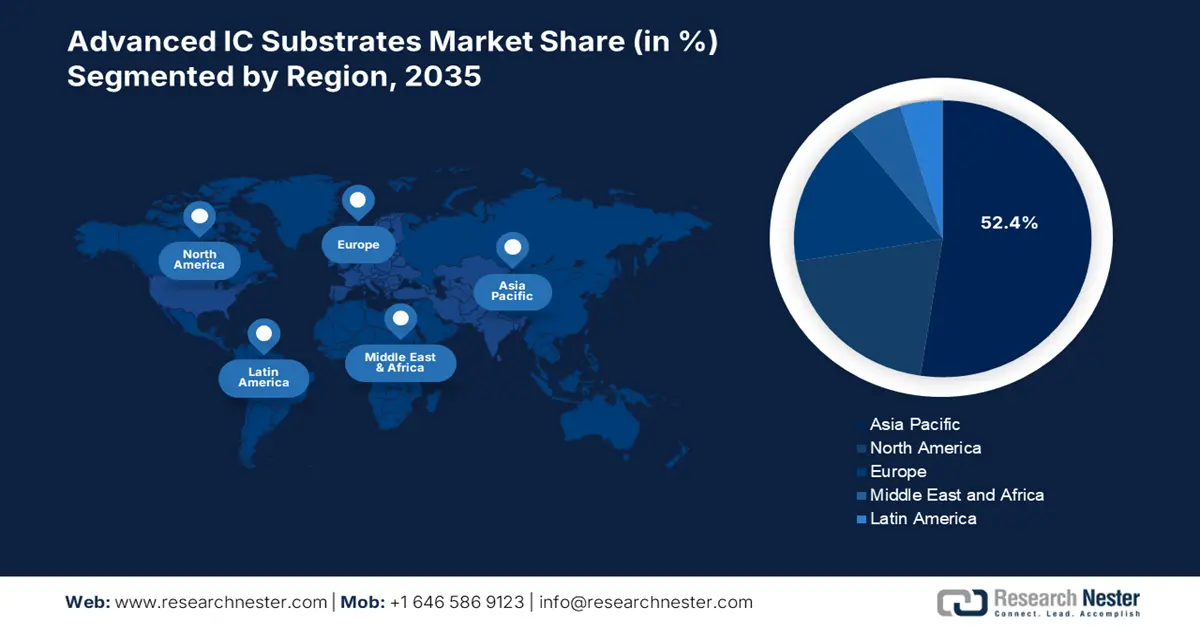

Regional Highlights:

- Asia Pacific holds a 52.4% share in the Advanced IC Substrates Market, driven by rapid expansion of semiconductor manufacturing and government investments, fostering growth through 2035.

Segment Insights:

- The Mobile and Consumer segment is poised for significant growth from 2026-2035, driven by high demand for smartphones and tablets requiring advanced IC substrates for miniaturized components.

Key Growth Trends:

- Growing demand for advanced IC substrates in the automotive sector

- Rising demand for HPC and AI applications

Major Challenges:

- Complexity in fabrication and yield issues

- Technological transition challenges

- Key Players: ASE Kaohsiung, Siliconware Precision Industries Co. Ltd., and TTM Technologies Inc.

Global Advanced IC Substrates Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 21.12 billion

- 2026 Market Size: USD 23.1 billion

- Projected Market Size: USD 56.8 billion by 2035

- Growth Forecasts: 10.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (52.4% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: China, Japan, South Korea, United States, Germany

- Emerging Countries: China, Japan, South Korea, Taiwan, India

Last updated on : 12 August, 2025

Advanced IC Substrates Market Growth Drivers and Challenges:

Growth Drivers

- Growing demand for advanced IC substrates in the automotive sector: The increasing adoption of electric vehicles, autonomous driving technologies, and advanced driver assistance systems is resulting in a significant demand for advanced semiconductor packaging solutions with high performance. Next-generation automotive applications require integrated circuit substrates due to their ability to offer high processing power, power management capabilities, and seamless connectivity. Automakers are emphasizing vehicle intelligence, safety, and user experience by integrating complex electronic systems, which are boosting the demand for advanced IC substrates. These substrates enable efficient interconnections between multiple semiconductor components, ensuring reliable operation in high-performance automotive environments.

- Rising demand for HPC and AI applications: The expansion of AI, ML, and HPC is resulting in an increasing need for next-generation integrated circuit substrates. Advanced substrates are essential as they optimize electrical operations, wiring density, and thermal control needed for complex AI and HPC processing requirements. Various companies are joining strategic partnerships to develop AI and HPC-enabled IC substrates. For instance, in November 2023, AT&S announced its plans to supply complex IC substrates to AMD for use in their high-performance data center processors and accelerators. These substrates highlight their significant position in modern computing systems by improving both data processing ability and power control systems.

Challenges

- Complexity in fabrication and yield issues: Production of advanced IC substrates depends on accurate techniques to laminate multiple layers, form microvia, and pattern ultra-thin circuits. However, the adoption of high-yield rates is challenging due to manufacturing issues, including misalignment, delamination, and warpage defects. The production difficulties, material losses, and elevated costs are direct consequences of these issues. Yield inconsistencies can slow the mass adoption and limit production scalability, impacting advanced IC substrates market growth.

- Technological transition challenges: The transition from conventional organic substrates to advanced materials such as glass-based or silicon interposers is posing significant technological challenges. In addition, ensuring seamless integration with existing semiconductor manufacturing processes requires extensive research and development and costly infrastructure upgrades. Material compatibility issues and fabrication complexities can delay large-scale adoption. As the semiconductor industry is moving toward heterogeneous integration, overcoming these technological transition hurdles remains a critical barrier to the widespread use of next-generation IC substrates.

Advanced IC Substrates Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

10.4% |

|

Base Year Market Size (2025) |

USD 21.12 billion |

|

Forecast Year Market Size (2035) |

USD 56.8 billion |

|

Regional Scope |

|

Advanced IC Substrates Market Segmentation:

Type (FC BGA, FC CSP)

FC BGA segment is projected to account for advanced ic substrates market share of more than 65.3% by the end of 2035, owing to the continuous evolution of semiconductor packaging, delivering increased electrical characteristics and miniaturization capabilities. Several organizations are actively expanding their presence in the FC-BGA substrates market. For instance, in February 2023, LG Innotek unveiled its latest FC-BGA substrate, featuring high integration, fine patterning, and minimized warpage. The company started its FC-BGA production with a new smart factory, with an investment of USD 336 million.

The rapid proliferation of data centers and cloud computing services is boosting the demand for high-performance servers capable of managing extensive data processing tasks. FC-BGA substrates are integral to these servers, offering enhanced electrical performance and reliability essential for efficient data handling. As businesses are increasingly transitioning to cloud-based solutions, the need for advanced IC substrates like FC-BGA is rising, supporting the infrastructure of modern data centers.

Application (Mobile and Consumer, Automotive, Transportation, IT, and Telecom)

The mobile and consumer segment in advanced ic substrates market is expected to account for a significant share, owing to the high demand for smartphones and tablets that need advanced IC substrates to support high-performance and miniaturized components. Consumers are seeking devices with enhanced features, such as high-resolution displays and powerful processors. This has resulted in increasing need for complex integrated circuits. Moreover, innovations in semiconductor packaging, such as the development of advanced IC substrates, enable the integration of more functionalities into compact devices. These substrates support high-density interconnects and efficient heat dissipation, essential for modern mobile and consumer electronics.

Various semiconductor companies are investing in advanced IC substrates to enhance performance and meet the evolving demands of mobile and consumer electronics. For instance, in October 2024, KLA introduced a comprehensive portfolio of IC substrates aimed at advancing semiconductor packaging technology. These solutions address challenges in advanced packaging applications to improve yield, performance, and reliability. This technological progress can facilitate the production of feature-rich, compact devices, further boosting the market.

Our in-depth analysis of the global advanced IC substrates market includes the following segments:

|

Type |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Advanced IC Substrates Market Regional Analysis:

Asia Pacific Market Analysis

Asia Pacific in advanced IC substrates market is anticipated to account for around 52.4% revenue share by 2035, owing to the rapid expansion of semiconductor manufacturing in countries, including India, China, and Japan. Governments in these countries are actively investing in semiconductor infrastructure and providing incentives to local manufacturers to enhance production capabilities. Moreover, the presence of leading foundries and packaging firms in the region is accelerating the demand for high-performance IC substrates, supporting advanced chip designs for applications like AI, 5G, and IoT.

The surging demand for consumer electronics and mobile devices is another major factor fueling the advanced IC substrates market growth. With the region being a global hub for smartphone and electronics manufacturing, companies are increasingly adopting advanced IC substrates to enhance device performance and energy efficiency. The shift towards miniaturized and high-density chip designs in smartphones, wearables, and other smart devices is further fueling the need for advanced IC packaging solutions, strengthening the market expansion in the region.

The China advanced IC substrates market is witnessing steady growth due to the country’s push for self-sufficiency in semiconductor manufacturing. The government is introducing policies, subsidies, and funding programs to reduce reliance on foreign semiconductor components, including IC substrates. Investments in domestic substrate production and packaging technologies are accelerating, as companies seek to strengthen the local supply chain. This is resulting in the rapid growth of domestic IC substrate manufacturers, enhancing the country’s capabilities in advanced semiconductor packaging.

The advanced IC substrates market in India is experiencing a rapid expansion, attributed to local government initiatives including the Design-Linked Incentive program and Production-Linked Incentive scheme. These policies encourage domestic and foreign investments in semiconductor fabrication and packaging, including IC substrates. The government is also approving multiple semiconductor projects, attracting global players to set up advanced packaging facilities in the country. This push is strengthening the country’s position in the semiconductor supply chain and fueling demand for high-quality IC substrates.

North America Market

The advanced IC substrates market in North America is expected to account for a significant share, attributed to the rapid electrification of vehicles and advancements in aerospace electronics. As the region emerges as a hub for electric vehicle production and aerospace innovation, the need for robust, high-performance substrates capable of supporting automotive-grade chips is growing rapidly.

The U.S. advanced IC substrates market is expected to experience significant growth, due to the country being at the forefront of semiconductor innovation, with leading firms driving the adoption of chipset-based architectures. This shift is fueling demand for high-performance IC substrates that enable ultra-fast, energy-efficient interconnections between multiple dies. As chipsets become integral to high-performance computing, AI, and data center applications, manufacturers are focusing on advanced packaging solutions like embedded bridges and silicon interposers to enhance signal integrity and power efficiency.

Local research institutions and semiconductor companies are developing next-generation IC substrates using novel materials like glass and advanced organic laminates to improve performance, thermal management, and miniaturization. For instance, in September 2023, Intel introduced glass substrates for next-gen HPC and AI chips, claiming significant improvements in power efficiency and signal transmission.

The advanced IC substrates market in Canada is expanding rapidly, attributed to the expanding research and development efforts in IC substrates. Leading universities and research institutes are collaborating with global semiconductor firms to develop next-generation packaging technologies. These efforts help improve substrate design for high-performance computing and AI applications, fostering a strong ecosystem for advanced IC substrate innovation.

Key Advanced IC Substrates Market Players:

- ASE Kaohsiung (ASE Inc.)

- Company Overview

- Business Strategy

- Key Technology Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Siliconware Precision Industries Co. Ltd.

- TTM Technologies Inc.

- AT&S Austria Technologies & Systemtechnik AG

The advanced IC substrates market is characterized by intense competition, with major players focusing on innovation, expansion, and collaborations to strengthen their advanced IC substrates market positions. Companies like Ibiden, Unimicron, Shinko Electric Industries, AT&S, and SEMCO lead the industry by advancing FC-BGA and FC-CSP technologies to cater to the growing demand from AI, 5G, and HPC applications. The market is also witnessing strategic mergers, acquisitions, and capacity expansions as firms scale up production to meet increasing requirements. Also, regional manufacturers across Asia Pacific and North America are enhancing their capabilities through R&D investments and supply chain improvements to stay competitive. Here are some key players operating in the global market:

Recent Developments

- In March 2025, TSMC announced plans to expand its investment in advanced semiconductor manufacturing in the U.S. with an additional USD 100 billion commitment. This builds upon the company’s ongoing USD 65 billion investment in its Phoenix, Arizona, operations, bringing TSMC’s total U.S. investment to USD 165 billion. The expansion will include the construction of three new fabrication plants, two advanced packaging facilities, and a major R&D center.

- In September 2024, Infineon announced a significant technological advancement in producing gallium nitride (GaN) chips. By successfully fabricating GaN chips on 300mm wafers, the company achieved a 2.3-fold increase in chip yield per wafer compared to the traditional 200mm wafers.

- Report ID: 7453

- Published Date: Aug 12, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Advanced IC Substrates Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.